Nyheter

Market underpricing UK rate hike risk

ETF Securities FX Research: Market underpricing UK rate hike risk

Highlights

- Upside potential for GBP despite the mixed message from the Bank of England (BOE) keeping volatility elevated. The market is underpricing the chance of rate hikes.

- Rising real interest rates will continue to be supportive of Sterling (GBP) in coming months.

- Positioning for GBP against the USD has rebounded to historical averages, but remains depressed against the Euro, which is an overcrowded trade.

One year on from the last rate cut, the Bank of England (BOE) has kept rates on hold, with the MPC voting 6-2 in favour of the decision (roughly the same as last month). Although policy remains unchanged, GBP should remain supported by what is expected to be a tighter policy path in 2017/2018. Indeed, Governor Carney has indicated that policy may need to be tightened at a faster rate than the market is currently pricing.

(click to enlarge)

Currency volatility has made a persistent move upward in recent weeks, largely to the detriment of the Pound. A relatively more hawkish policy stance by the UK central bank will support the Pound as Brexit negotiation outcomes remain obscure. As we believe inflation will remain stubbornly high, real interest rate differentials will become an increasingly important indicator for FX markets. Rising real interest rate differentials in the US continue will remain a supportive influence for GBP.

Cautious Bank of England

While a decidedly cautious tone was struck by Governor Carney at the BOE press conference last week, tighter policy is coming: if UK economic growth continues at the rate the BOE has forecast, the market is underpricing the amount of policy tightening that is necessary. The market is only pricing in a 50% chance of a rate hike by end March 2018.

The UK economy remains somewhat mixed after the EU Referendum, with the unemployment rate at pre-crisis levels and evidence that both the manufacturing and services sector are growing in a robust manner. However, negative real wage growth and plummeting consumer confidence remain a constraint for the household sector.

The reason for the additional BOE stimulus (a rate cut and additional asset purchases) a year ago was appropriately forward looking, as Governor Carney quoted; ‘the weaker medium-term outlook for activity…[will lead to] an eventual rise in unemployment’. The UK central bank seems to have become less proactive since then, highlighting that the UK is currently ‘in the teeth’ of the squeeze for households and both consumption growth and business investment will improve further in coming months.

Inflation pressure mounts

Meanwhile, inflation remains elevated in the UK and well above the BOE’s target. The longer this continues, the greater the chance of expectations becoming unanchored, especially if energy price gains are sustained. While inflation hasn’t surprised to the upside in recent months, market implied inflationary expectations remain elevated (well above a year ago), and above other major economies. Inflation is expected to remain above the BOE target for the entire BOE forecast horizon, a period of three years. The BOE’s credibility is on the line, because it appears to be becoming less proactive with policy and reacting to events that have, and may not, occur i.e. a hard Brexit.

(click to enlarge)

Current BOE policy remains extremely accommodative. There may be uncertainties around the Brexit negotiations, but we believe emergency interest rate settings do not seem appropriate. Indeed, Governor Carney notes that there are limits to what monetary policy can do relating to the Brexit situation. We expect that negotiations surrounding Brexit will remain in flux and given there is unlikely to be significant progress made, the worst-case scenario has already been digested by the FX market. In turn, the BOE is likely to unwind their Brexit induced rate cut from last year in H2 2017.

The key sentence in the BOE’s Monetary Policy Summary report is ‘The combination of high rates of profitability, especially in the export sector, the low cost of capital and limited spare capacity, supports investment by UK firms over the forecast period, offsetting the effect of continued uncertainties around Brexit’. Surely if the economic uncertainty surrounding Brexit is offset, then the 2016 rate cut and additional stimulus should be unwound…if not in 2017, then when?

Just a day after the meeting, the mixed messages to the market continued: Deputy Governor Broadbent, who voted to keep rates unchanged, commented that ‘there may be some possibility for interest rates to go up a little bit’. This is reminiscent of the previous meeting that was interpreted dovishly by the market, only for the ‘doves’ to signal tighter policy was an issue that needed discussion only days later. Mixed messages are an impediment for economic stability and consumer and business confidence.

Meanwhile, gradually tighter Fed policy is already priced into the USD. Although we expect the broad USD index is in a bottoming process, a move higher will be gradual and predicated on political risks fading, something that will take time given investor focus on the incompetence of the Trump administration. Accordingly, the more hawkish policy that we expect from the BOE will bring forward expectations of a rate hike in the fourth quarter and forcing GBP higher in H2 2017.

How the market is positioned

GBP positioning has rebounded against the USD, in line with the recent more bullish performance and is now at levels consistent with longer-term historical averages.

(click to enlarge)

Against the Euro, GBP looks extremely attractively priced – hovering around record low levels. We feel that the Euro strength is at risk of an unwind as the ECB remains conservative in its policy approach in the face of the elevated Euro. Compared to historical long-term averages, positioning for the Euro highlights a very overcrowded trade.

The bottom line…

The mixed messages from the BOE are confusing investors and keeping GBP volatility elevated. We expect the BOE to unwind its Brexit-induced rate cut of 2016 in the second half of 2017, but not to remove its balance sheet stimulus from the economy. GBP will benefit from tighter policy settings. We believe that GBP will consolidate above the 1.30 level and potentially break to the upside, approaching 1.35.

For more information contact:

ETF Securities Research team

ETF Securities (UK) Limited

T +44 (0) 207 448 4336

E info@etfsecurities.com

Important Information

This communication has been issued and approved for the purpose of section 21 of the Financial Services and Markets Act 2000 by ETF Securities (UK) Limited (“ETFS UK”) which is authorised and regulated by the United Kingdom Financial Conduct Authority (the “FCA”).

