Nyheter

ECB rule bending to pressure the Euro

ETF Securities – ECB rule bending to pressure the Euro

Highlights

- Markets have repriced the Euro lower, as the chance for a populist Presidential win from Le Pen’s Front Nationale (FN) has increased in recent weeks.

- The Euro, beset by political uncertainty, has been unable to benefit from the uptick in the underlying economic environment and an improvement in investor positioning in the futures market.

- Although European Central Bank (ECB) quantitative easing (QE) program appears at its limit, the central bank appears ready to deviate from its ‘capital key’ and buy bonds from more heavily indebted nations, in turn putting further pressure on the Euro later in 2017.

Politics repricing the Euro

Analysts have repriced consensus forecasts lower for the EUR/USD during 2017, as political uncertainty threatens to break-up the Eurozone. At the end of 2016, consensus forecasts centred around 1.07 by end Q1 2017, compared to just 1.04 currently. We expect that the Euro should end Q1 around 1.08 as political uncertainty fades.

(click to enlarge)

The Euro has been battered by political uncertainty and has been unable to benefit from the improvement in the underlying economic environment. The Bloomberg Eurozone Economic Surprise Index suggests that the Euro could, in the absence of the ECB’s QE activities and the current uncertainty surrounding the political environment, be significantly higher against the USD.

Although populism and an increasingly insular voter attitude is a distinct similarity between the US and the Eurozone, the result for the currency could be a stark contrast. After vowing to bring back the French Franc, the potential for FN’s Le Pen to win the French election could prompt the Euro to move to parity against the US Dollar, a contrasting result compared to the US Dollar strength after the Trump Presidential victory. Nonetheless, EUR/USD parity on the back of a Le Pen victory is not our base case.

Economics drives policy differences

There are also other differences on an economic level between the US and Europe: unemployment across the Eurozone remains elevated, and excess spare capacity is likely to keep wage growth muted for some time. With excess labour market capacity, there is unlikely to be the pressure on core inflation that we expect to occur in the US later in 2017.

(click to enlarge)

However, inflation expectations have been rising on a global basis. The unwind of oil price effects has pushed headline prices higher, even beyond our bullish view and well beyond consensus expectations for the Eurozone. Eurozone inflation reached the highest level since March 2013, and now is in line with the ‘close to or below’ the 2.0% ECB target. Importantly inflation is unlikely to spike above the central bank’s target in coming months, and the ECB will ‘look through recent upturns in headline inflation’.

ECB nearing its limit

While the US Federal Reserve is taking a hawkish approach, the ECB is firmly in accommodative support mode with monetary policy.

(click to enlarge)

The ECB’s balance sheet has never been larger. However, the ECB is nearing the limit of its QE activities, with growth in its balance sheet fading. However, there are signs that the central bank could move outside the current scope of the asset purchase scheme to once again boost its balance sheet and the Eurozone money supply.

(click to enlarge)

Although the Euro should benefit if the ECB was able to cease its bond buying without any significant dislocations in interest rate markets by year-end, the potential for fresh policy pressure has weighed on the common currency.

The ECB’s latest Account of the monetary policy meeting noted the potential for the central bank to make ‘limited and temporary deviations’ from its capital key. This suggests the possibility of moving away from a broad GDP based bond buying scheme towards a debt weighted scheme. Such a move would advantage more heavily indebted nations such as Italy, but pressure the Euro in H2 2017.

What are markets pricing?

Futures market positioning has rebounded from extremely depressed levels, but investors remain net short of the Euro. However, the Euro is more depressed than what the historical relationship indicates. In contrast, options market pricing is highlighting the Euro is expected to be the second worst performer against the USD in the G10. Options pricing is the most pessimistic about the Euro’s valuation since June 2016.

(click to enlarge)

We expect the Euro to strengthen to around 1.08 in coming months as it becomes more apparent that Le Pen’s FN party is unlikely to win the French Presidency. Despite this volatility will remain, and further ECB asset purchases and ‘rule bending’ could see the Euro move back toward current levels in H2 2017.

Important Information

The analyses in the above tables are purely for information purposes. They do not reflect the performance of any ETF Securities’ products . The futures and roll returns are not necessarily investable.

General

This communication has been provided by ETF Securities (UK) Limited (“ETFS UK”) which is authorised and regulated by the United Kingdom Financial Conduct Authority (the “FCA”).

