Nyheter

Commodity ETPS see fifth consecutive week of inflows

Commodity ETPS see fifth consecutive week of inflows

Highlights

- ETFS Physical Silver (PHAG) sees $38mn of inflows, the second highest in five months.

- Long copper ETPs see US$19mn of inflows, the highest in 10 weeks as an 8.9% price drop was viewed as buying opportunity.

- ETFS Aluminium (ALUM) sees largest inflows since August 2013.

- ETFS Daily Leveraged Natural Gas (LNGA) saw US$6.2mn of inflows as a 6.0% fall in price attracted buyers.

- Profit-taking drives US$15.2mn out of long platinum ETPs.

- Commodity ETPs saw a fifth consecutive week of inflows, with investors taking advantage of price dips in industrial metals to build long positions.

With the situation in the Ukraine showing few signs of stabilising and economic data from China coming in softer – than – expected, gold and silver prices rose as both metals lived up to their reputation as portfolio diversifiers and insurance assets. Investors tilted their portfolios in favour of silver, likely because of expected leveraged moves relative to the gold price.

ETFS Physical Silver (PHAG) sees $38mn of inflows, the second highest in five months. The strong inflows last week follow on the US $132 mn three weeks ago. Investors are increasingly allocating to silver as it has traditionally outperformed gold when both are rising. So far this year gold has returned 13.6% while silver has returned 8.9%, highlighting the potential for silver to catch up.

Long gold ETPs saw US$67 mn of outflows as some investors chose to take profits on recent price gains. Long copper ETPs see US$19 mn of inflows, the highest in 10 weeks as an 8.9% price drop was viewed as buying opportunity. The main trigger for the price slump was a corporate bond default that raised concerns about a possible unwinding of copper collateralised financing deals that some feared would release copper stockpiles into the market. Weaker than expected China export and growth numbers and a fall in the Chinese Renminbi added to the negative sentiment. Investors appear to looking beyond the near – term turbulence, which has been driven by the government’s efforts to introduce healthy two -way risk into the market. China’s copper demand in fact remains robust. Imports for January and February are up over 40% on a year earlier, with January imports reaching record levels. Demand generally picks up after the end of Q1, and we expect a similar pattern will be followed this year. Although a number of investors expect prices to continue to fall (there were US$5.7mn of inflows into ETFS Daily Short Copper (SCOP) last week as well) more investors appear to see price upside.

ETFS Aluminium (ALUM) sees largest inflows since August 2013. As the Aluminium price fell 3% last week, flows into ETFS aluminium ETPs rose US$9 mn. Investors appear to be looking beyond the lower – than -expected export and production data in China and are focusing on the ore export ban in Indonesia which could crimp China’s production of aluminium given that its smelting facilities are dependent on the low temperature (trihydrate) bauxite which is difficult to get from other sources. Possible Russia export sanctions are also playing a role as Russia is the world’s second largest supplier of the met al.

ETFS Daily Leveraged Natural Gas (LNGA) saw US$6.2mn of inflows as a 6.0% fall in price attracted buyers. However, we continue to believe that demand for gas in spring will be lower and ease the pressure on supplies leading to further price declines.

Profit taking drives US$15.2mn out of long platinum ETPs. The outflows were the largest since September 2013 despite the South Africa mine strike entering its eighth week.

So far the three main producers have lost 499,000 ounces of production according to Bloomberg calculations and the figure is closely approaching the 496,359 ounces of lost output from the 2012. While the rally took a pause last week, it has the potential to continue further as stocks deplete.

Key events to watch this week.

Next week’s FOMC meeting will be the first chaired by Yellen and the market will be attentive to any change in policy signals. Should EU car registration data continue to rise as it has in the past five months, we could have catalyst to platinum group prices which have simply treaded water last week.

Note: All flow and AUM data in this report are based on ETF Securities ETPs to 13 March 2014 and are denominated in USD unless otherwise indicated.

Important Information

This communication has been provided by ETF Securities (UK) Limited (”ETFS UK”) which is authorised and regulated by the United Kingdom Financial Conduct Authority.

