Nyheter

Cyclical Assets In Focus

ETFS Multi-Asset Weekly A Turbulent Week for Investors Cyclical Assets In Focus

Highlights

Industrial metals staged a modest recovery after China posts upside surprise.

Global equities advance.

USD and CAD to outperform

Cyclical assets were back in focus last week, with industrial metals and global equities seeing modest gains. Better-than-expected Chinese Q3 GDP and industrial production data lifted investor sentiment and contributed to the advance. The FOMC meeting and US Q3 GDP growth data will likely be the focus for global markets this week, with industrial metals and US equities likely to benefit from improving growth in the country and the US Dollar likely to be buoyed by rising expectations for tighter Fed policy in 2015.

Commodities

Industrial metals staged a modest recovery after China posts upside surprise. Aluminium, palladium and lead all posted gains last week, rising by 4.1%, 4.0% and 2.9% respectively, as China’s Q3 GDP and industrial production surprised on the upside. Investors are starting to realise that the recent correction has been excessive and cyclical commodities like industrial metals are well positioned to benefit from robust activity in China and the US. Meanwhile, after rising over 70% since the beginning of the year, Arabica coffee prices slumped 11% last week on rainfall prospects in Brazil. Drought and irregular rain in Brazil, the world’s top producer, have hurt the prospect for 2015 crop. However, with rains resuming the flowering process has started for the 2015 crop, but analysts are divided in their opinion as to the extent the earlier disruptions will cause irrevocable damage to the crop.

Equities

Global equities advance. The FTSE MIB, the DAX, and the FTSE100 rallied strongly last week, after Chinese economic growth data boosted optimism over the global economic outlook. The rally however might be short-lived after 24 European banks failed the European Banking Authority (EBA) stress tests over the weekend. The Russell 2000 also gained last week, rising 2.8%, as US stock earnings beat expectations. With Q3 US GDP growth figures coming out on Thursday and likely confirming the steady pace of expansion of the US economy, US equities should continue to benefit. Meanwhile, continued weakness in the gold price weighed on the DAXglobal Gold Miners Index last week, erasing all the gains so far accumulated during the year. We anticipate this to be temporary and for gold miners to resume their growth as valuations remain well below historical levels.

Currencies

USD and CAD to outperform. Central Banks will again dominate currency landscape this week, with the US Federal Reserve, the Bank of Japan and the Reserve Bank of New Zealand all holding policy meetings. While most central banks have been trying to talk down their currencies in recent months, the US Fed and the Bank of Canada have been the exception. We expect this week’s FOMC meeting to be the catalyst for a stronger USD. The Fed will likely cease its bond buying this month, in line with previous guidance. Its forward guidance will be the main focus and any changes to the language will prompt a swift reaction for USD. We remain bullish on the outlook for the USD and feel that this week’s GDP release will again confirm that the recovery is on track in the US. The Canadian dollar (CAD) should be one of the best performers in coming months, with an improving domestic economy supporting rate differentials and a stabilisation in oil prices. CAD is significantly tied to oils’ fortunes, and this source of downward pressure will be gradually removed.

Important Information

This communication has been issued and approved for the purpose of section 21 of the Financial Services and Markets Act 2000 by ETF Securities (UK) Limited (”ETFS UK”) which is authorised and regulated by the United Kingdom Financial Conduct Authority (”FCA”).

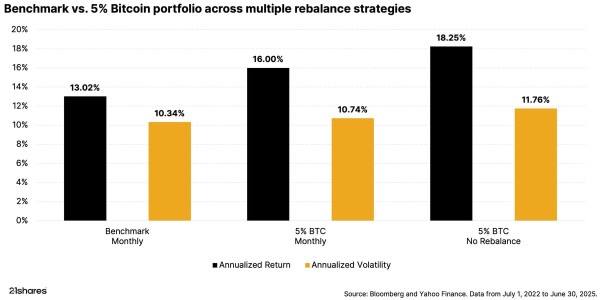

Many investors wonder: If I add Bitcoin to my portfolio, what difference will it make? To answer these questions, we analyzed data to see how even a small Bitcoin allocation can impact your overall investment returns and risk.

It’s Crypto Week. Keep an eye on these bills

This week, the US House of Representatives will host “Crypto Week,” a focused effort to create clearer rules for digital assets. If these new laws pass, they could help investors feel more confident about entering the crypto market. The historic Crypto Week will likely benefit crypto lending projects like Aave, which has recently exceeded $45 billion in total value locked. Take a closer look at what’s on Congress’s agenda and why it matters for the future of crypto.

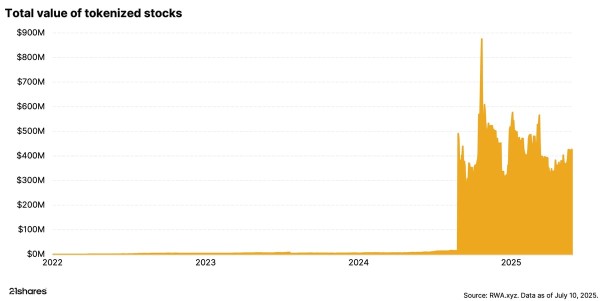

Turning stocks into tokens? Why it’s cool, but complicated

Crypto keeps evolving, and one clear use case is tokenization, turning real-world assets like property, investment funds, or stocks into digital tokens on the blockchain. Tokenized stocks are grabbing headlines right now as they let you trade company shares anytime, anywhere, making investing easier and faster. But it’s still early days, and there are challenges ahead. Explore how stock tokenization works and what’s holding it back.

Research Newsletter

Each week the 21Shares Research team will publish our data-driven insights into the crypto asset world through this newsletter. Please direct any comments, questions, and words of feedback to research@21shares.com

Disclaimer

The information provided does not constitute a prospectus or other offering material and does not contain or constitute an offer to sell or a solicitation of any offer to buy securities in any jurisdiction. Some of the information published herein may contain forward-looking statements. Readers are cautioned that any such forward-looking statements are not guarantees of future performance and involve risks and uncertainties and that actual results may differ materially from those in the forward-looking statements as a result of various factors. The information contained herein may not be considered as economic, legal, tax or other advice and users are cautioned to base investment decisions or other decisions solely on the content hereof.

A slice of Bitcoin gives a big portfolio boost

LYOR ETF är en aktiv satsning på ”over night lån”

WisdomTree noterar hävstångsprodukter på Xetra

VALOUR TRX SEK spårar priset på kryptovalutan Tron

Börshandlade fonder för globala utdelningsaktier

De bästa ETFer som investerar i europeiska utdelningsaktier

Nordea Asset Management lanserar nya ETFer på Xetra

Svenska investerare — 21Shares Nasdaq Stockholm-sortiment har just blivit starkare

De bästa ETFerna med fokus på momentum

Hetaste investeringstemat i juni 2025

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanDe bästa ETFer som investerar i europeiska utdelningsaktier

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanNordea Asset Management lanserar nya ETFer på Xetra

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanSvenska investerare — 21Shares Nasdaq Stockholm-sortiment har just blivit starkare

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanDe bästa ETFerna med fokus på momentum

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanHetaste investeringstemat i juni 2025

-

Nyheter2 veckor sedan

Nyheter2 veckor sedan12 000 artiklar om börshandlade fonder

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanPrimer: Injective, infrastructure for global finance

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanREX Shares lanserar tre nya covered call ETFer i Europa