Nyheter

Exploits, Liquidations, and What Lies Beneath the Surface

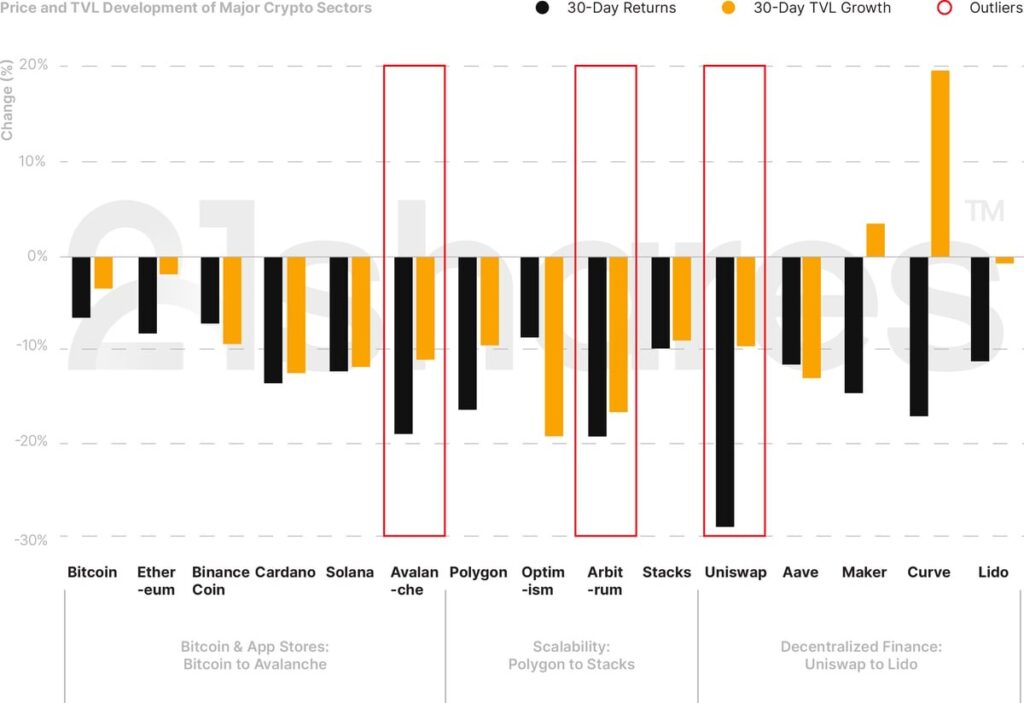

Crypto’s market cap declined by 6% over the past month. The main reason for this drop is the market’s low volatility, following Curve’s $62M exploit on July 30, until August 17. A combination of events could have influenced this sell-off, including a possible upcoming interest rate hike, the Ripple case getting longer, and rumors about SpaceX liquidating its Bitcoin holdings. Bitcoin and Ethereum fell by 6.62% and 8.19%, respectively, over the past month. The largest decentralized exchange by total value locked (TVL), Uniswap, suffered the most in August, declining by 29.05%. On the other hand, Curve’s TVL rebounded, growing by 19.78% over the past month, indicating that the 65.9% recovered funds remain on-chain.

Figure 1: Price and TVL Development of Major Crypto Sectors in August

Source: 21shares, CoinGecko, DeFi Llama. Data as of August 30 close.

5 Trends to Remember from August

• Declining market activity, FUD, and macro backdrop fueling the largest liquidations since FTX

