Nyheter

En introduktion till BETS ETF, Europas första Sports Betting och iGaming ETF

Sports Betting and iGaming UCITS (ticker: BETS ETF) erbjuder Europas första möjlighet att få tillgång till ett snabbt växande underhållningssegment i form av en börshandlad fond.

Detta kommer att bli Europas första sportspel och iGaming ETF, och den europeiska investerarens första möjlighet att få tillgång till den snabbt växande globala sportspel- och onlinespelindustrin genom en ETF.

BETS ETF kommer att spåra det reglerbaserade Solactive Fischer Sports Betting and iGaming Index, vilket ger exponering för globala företag som genererar majoriteten av sina intäkter och/eller intäkter genom Sportsbetting och iGaming. Företag kategoriseras i pure-play och non-pure play baserat på deras exponering för dessa sportspel och iGaming.

Företag inkluderar B2C online-fokuserade varumärken som har exponering för ett brett utbud av onlinespelprodukter; omnichannel-företag med tegel och murbrukcasinon med en ökande tonvikt på online; och tjänster tillhandahåller B2C såsom teknikplattform, sportleverantörer, media och affiliate-marknadsföringsföretag.

Indexet är diversifierat över företagstyp, storlek och regional exponering. Det inkluderar större och mer etablerade företag tillsammans med flera små till medelstora företag som specialiserat sig på en aspekt av värdekedjan som kan växa i linje med eller snabbare än branschen.

Investment case

Den amerikanska investmentbanken Goldman Sachs förväntar sig att den amerikanska marknaden för sportspel och iGaming expanderar 23x från 2 miljarder dollar 2020 till 53 miljarder dollar 2033. Globalt förväntas branschen växa med 11 procent per år under de närmaste fem åren, enligt H2 Capital. Europa och Asien är också marknader med hög tillväxt.

Onlinespel hade tidigare varit olagligt i USA, men de senaste ändringarna i lagstiftningen som gjorde det möjligt för enskilda amerikanska stater att legalisera sportspel och iGaming, i olika former. Den förändrade lagstiftningen har varit en viktig tillväxtkatalysator för marknaden.

Andra tillväxtfaktorer inkluderar bredare social acceptans av sportspel som en underhållningsaktivitet, sportspelstöd från ligor, lag och medieföretag; konvertering från olagliga till lagliga marknader; tekniska förbättringar som möjliggör en förbättrad onlineupplevelse; och mer tid på mobila enheter.

Branschen har potential att generera attraktiv finansiell avkastning med MGM och Draftkings som förväntar sig EBITDA-marginaler på mellan 30-35 procent. Större aktörer som kan utnyttja marknadsföringskostnader (en av de viktigaste driftskostnaderna) inom ett bredare utbud av produkter och fysiska egenskaper förväntas generera över genomsnittliga marginaler. Relativt måttlig capex driver också över genomsnittet för Free Cash Flow och ROI.

Sports Betting and iGaming Index Information

| Index Top 10 Holdings (indikativt) | Vikt, % |

| DRAFTKINGS INC | 8.00% |

| EVOLUTION GAMING GROUP AB | 8.00% |

| FLUTTER ENTERTAINMENT PLC | 8.00% |

| SKILLZ INC | 8.00% |

| BOYD GAMING CORP | 5.00% |

| CAESARS ENTERTAINMENT INC | 5.00% |

| CHURCHILL DOWNS INC | 5.00% |

| ENTAIN PLC | 5.00% |

| MGM RESORTS INTERNATIONAL | 5.00% |

| PENN NATIONAL GAMING INC | 5.00% |

Svenska investerare noterar direkt att ett av de största innehaven i BETS ETF utgörs av svenska Evolution Gaming Group.

