Nyheter

How Would Celsius’ Liquidation Impact the Crypto Market?

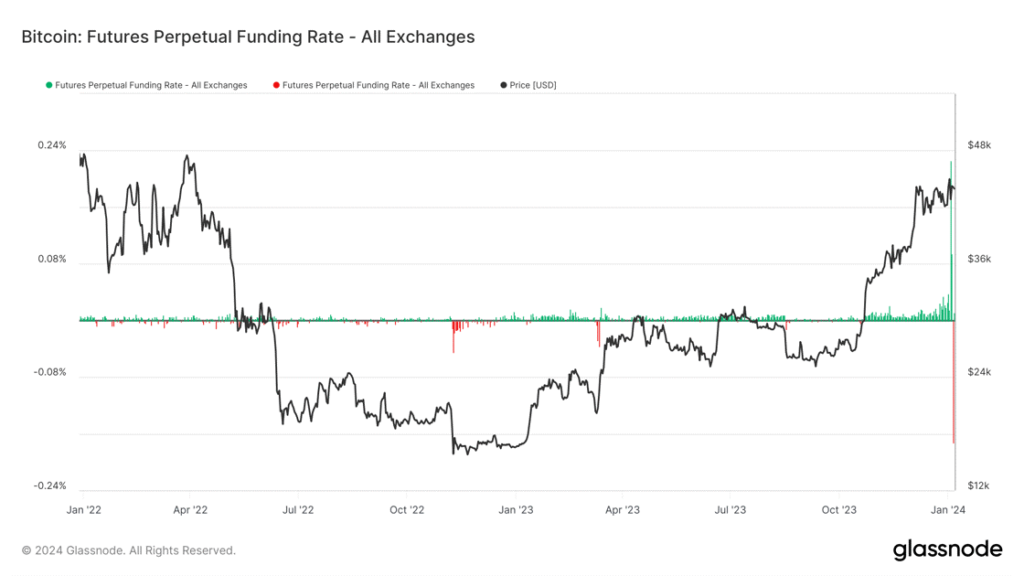

On January 3, crypto-focused financial services platform MatrixPort published a report speculating that the Securities and Exchange Commission (SEC) could reject applications for a spot Bitcoin ETF this month and approve them later in the year because of political headwinds within the agency. Although Bitcoin dropped by 4.8% following the report, the soaring open interest combined with the high funding rate, whose spike can be seen below in Figure 1, also contributed to the short-lived decline. This implied the market was overleveraged and required a corrective flush.

Figure 1: BTC Funding Rate

Source: Glassnode

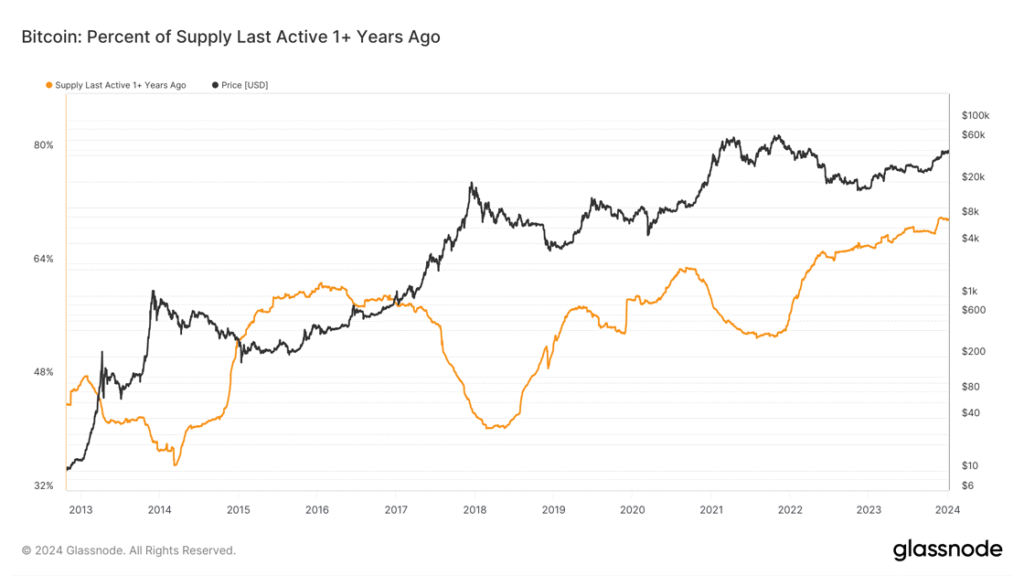

Conversely, progress seems to prevail as Goldman Sachs aims to be an authorized participant for Blackrock and Grayscale, while the SEC met with the NYSE, Nasdaq, and CBOE to discuss amendments triggered in the 11th hour. In addition, multiple asset issuers also filed 8A forms last week, which could imply that applicants have overcome significant hurdles from the agency’s point of view. In summary, the outlook for Bitcoin appears robust, with long-term investors—those who have held the asset for over a year—reaching the highest levels (~67%) in Bitcoin’s 15-year history, as seen below in Figure 2. This underscores the strong conviction in the asset over the long term