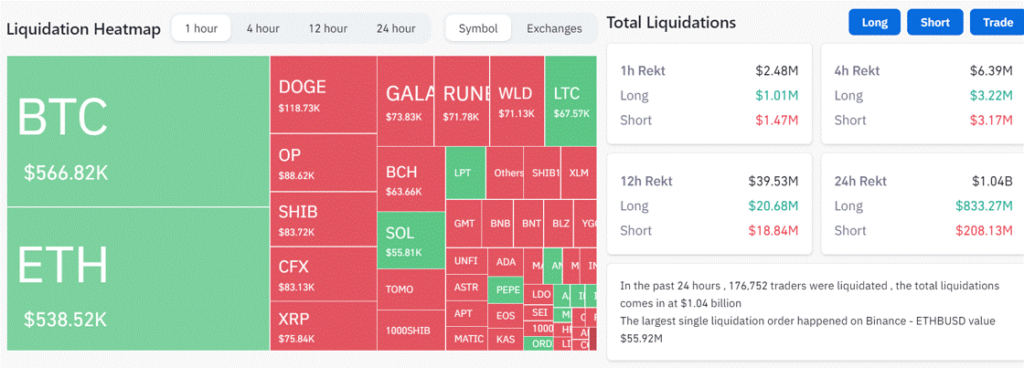

In late August, the crypto market experienced approximately $1.04 billion in liquidations, with around $833 million from long positions. Various factors fueled the chain of liquidations, notably the Fed’s minutes emphasizing ongoing inflation and the potential for more interest rate hikes. This, combined with elevated US long-term bond yields and a hawkish Fed stance, prompted short-term risk aversion that impacted both the crypto and stock markets. This relationship is highlighted by Bitcoin’s renewed positive correlation with S&P 500 and Nasdaq, reaching 0.8 and 0.72, respectively, and implying that the three markets are once again moving in tandem.

The downturn was also exacerbated by erroneous reports of SpaceX liquidating its Bitcoin holdings. While many speculated about a potential sell-off, it’s important to note that write-downs are a standard accounting practice and do not necessarily imply that the investments have been sold or liquidated. In addition, global markets experienced a mild shock due to news of Evergrande’s bankruptcy filing under US Chapter 15, raising concerns about its impact on the global real estate market.

Finally, the SEC’s ability to appeal specific judgments about the Ripple case added to the negative sentiment, which we will briefly touch on next. Although August’s events pale in comparison to the gravity of the FTX debacle, Bitcoin’s annualized volatility recently hit its lowest level in over five years, which indicated an anticipated market breakout. That said, the market modestly rebounded on the news of a Federal Appeals Court ruling siding with Grayscale in their case against the SEC on converting GBTC into a spot ETF.

Figure 2: Liquidations Across the Crypto Market

Source: Coinglass (on August 17)

• Ripple Continues Saving Grace by Forging New TradFi Partnerships

On August 18, the SEC filed an interlocutory appeal against the inconclusive summary order in the Ripple case issued by Federal Judge Analisa Torres on July 13. The appeal primarily objects to the court’s view that the programmatic sales of XRP (on exchanges) are not considered securities, highlighting a disagreement among district courts regarding the controlling issues. In response, XRP fell by around 30% over the past month. Ripple has until September 1 to submit a response to the SEC’s appeal. There are no definite dates for the trial yet; Judge Torres suggested that the court would be in session later in the second half of 2024. Until then, we expect XRP to experience speculation to drive its price movement while Ripple continues to secure strategic partnerships to enforce its value proposition as a crypto-native software solution for players in traditional finance. In its latest move, Ripple is collaborating with fintech giant MasterCard and ConSensys, among others, to build a central bank digital currency (CBDC) program to support central banks and governments in pursuing a digital currency. The program will explore the design of CBDCs, interoperability, and limitations.

• Did Tether’s Profit Surge Lure PayPal’s Venture into Stablecoins?

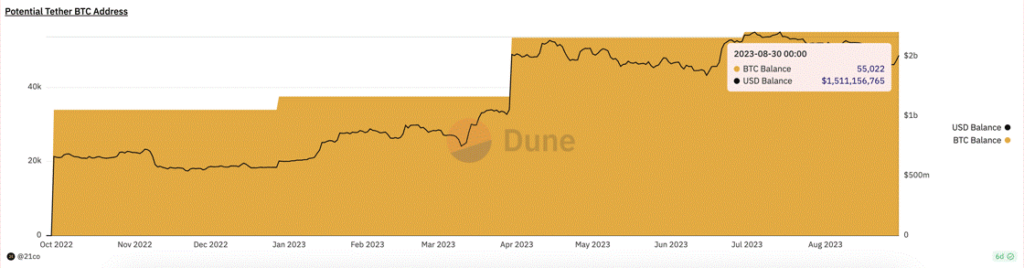

The issuer behind the biggest US-dollar stablecoin is now the 11th-largest holder of Bitcoin. Following their announced plans to convert profits into Bitcoin, Tether has amassed 55K BTC (~$1.6B). The latest attestation report shows a ~$800M rise in excess reserves in Q2, reaching $3.3B. This significant development enhances demand for Bitcoin’s role in corporate treasury management. Conversely, Tether should convert surplus BTC and profits into cash to fortify the company’s resilience against unforeseen issues. For context, Tether’s cash reserves dropped from $5.3B in December 2022 to $90M in Q2 23, a concern for an $85B stablecoin, despite access to liquid instruments like US treasuries, and REPOs. Finally, although not confirmed by Tether, the wallet holdings align with the issuer’s quarterly holdings. That said, Tether’s thriving business endeavor might have piqued the curiosity of traditional financial behemoths cautiously entering the stablecoin landscape.