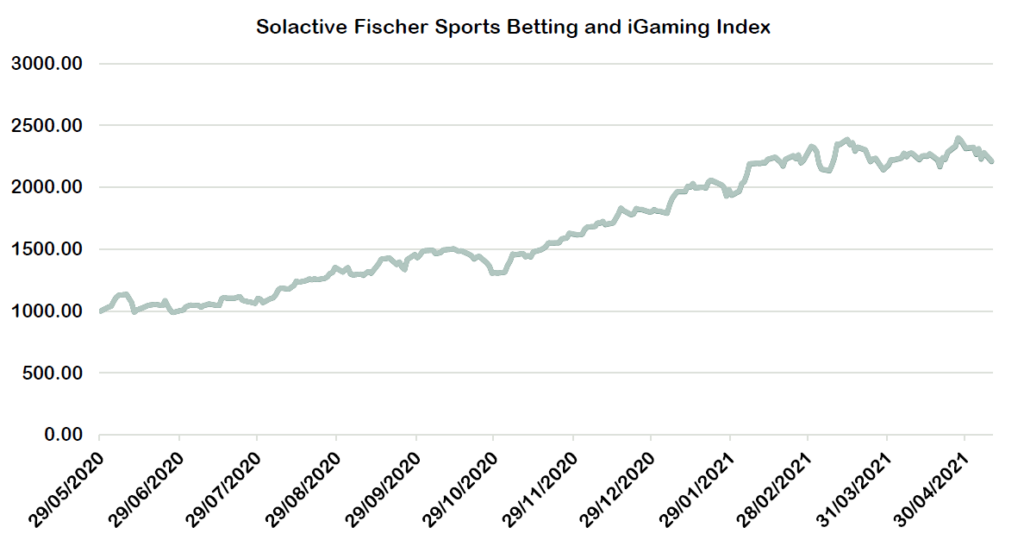

Källa: Solactive. Index data per den 29 januari 2021

Net Total Return: 121.17%; Källor: Solactive, HANetf and Bloomberg. Historisk utveckling är ingen garanti för framtida avkastning.

Utvecklingen före starten baseras på back testad indexdata. Backtestning är processen att utvärdera en investeringsstrategi genom att använda den på historisk data för att simulera vad resultatet av en sådan strategi skulle ha varit. Back testad data representerar inte verklig utveckling och ska inte tolkas som en indikation på verklig eller framtida utveckling. Tidigare resultat för indexet är i USD.

Tidigare resultat är inte en indikator för framtida resultat och bör inte vara den enda faktor som ska beaktas när du väljer en produkt. Investerare bör läsa emittentens prospekt (“Prospekt”) innan de investerar och bör hänvisa till avsnittet i Prospektet med rubriken ”Riskfaktorer” för ytterligare information om risker förknippade med en investering i denna produkt.

Källa: Solactive Fischer Sports Betting och iGaming Index; Bloomberg-data per 10/05/21.

Metodöversikt

- Företag som ingår i indexet vid lanseringen

- Globala företag noterade på en reglerad börs med ett börsvärde på minst 200 000 000 USD.

- En genomsnittlig daglig omsättning på minst 250 000 USD under de senaste tre månaderna inklusive urvalsdagen.

- Primär notering i ett av de länder som ingår i utvecklade marknader och tillväxtmarknader enligt definitionen i Solactive Country Classification samt Malta.

Undersökning

I indexets syfte är följande de produkter och / eller tjänster som anses passa Sports Betting och iGaming-indexstrategi:

- Drift av online/internet-spelplattformar;

- Business-to-consumer operatörer eller konsumentvänliga varumärken;

- Leverantörer av teknikplattformar som tillhandahåller infrastrukturen och andra inklusive hanteringssystem för spelarkonton; och

- Media, dotterbolag, streaming och innehåll och andra tjänsteleverantörer.

- Baserat på INDEX UNIVERSE bestäms den ursprungliga sammansättningen av indexet liksom alla val för en vanlig återbalans på urvalsdagen i enlighet med följande regler (”INDEX KOMPONENTKRAV”):

- Uteslutning av företag som genererar minst 50 procent av sina intäkter från hästkapplöpning och lotteri.

- Företag kommer att klassificeras som “Pure Play” och “Non-Pure Play”. Den maximala vikten för en indexkomponent som klassificeras som ”Pure Play” har en maximal vikt på 8 procent.

- Den maximala vikten för en indexkomponent som är klassificerad som ”Non-Pure Play” har en maximal vikt på fem procent-

Rebalansering

För att återspegla det nya urvalet av indexkomponenter som fastställts på selection day justeras index på dagen för rebalansering efter stängning.

Detta genomförs genom att implementera de aktier som bestäms på fixing day baserat på vikterna beräknade på selection day.

Om Fischer Gaming

Fischer Gaming är ett boutique consulting-företag som specialiserat sig på den globala spelindustrin. Företagets grundare och VD, Aaron Fischer, har en omfattande historia inom spelindustrin och är för närvarande Chief Financial and Strategy Officer för onlinespelföretaget Game Play Network i Los Angeles.