Dogecoin’s performance and staying power across multiple market cycles suggest it is not “just another one of those memecoins”.

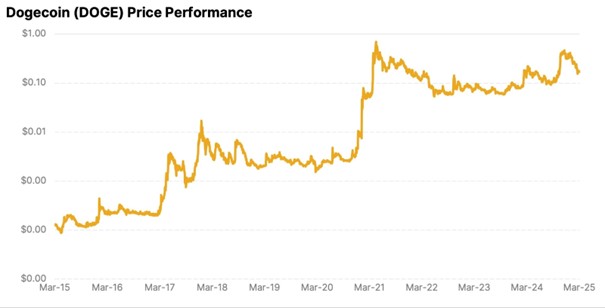

Over the past decade, DOGE has outperformed even Bitcoin, delivering over 133,000% in returns, nearly 1,000x BTC’s gains in the same period. Despite deep drawdowns during bear markets, Dogecoin has shown remarkable structural resilience.

Following each major rally, it has consistently formed higher lows, a pattern of long-term appreciation and compounding strength.

Historically, Dogecoin has closely mirrored Bitcoin’s movements, often peaking a few weeks after. While 2024 saw Bitcoin dominate headlines following landmark ETF approvals, DOGE still followed its trajectory, though it has yet to stage its typical delayed breakout.

As macro uncertainty continues to fade and momentum returns to the market, retail participation is likely to accelerate, setting up conditions in which Dogecoin has historically thrived.

At the same time, regulatory clarity around Dogecoin has improved. The SEC recently confirmed that most memecoins are not considered securities, comparing them to collectibles. Additionally, they clarified that proof-of-work rewards, like those earned from mining DOGE, also fall outside that scope. These developments further legitimize Dogecoin’s role in the ecosystem, potentially setting the stage for its next paw up, especially as it now holds a firm base around $0.17, nearly 3x its pre-rally level before reaching a new all-time high in the last cycle.

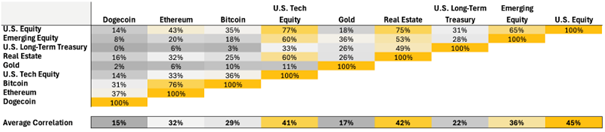

In addition to its long-term performance, Dogecoin stands out as an asset that behaves asymmetrically, offering investors a rare source of uncorrelated returns across both traditional and crypto portfolios. With an average correlation of just 15% to major assets, DOGE’s price action remains largely detached from broader macroeconomic trends, reinforcing its value as a true diversification tool.

Dogecoin demonstrates significant independence within the crypto market, with its correlation to Bitcoin at only 31% and to Ethereum at 37%. This divergence stems from unique capital flow dynamics, where higher-beta assets like DOGE tend to rally after blue-chip crypto assets reach major milestones.

While Bitcoin slowly evolves into a digital store of value and Ethereum powers decentralized infrastructure, Dogecoin remains largely a cultural asset, thriving on narrative momentum and crowd psychology, offering explosive upside when risk appetite surges.

For investors seeking an upside without mirroring the behavior of core holdings, Dogecoin offers a compelling case. Its ability to decouple from market trends while tapping into more speculative surges makes it a powerful, though unconventional, addition to a portfolio with wildcard potential.

Research Newsletter

Each week the 21Shares Research team will publish our data-driven insights into the crypto asset world through this newsletter. Please direct any comments, questions, and words of feedback to research@21shares.com

Disclaimer

The information provided does not constitute a prospectus or other offering material and does not contain or constitute an offer to sell or a solicitation of any offer to buy securities in any jurisdiction. Some of the information published herein may contain forward-looking statements. Readers are cautioned that any such forward-looking statements are not guarantees of future performance and involve risks and uncertainties and that actual results may differ materially from those in the forward-looking statements as a result of various factors. The information contained herein may not be considered as economic, legal, tax or other advice and users are cautioned to base investment decisions or other decisions solely on the content hereof.

Börshandlade produkter som ger exponering mot Sui

The Dogecoin case study: How to value memecoins

MWOA ETF köper aktier i industriföretag

XENIX ETF AWARDS Nordics 2025, Stockholm

JLOD ETF investerar i lokala obligationer från emerging markets

Bitcoin var den bäst presterande tillgången men…

Sju börshandlade fonder som investerar i försvarssektorn

Världens första europeiska försvars-ETF från ett europeiskt ETF-företag lanseras på Xetra och Euronext Paris

21Shares bildar exklusivt partnerskap med House of Doge för att lansera Dogecoin ETP i Europa

HANetfs Tom Bailey om framtiden för europeiska försvarsfonder

-

Nyheter1 dag sedan

Nyheter1 dag sedanBitcoin var den bäst presterande tillgången men…

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanSju börshandlade fonder som investerar i försvarssektorn

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanVärldens första europeiska försvars-ETF från ett europeiskt ETF-företag lanseras på Xetra och Euronext Paris

-

Nyheter4 veckor sedan

Nyheter4 veckor sedan21Shares bildar exklusivt partnerskap med House of Doge för att lansera Dogecoin ETP i Europa

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanHANetfs Tom Bailey om framtiden för europeiska försvarsfonder

-

Nyheter1 vecka sedan

Nyheter1 vecka sedanFastställd utdelning i MONTDIV april 2025

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanInvestera i Polen med börshandlade fonder

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanFranklin Templeton lanserar två nya kärn-UCITS-ETFer för europeiska investerare