Figure 3: Tether’s Potential BTC Holdings

Source: 21.co on Dune

On August 7, Paypal partnered with stablecoin issuer Paxos to launch their own USD-pegged stablecoin, PYUSD, built on Ethereum and fully backed by U.S. dollar deposits, short-term U.S. treasuries and similar cash equivalents. According to the press release, eligible U.S. customers will be able to pay for their purchases using PYUSD in the same manner that Gnosis Pay announced it will empower European customers to pay for their purchases with Monerium’s euro-pegged stablecoin (EURe) via its Visa card, with a convergence mechanism running in the backend. This trend aims to boost mass adoption by solving two ailing issues stifling the industry, by providing users with a familiar user interface while being compliant to regulations. Moreover, onboarding more traditional players from the second generation of the internet shows the institutional appetite for the stablecoin subsector, whose market cap is valued at $125B, with USDT dominating by 66%. More traditional players, especially those with existing tools to their advantage, will likely follow suit, aiming to topple this dominance in their favor. In the grand scheme of things, the more regulated players in the space, the healthier the market.

• Coinbase Scores Two Points for Adoption

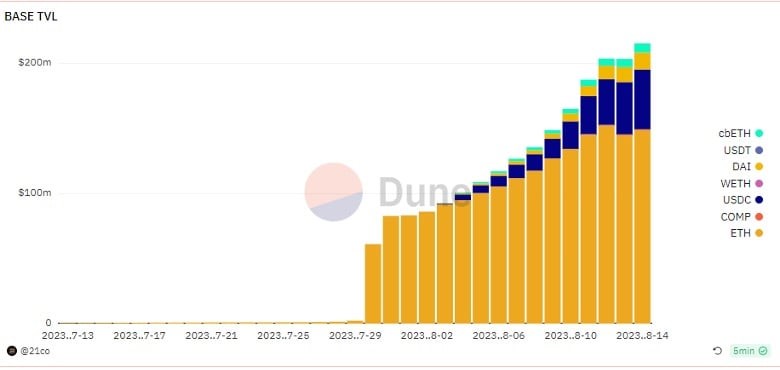

After a year in application, Coinbase won regulatory approval to offer crypto futures to its retail clients in the U.S. According to a recent study, 58.8 million Americans hold crypto, up 18% from the previous year. This move can bring more American retail investors into crypto, thanks to regulations, an essential element for mass adoption. The trading volume of the global crypto derivatives market represents almost 75% of the entire crypto market. The Coinbase Derivatives Exchange has established a deep liquidity pool with $4.7B worth of BTC and $2B worth of ETH futures traded in notional volume in 2023. We’re also seeing more adoption on the infrastructure level, with Coinbase’s scaling solution Base launching on Ethereum on August 9, attracting $226.59M in assets under management.