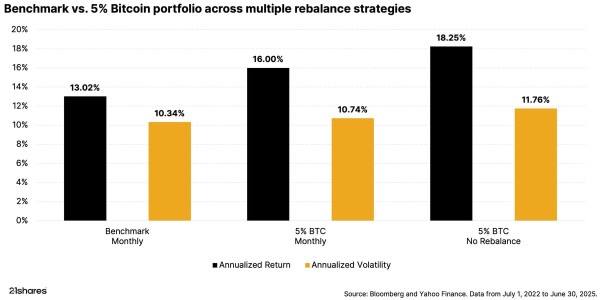

Many investors wonder: If I add Bitcoin to my portfolio, what difference will it make? To answer these questions, we analyzed data to see how even a small Bitcoin allocation can impact your overall investment returns and risk.

It’s Crypto Week. Keep an eye on these bills

This week, the US House of Representatives will host “Crypto Week,” a focused effort to create clearer rules for digital assets. If these new laws pass, they could help investors feel more confident about entering the crypto market. The historic Crypto Week will likely benefit crypto lending projects like Aave, which has recently exceeded $45 billion in total value locked. Take a closer look at what’s on Congress’s agenda and why it matters for the future of crypto.

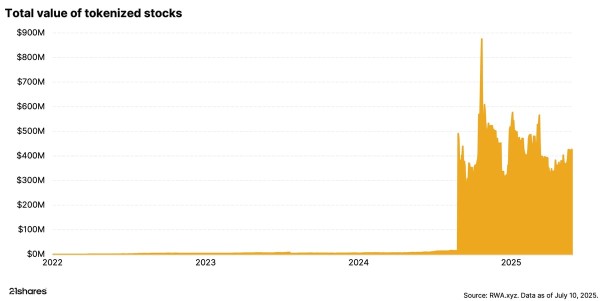

Turning stocks into tokens? Why it’s cool, but complicated

Crypto keeps evolving, and one clear use case is tokenization, turning real-world assets like property, investment funds, or stocks into digital tokens on the blockchain. Tokenized stocks are grabbing headlines right now as they let you trade company shares anytime, anywhere, making investing easier and faster. But it’s still early days, and there are challenges ahead. Explore how stock tokenization works and what’s holding it back.

Research Newsletter

Each week the 21Shares Research team will publish our data-driven insights into the crypto asset world through this newsletter. Please direct any comments, questions, and words of feedback to research@21shares.com

Disclaimer

The information provided does not constitute a prospectus or other offering material and does not contain or constitute an offer to sell or a solicitation of any offer to buy securities in any jurisdiction. Some of the information published herein may contain forward-looking statements. Readers are cautioned that any such forward-looking statements are not guarantees of future performance and involve risks and uncertainties and that actual results may differ materially from those in the forward-looking statements as a result of various factors. The information contained herein may not be considered as economic, legal, tax or other advice and users are cautioned to base investment decisions or other decisions solely on the content hereof.

A slice of Bitcoin gives a big portfolio boost

LYOR ETF är en aktiv satsning på ”over night lån”

WisdomTree noterar hävstångsprodukter på Xetra

VALOUR TRX SEK spårar priset på kryptovalutan Tron

Börshandlade fonder för globala utdelningsaktier

De bästa ETFer som investerar i europeiska utdelningsaktier

Nordea Asset Management lanserar nya ETFer på Xetra

Svenska investerare — 21Shares Nasdaq Stockholm-sortiment har just blivit starkare

De bästa ETFerna med fokus på momentum

Hetaste investeringstemat i juni 2025

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanDe bästa ETFer som investerar i europeiska utdelningsaktier

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanNordea Asset Management lanserar nya ETFer på Xetra

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanSvenska investerare — 21Shares Nasdaq Stockholm-sortiment har just blivit starkare

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanDe bästa ETFerna med fokus på momentum

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanHetaste investeringstemat i juni 2025

-

Nyheter2 veckor sedan

Nyheter2 veckor sedan12 000 artiklar om börshandlade fonder

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanPrimer: Injective, infrastructure for global finance

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanREX Shares lanserar tre nya covered call ETFer i Europa