Tidigare var han Chief Strategy Officer för MGM Resorts International från 2017 till 2020 där han var ansvarig för företagsstrategi och investerarrelationer. Han var särskilt involverad i viktiga strategiska initiativ som online sportspel och iGaming; budet på en Japan Integrated Resort-licens och andra projekt för att förbättra företagets avkastning och skapa värdes för aktieägarna. Aaron var en ledande aktiesanalytiker vid Goldman Sachs London och CLSA/Citic Securities i Asien där han specialiserade sig på spel, konsument- och lyxvaror. Aaron började sin karriär som revisor på Arthur Andersen i Australien.

Sammanfattning

Sportsbetting och iGaming Index ger exponering för en av de mest spännande tillväxtmöjligheterna i den globala spel- och underhållningssektorn. Regleringsförändringar och enormt uppskattad efterfrågan på sportspel och iGaming förväntas ge en 23x tillväxt i branschen i USA. Branschen förväntas också generera höga marginaler. vara extremt kassaflödesgenerativt tillsammans med en hög avkastning, med tanke på de låga kapitalkravet. Detta index ger en väldiversifierad exponering som inkluderar branschledare med välkända konsumentvarumärken och en mängd leverantörer av ”hackor och spadar” från branschen.

Nyckeldefinitioner

”Sportspel” definieras som satsning av pengar eller något annat värde på resultatet av ett evenemang eller spel.

”IGaming” inkluderar andra former av onlinespel som inkluderar traditionella kasinospel som slots, blackjack, roulette och daglig fantasisport. Det har definierats som ett onlinespel där betalning krävs, monetära priser kan tilldelas och resultatet av spelet bestäms övervägande av en slump. ”

”Non-pure play” -företag genererar eller förväntas generera mindre än 50% av intäkterna från sportspel och onlinespel. Icke-Pure Play-företag inkluderar spelföretag som kasinooperatörer och andra företag, t.ex. leverantörer av spelmaskiner och teknikleverantörer som också tillhandahåller produkter och tjänster till kunder eller andra företag inom den definierade branschen.

“Pure Play” -företag genererar eller förväntas generera minst 50% av sina intäkter från sportspel och onlinespel. Om intäktsströmmarna inte är offentligt tillgängliga kommer företagets huvudsakliga affärssegment att granskas baserat på dess affärsverksamhet, årsredovisningar, företagspresentationer eller andra offentligt tillgängliga källor.

Handla BETS ETF

Sports Betting and iGaming UCITS (ticker: BETS ETF) listas på Londonbörsen. Det gör det möjligt för europeiska investerare att handla denna börshandlade fond genom en mäklare som erbjuder handel på denna marknadsplats, till exempel DEGIRO. Sedan den 15 juni 2021 handlas Sports Betting and iGaming UCITS (ticker: BETS) ocksåpå tyska Xetra och Borsa Italiana. Detta innebär att det går att handla med BETS ETF genom en svensk nätmäklare som DEGIRO, Nordnet eller Avanza.

Största innehav

I BETS ingår många välkända företag, flera av dem svenska. Faktum är att svenska företag är den näst största gruppen, 16,74 procent, efter USA som svarar för 59,43 procent av den geografiska allokeringen.