• Visa’s Experimentations to Abstract the Complexity of Crypto

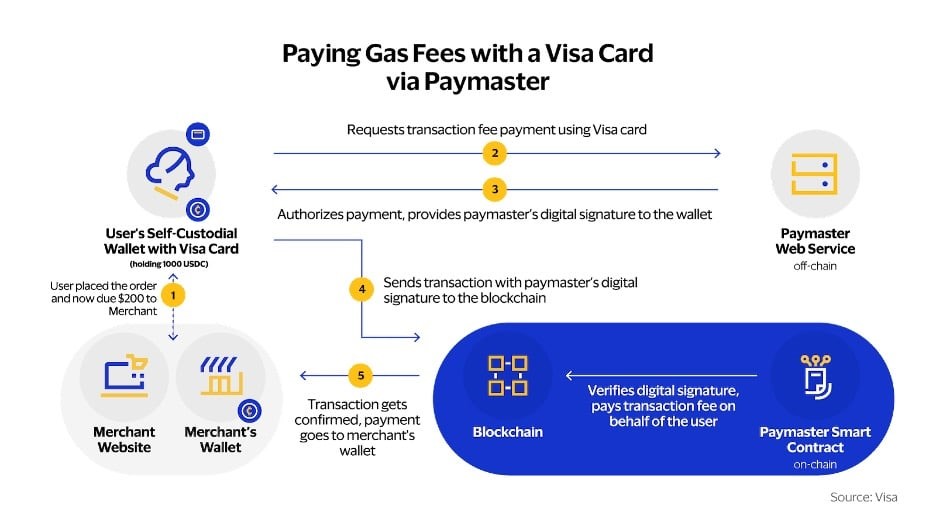

After Visa initially announced their experiment utilizing Account Abstraction (AA) to streamline crypto native payments on top of Ethereum back in May, the financial services giant revealed the piloted project’s latest updates. Namely, leveraging the ERC-4337 standard, more commonly known as AA, Visa abstracted the process of paying gas fees in ETH using a credit card. As AA allows for asset conversion in the backend, users will not have to worry about holding the right native token to pay for transaction costs. Thus, users would be met with the flexibility of paying with their cards or any other ETH-based token, and the AA smart contract will simply trigger the conversion via what’s known as a paymaster smart contract that sponsors transactions on users’ behalf. That said, Visa’s experiment has the power and potential to transform the crypto native ecosystem and make them more accessible using the average users’ traditional financial instruments, and could, thus, catalyze the adoption of native blockchain applications without users necessarily becoming aware of the technical intricacies.

Figure 4: Visa’s Process to Abstract ETH Gas Fees

Source: Visa

What to Expect

• OP Stack Establishing its Presence and EVM Maintaining Dominance

Optimism’s modular framework, OP Stack, is maintaining its position as the leading scaling solution for Ethereum, with established players like Binance, Coinbase, Worldcoin and A16Z all opting to leverage the solution to build their customized networks. Coinbase launched public access to its scaling solution dubbed Base in August, leveraging the OP Stack. The scaling solution Base experienced tremendous growth, amassing close to ~$275M in AuM around two months and generating $3.2M in revenue, of which Coinbase will share 2.5% of the total amount with the OP Stack to help develop the broader Optimism ecosystem, while welcoming the deployment of some of DeFi blue chips like Uniswap, Aave, 1Inch and others.

Figure 5: Coinbase Scaling Solution AuM

Source: 21.co on Dune

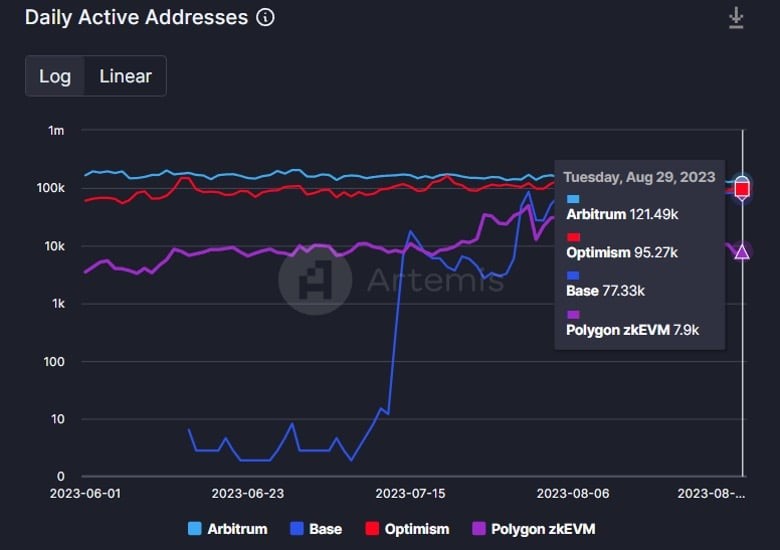

While the initial shift was prompted by a meme coin frenzy, the ongoing surge in user activity signifies enthusiasm for the Ethereum ecosystem. Moreover, Base holds significant growth potential due to Coinbase’s extensive 110M user base, which can seamlessly transition to the on-chain ecosystem through user-friendly interfaces. In line with this, Coinbase revealed “on-chain summer”, an initiative to introduce users to Base’s vibrant ecosystem and the network’s enhanced performance. The program was a success as Base logged close to 136K daily active users at peak, surpassing Optimism and Polygon. It remains to be seen whether Base can sustain its user base in the long run. However, it will certainly be a key network to look out for over the next few months.