This communication is only targeted at qualified or professional investors

Nyheter

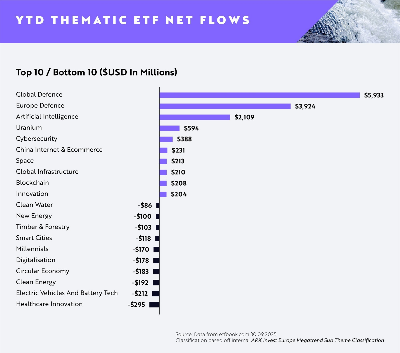

AI minskar gapet mot försvaret då flödena av europeiska tematiska ETFer når 13,1 miljarder dollar hittills i år

Flödena av europeiska tematiska UCITS-ETFer fortsätter att öka uppåt i takt med att investerare dras mot högt övertygande megatrender, med AI (Artificiell Intelligens), försvar, energi (specifikt uran) och Kinas internet och e-handel alla i ledande positioner.

Viktiga punkter

- AI minskar gapet på försvaret då flödena av europeiska tematiska ETFer når 13,1 miljarder dollar hittills i år

- Försvaret fortsätter att dominera under första till tredje kvartalet (+9,86 miljarder dollar)

- AI toppar nettoinflödena för augusti och september

Globala försvars-ETFer fortsätter att leda flödena hittills i år (YTD) med +5,93 miljarder dollar i nettoflöden, med europeiska försvars-ETFer på andra plats med +3,92 miljarder dollar i nettoflöden.

Emellertid har ETFer inom artificiell intelligens sett en anmärkningsvärd ökning i efterfrågan sedan slutet av första halvåret 2025, med dominerande inflöden under augusti och september för att nå nästan +2,11 miljarder dollar i nettoflöden hittills i dag. Detta motsvarar en ökning med cirka 133 % i nettoflöden sedan slutet av första halvåret jämfört med Global Defence på +23 % och European Defence på 29 %.

Investerarnas aptit för försvar är fortsatt stark då geopolitiska risker och moderna krigföringskrav driver strukturella medvindar för sektorn. Försvarsentreprenörer i framkant inom avancerad flyg- och rymdteknik, cybersäkerhet och drönarteknik tar en växande andel av de globala upphandlingsbudgetarna.

I Europa är allokeringarna fortfarande höga då regeringar över hela kontinenten reagerar på nya säkerhetsrealiteter med ökade utgiftsåtaganden. Investerare verkar fokuserade på lokala ledare med exponering mot underrättelsesystem, försvarselektronik och strategisk tillverkning.

Den ökade efterfrågan på ETFer inom artificiell intelligens visar att innovationstakten inom generativa modeller och företags-AI fortfarande är en viktig magnet för kapital. Investerare föredrar plattformar med skalbar AI-infrastruktur och exponering mot verkliga applikationer inom programvara, halvledare och robotteknik.

På andra håll rankades uran-ETFer på fjärde plats med +594 miljoner dollar i nettoflöden, medan cybersäkerhets-ETFer rankades på femte plats med +388 miljoner dollar. Båda teman fortsätter att attrahera kapital tack vare tydliga men hållbara drivkrafter: uran från den förnyade satsningen mot kärnkraft i övergången till ren energi och cybersäkerhet från eskalerande digitala hot och växande efterfrågan på motståndskraftig infrastruktur.

Rahul Bhushan, VD och global chef för investeringsprodukter på ARK Invest, kommenterade flödena: ”Investerare ompositionerar sig aktivt mot innovationsdrivna, strukturellt drivna teman i en föränderlig makromiljö. Med geopolitiska risker, genombrott inom generativa modeller och AI-ledd innovation uttrycker investerare starka åsikter om megatrender snarare än breda, odifferentierade exponeringar. Det är tydligt att tematiska ETFer inte längre bara är taktiska satsningar, de är centrala strategiska exponeringar.”

HANetfs Hector McNeil förklarar hur ETFer genererar hög avkastning med covered calls

JPEY ETF högavkastande företagsobligationer vautasäkrade till Euro

AI minskar gapet mot försvaret då flödena av europeiska tematiska ETFer når 13,1 miljarder dollar hittills i år

XMME ETF – Levler MSCI EM by Xtrackers

34GI ETF bara eurodenominerade företagsobligationer med förfall 2024

De bästa lågvolatilitets ETFer på marknaden

Fokus mot en helt ny börshandlad produkt i september 2025

M5TYs senaste utdelningstakt (55 %) belyser covered call-strategins inkomstpotential

Could Bitcoin be the key to your dream house?

Börshandlade fonder för europeiska small caps

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanDe bästa lågvolatilitets ETFer på marknaden

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanFokus mot en helt ny börshandlad produkt i september 2025

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanM5TYs senaste utdelningstakt (55 %) belyser covered call-strategins inkomstpotential

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanCould Bitcoin be the key to your dream house?

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanBörshandlade fonder för europeiska small caps

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanLevler noterar ytterligare fyra börshandlade fonder i Sverige

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanThe Investment Case for TLT (Long-Dated Treasury Bonds)

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanMiners Find Their Mojo as Gold Consolidates