Figure 2: Percentage of BTC supply moved over a year ago

Source: Glassnode

Celsius Begins its Liquidation Procedure

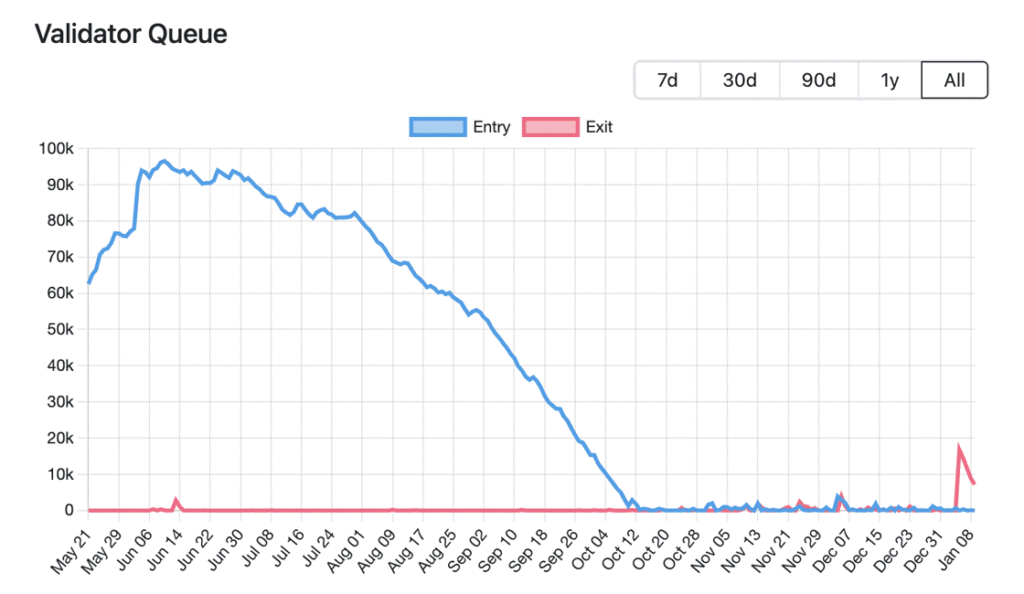

The bankrupt lender submitted a request to unstake 206K ETH, as part of its efforts to pay back creditors. Representing 1.9% of the total staked ETH ($450M), the request could add some selling pressure over the coming weeks. However, it’s worth noting that Celsius will allow in-kind redemptions, meaning it’ll distribute BTC and ETH holdings to users directly, so the company won’t have to sell the underlying to meet its obligations. Finally, the decision is also causing a significant surge in the ETH exit validator queue, as shown in Figure 3, which would take close to 14 days to fully exit and withdraw now while contributing to an increase in staking yield, bringing it up from ~3.088% to ~3.117%.

Figure 3: Ethereum Validator Queue

Source: Ethereum Validator Queue

Arbitrum Enhancing Customization Options

Arbitrum has announced that its custom blockchain development solution, Orbit, will allow networks building on top of it to designate their tokens as gas currencies instead of ETH, once they meet a specific criteria. The upgrade ensures that networks built on top of Orbit can create utility for their token while offering advanced features like gas subsidy. This level of flexibility puts Arbitrum on par with Cosmos, which makes it a more favorable option amongst developers. However, with the announcement of Arbitrum’s optimized architecture and the forthcoming implementation of Ethereum’s Dencun upgrade expected in February, there has been a resurgence of interest in Arbitrum, as well as other high-beta plays on the Ethereum network, such as Optimism and Lido, seen below in figure 4. Thus, we expect the assets mentioned above to perform well leading into the upgrade.

Figure 4: Price Action of ETH vs ETH Beta(s) vs SOL

Source: TradingView

This Week’s Calendar

Source: Forex Factory, CoinMarketCal

Research Newsletter

Each week the 21Shares Research team will publish our data-driven insights into the crypto asset world through this newsletter. Please direct any comments, questions, and words of feedback to research@21shares.com

Disclaimer

The information provided does not constitute a prospectus or other offering material and does not contain or constitute an offer to sell or a solicitation of any offer to buy securities in any jurisdiction. Some of the information published herein may contain forward-looking statements. Readers are cautioned that any such forward-looking statements are not guarantees of future performance and involve risks and uncertainties and that actual results may differ materially from those in the forward-looking statements as a result of various factors. The information contained herein may not be considered as economic, legal, tax or other advice and users are cautioned to base investment decisions or other decisions solely on the content hereof.

Produktuppdatering: Toncoin blir Gram

CEMN ETF följer de största företagen från utvecklade marknader

Nya ETF- och ETP-noteringar den 16 juni 2026 på Deutsche Börse

RCEG ETF spårar eurodenominerade statsobligationer utfärdade av eurozonens medlemsstater

JEQE ETF en månadsutdelare som förvaltas aktivt

USA satsar 2 miljarder dollar på kvantdatorer – så kan investerare dra nytta av utvecklingen

Extrema skillnader: Varför presterar Europas kvantdator-ETFer så olika?

Fastställd utdelning i MONTDIV maj 2026

Varför Plus500 är en dröm för finans-affiliate

ASWF ETF är en aktivt förvaltad fond som investerar i Kanada

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanUSA satsar 2 miljarder dollar på kvantdatorer – så kan investerare dra nytta av utvecklingen

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanExtrema skillnader: Varför presterar Europas kvantdator-ETFer så olika?

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanFastställd utdelning i MONTDIV maj 2026

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanVarför Plus500 är en dröm för finans-affiliate

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanASWF ETF är en aktivt förvaltad fond som investerar i Kanada

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanQQCC ETF följer företag världen över som är aktiva inom kvantberäkning

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanETFer för fotbolls-VM 2026

-

Nyheter3 veckor sedan

Nyheter3 veckor sedan21shares produkter nu finns tillgängliga hos Revolut