Finally, the enthusiasm for the Ethereum ecosystem has also reverberated across the wider smart contract landscape. For instance, Fantom is considering building an optimistic-based rollup linking to Ethereum, while Celo proposed pivoting into an ETH scaling solution using the OPStack. Binance has similarly launched its own ETH scaling solution dubbed OpBNB, aligning its technical approach with Base. Conclusively, all three decisions stem from the desire to harness Ethereum’s network effects and its liquidity amidst the declining on-chain activity.

Figure 6: Daily Active Addresses of the Four Leading Ethereum Scaling Solutions

Source: Artemis.xyz

• Where Are Stablecoins Headed?

Coinbase is doubling down on the stablecoin space by taking an equity stake in Circle. While it may not immediately impact investors, as Circle will still be issuing USDC, the move speaks volumes of the level of consolidation the community has reached. The more competition heats up in this space, the tougher it will be for smaller stablecoins to shine, which – in theory – should filter out the ones with weak underlying technology or little added value. Contrarily, with a clear added value, PayPal’s new stablecoin will take some time to catch up with the rally, especially since 90% of the stablecoin’s supply is still in addresses that belong to its issuer, Paxos Trust.

More legal clarity on stablecoins in the U.S. is on the way, and it could be PayPal’s golden ticket to set sail. On August 28, representatives from the Financial Services Committee sent a letter to Federal Reserve Board Chairman Jerome Powell objecting to the Fed’s recent “Creation of Novel Activities Supervision Program,” published a day after PayPal’s PYUSD launch. The supervisory guidelines aim at monitoring stablecoin activities engaged by banks under the Fed’s jurisdiction. In the letter, the Committee wrote that the Fed’s move undermines Congress’ progress on legislation to establish a regulatory framework for payment stablecoins. We believe the Committee’s letter indicates a political will to reach legal clarity, just like the Fed’s move was a strong indicator that stablecoins will inevitably soar in mass adoption.

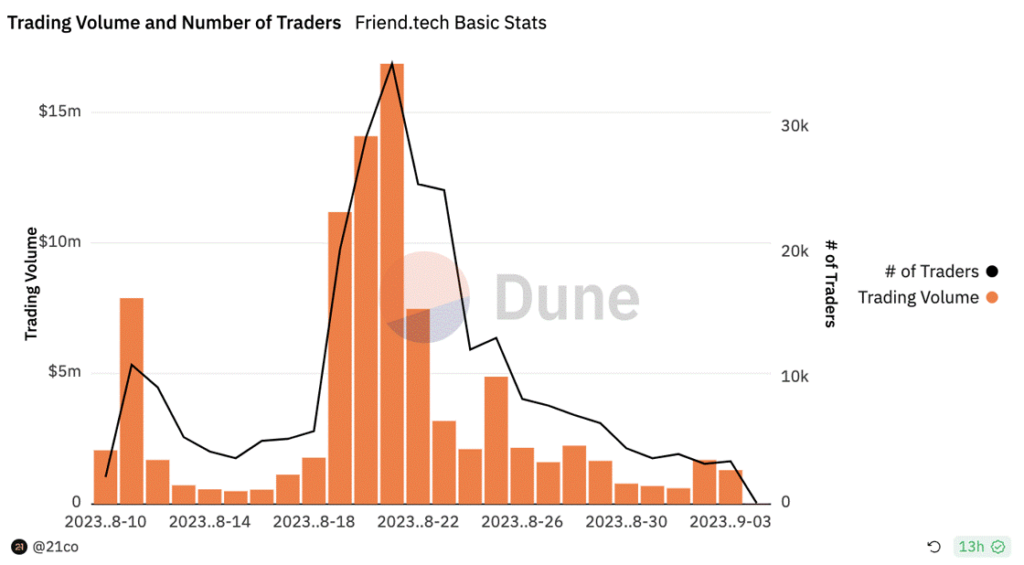

• The Debut of Friend.tech and the broader Social-Fi movement

Friend.tech, a novel social app launched on Base network, letting users tokenize and trade Twitter account shares. Share prices scale with availability; more shares mean higher prices with a 10% tax split—5% for the protocol and 5% for the Influencer, while shareholders access private chats, exclusive content and deepen social ties with their influencers.