| Land | Vikt |

| Sverige | 16,74% |

| USA | 59,43% |

| Kanada | 1,78% |

| Norge | 1,00% |

| Australien | 1,62% |

Största innehav

| Aktie | Kortnamn | Valuta | Vikt, % | Land |

| 888 HOLDINGS PLC | 888 | GBP | 1,701910% | Storbritannien |

| BET-AT-HOME.COM AG | ACX | EUR | 0,575898% | Tyskland |

| ASPIRE GLOBAL PLC | ASPIRE | SEK | 0,959674% | Sverige |

| BALLYS CORP | BALY | USD | 2,046740% | USA |

| BETTER COLLECTIVE A/S | BETCO | SEK | 1,082264% | Sverige |

| BETSSON AB | BETSB | SEK | 0,936334% | Sverige |

| BRAGG GAMING GROUP INC | BRAG | CAD | 0,878107% | Kanada |

| BOYD GAMING CORP | BYD | USD | 4,768926% | USA |

| CATENA MEDIA PLC | CTM | SEK | 1,165529% | Sverige |

| CHURCHILL DOWNS INC | CHDN | USD | 4,925578% | USA |

| CAESARS ENTERTAINMENT INC | CZR | USD | 5,558950% | USA |

| DRAFTKINGS INC | DKNG | USD | 7,006389% | USA |

| ENTAIN PLC | ENT | GBP | 8,097813% | Storbritannien |

| EVOLUTION AB | EVO | SEK | 7,420583% | Sverige |

| FLUTTER ENTERTAINMENT PLC | FLTR | GBP | 7,445402% | Storbritannien |

| GAMING INNOVATION GROUP INC | GIG | NOK | 0,998046% | Norge |

| GAN LTD | GAN | USD | 0,971180% | USA |

| GENIUS SPORTS LTD | GENI | USD | 3,296451% | USA |

| GOLDEN NUGGET ONLINE GAMING IN | GNOG | USD | 0,935332% | USA |

| INTERNATIONAL GAME TECHNOLOGY PLC | IGT | USD | 4,017571% | USA |

| KAMBI GROUP PLC | KAMBI | SEK | 1,258496% | Sverige |

| KINDRED GROUP PLC | KINDSDB | SEK | 3,089338% | Sverige |

| LEOVEGAS AB | LEO | SEK | 0,832470% | Sverige |

| MGM RESORTS INTERNATIONAL | MGM | USD | 5,249610% | USA |

| POINTSBET HOLDINGS LTD | PBH | AUD | 1,619365% | Australien |

| PENN NATIONAL GAMING INC | PENN | USD | 4,663736% | USA |

| PLAYTECH PLC | PTEC | GBP | 1,607353% | Storbritannien |

| RUSH STREET INTERACTIVE INC | RSI | USD | 0,973759% | USA |

| SCORE MEDIA AND GAMING INC | SCR | CAD | 0,898178% | Kanada |

| SCIENTIFIC GAMES CORP-A | SGMS | USD | 5,366975% | USA |

| SKILLZ INC | SKLZ | USD | 4,457611% | USA |

| WYNN RESORTS LTD | WYNN | USD | 5,194431% | USA |

Innehaven kan komma att förändras

New to Bitcoin and feeling unsure? You’re not alone. Getting started can feel intimidating, but a few simple tips can help you invest with more confidence and make smarter choices from the start.

Crypto is growing up: 3 things we heard from a recent conference

Crypto’s journey toward mainstream adoption is picking up speed, and the recent Permissionless conference in New York made that more evident than ever. Read the highlights and how they could define the future of crypto.

What keeps Bitcoin mining sustainable and why it matters for investors

If you’re new to Bitcoin (BTC), you might be curious about where it comes from. Unlike traditional money printed by central banks, Bitcoin is generated through a process called mining. The people behind this process are called miners. Understanding what Bitcoin mining is and what makes it sustainable can help you make more informed long-term investment decisions.

Research Newsletter

Each week the 21Shares Research team will publish our data-driven insights into the crypto asset world through this newsletter. Please direct any comments, questions, and words of feedback to research@21shares.com

Disclaimer

The information provided does not constitute a prospectus or other offering material and does not contain or constitute an offer to sell or a solicitation of any offer to buy securities in any jurisdiction. Some of the information published herein may contain forward-looking statements. Readers are cautioned that any such forward-looking statements are not guarantees of future performance and involve risks and uncertainties and that actual results may differ materially from those in the forward-looking statements as a result of various factors. The information contained herein may not be considered as economic, legal, tax or other advice and users are cautioned to base investment decisions or other decisions solely on the content hereof.

Thinking of buying your first Bitcoin? Read these 5 tips first

REX Shares lanserar tre nya covered call ETFer i Europa

WOEE ETF en aktiv globalfond från iShares

Försvarsfondernas ägande i SAAB ökar kraftigt

EDFS ETF spårar den europeiska försvarssektorn

De bästa ETFer som investerar i europeiska utdelningsaktier

YieldMax® lanserar sin andra produkt för europeiska investerare

Big News for Nuclear Energy—What It Means for Investors

Nya börshandlade produkter på Xetra

3EDS ETN ger tre gånger den negativa avkastningen på flyg- och försvarsindustrin

-

Nyheter1 vecka sedan

Nyheter1 vecka sedanDe bästa ETFer som investerar i europeiska utdelningsaktier

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanYieldMax® lanserar sin andra produkt för europeiska investerare

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanBig News for Nuclear Energy—What It Means for Investors

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanNya börshandlade produkter på Xetra

-

Nyheter3 veckor sedan

Nyheter3 veckor sedan3EDS ETN ger tre gånger den negativa avkastningen på flyg- och försvarsindustrin

-

Nyheter1 vecka sedan

Nyheter1 vecka sedanNordea Asset Management lanserar nya ETFer på Xetra

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanHANetfs VD Hector McNeil kommenterar FCAs kryptonyheter

-

Nyheter1 vecka sedan

Nyheter1 vecka sedanSvenska investerare — 21Shares Nasdaq Stockholm-sortiment har just blivit starkare