Despite early glitches, Friend.tech’s arrival is noteworthy. It employs Base’s Account Abstraction tech for a smooth on-chain user experience, letting users join with web2 credentials, deposit without a wallet setup, and trade shares fee-free. A web app model also evades Apple/Google limits, facilitating mobile deployment. Finally, Friend.tech integrates finance into social networking, reshaping the relationship to offer both financial and social gains and reflecting what is known as Social Finance (SocialFi).

Impressively, Friend.tech surpasses rivals like Lens protocol, achieving significant visibility in the social vertical. In 10 days, it traded ~$60M worth of shares, with up to $3M in daily fees, exceeding smart-contract platforms in peak hype. Remarkably, at the depth of the bear market, the application drew nearly 127K users, although some were possibly driven by the prospect of an airdrop while being amongst the rare crypto apps capturing the attention of external figures. High-profile personalities like NBA player Grayson Allen, CEO of Y Combinator Garry Tan, and even gaming influencers like FaZe Banks all joined the platform.

Figure 7: Total Trading Volume & # of Traders on Friend.tech

Source: @21co on Dune

In summary, Friend.tech could bring untapped web2 innovations into SocialFi, aligning with web3’s empowerment goals by converging social relationships with financial opportunities. However, pricing and wallet privacy need to be enhanced for trust. Vulnerabilities like linking wallets to Twitter emphasize the exigency for robust privacy safeguards within SocialFi applications to protect the technology’s integrity. Regulatory risks could also arise driven by expectations of user profits and revenue sharing. That said, Friend.tech’s is still worth monitoring as a blueprint for future crypto apps in terms of abstracting crypto’s complexity.

Bookmarks

• Exploits, Liquidations, and What Lies Beneath the Surface.

• Our researcher Tom Wan shared his insights in Blockworks’ webinar: Next-Level Web3 Data Strategies to Ride the Latest Trends.

• We published a dashboard tracking the post-mortem of the Curve exploit; check it out here.

• Have you heard of re-staking your staked ETH? EigenLayer is a new staking primitive that enables the reusing of staked ETH. We built a dashboard to track its progress and adoption. Check it out here.

Next Month’s Calendar

These are the top events we’re closely monitoring in September.

• September 20-22: Messari Annual Event

• September 30: Optimism Token Unlock (3.37%)

Source: 21shares, Forex Factory, CoinMarketCap

Research Newsletter

Each week the 21Shares Research team will publish our data-driven insights into the crypto asset world through this newsletter. Please direct any comments, questions, and words of feedback to research@21shares.com

Disclaimer

The information provided does not constitute a prospectus or other offering material and does not contain or constitute an offer to sell or a solicitation of any offer to buy securities in any jurisdiction. Some of the information published herein may contain forward-looking statements. Readers are cautioned that any such forward-looking statements are not guarantees of future performance and involve risks and uncertainties and that actual results may differ materially from those in the forward-looking statements as a result of various factors. The information contained herein may not be considered as economic, legal, tax or other advice and users are cautioned to base investment decisions or other decisions solely on the content hereof.

JGPD ETF är en aktivt förvaltad ETF som delar ut månadsvis

JP Morgan noterar tre nya ETFer på Xetra en av dem i SEK

OSYU ETF ger exponering mot Secured Overnight Financing Rate

iShares Space Technologies UCITS ETF investera bortom jorden

JIPD ETF delar ut månadsvis

USA satsar 2 miljarder dollar på kvantdatorer – så kan investerare dra nytta av utvecklingen

De bästa ETFerna för att investera i emerging markets

Extrema skillnader: Varför presterar Europas kvantdator-ETFer så olika?

Fastställd utdelning i MONTDIV maj 2026

Varför Plus500 är en dröm för finans-affiliate

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanUSA satsar 2 miljarder dollar på kvantdatorer – så kan investerare dra nytta av utvecklingen

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanDe bästa ETFerna för att investera i emerging markets

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanExtrema skillnader: Varför presterar Europas kvantdator-ETFer så olika?

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanFastställd utdelning i MONTDIV maj 2026

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanVarför Plus500 är en dröm för finans-affiliate

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanASWF ETF är en aktivt förvaltad fond som investerar i Kanada

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanQQCC ETF följer företag världen över som är aktiva inom kvantberäkning

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanETFer för fotbolls-VM 2026