Nyheter

Can These Adoption-Centric Developments Summon the Bull?

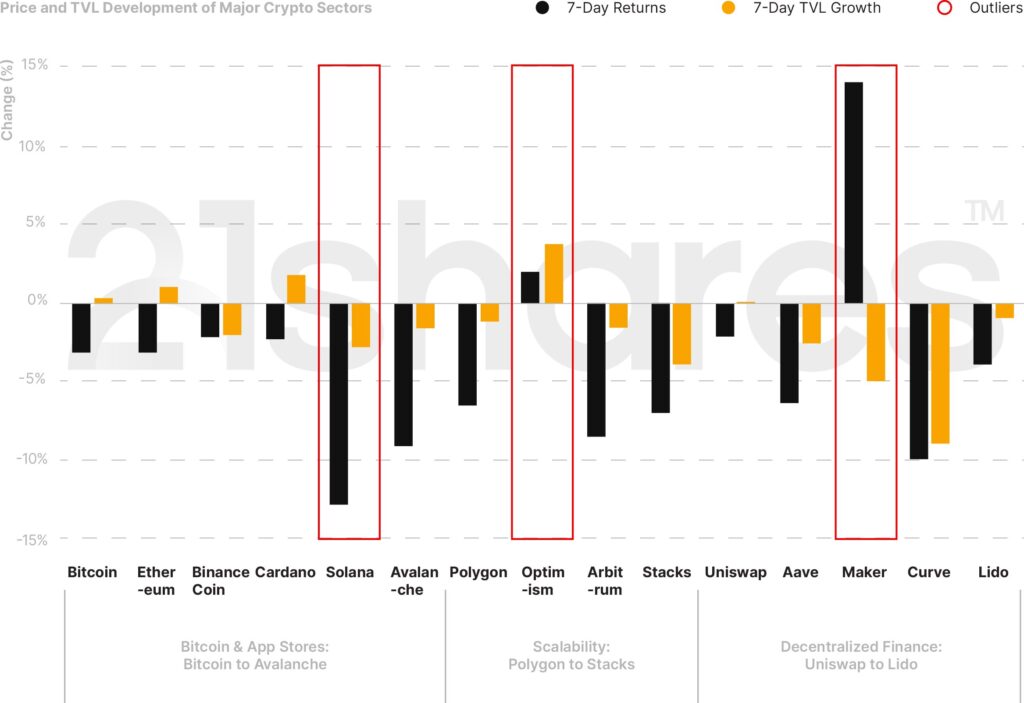

Markets fell over the past week following Nasdaq’s earnings call, where they announced they’re no longer pursuing crypto custody, citing regulatory uncertainty. As recession fears loom in the U.S., Bitcoin and Ethereum fell by around 3% each. The biggest winner was Maker DAO which increased by 14% over the past week, while Solana suffered the most with an almost 13% decrease. Maker’s surge can be attributed to their buyback scheme, which is meant to reduce the surplus of MKR to enhance the token’s scarcity and value proposition. The Smart Burn Engine periodically allocates excess DAI stablecoins from Maker’s surplus buffer to purchase MKR from a Uniswap pool. At the sixth edition of the Ethereum Community Conference (EthCC) last week, Solana introduced Solang, a new compiler designed to smooth the transition for Ethereum Virtual Machine (EVM) developers into the Solana ecosystem. More developments were unveiled at the EthCC; read on as we break them down later in this report.

Figure 1: Weekly Price and TVL Developments of Cryptoassets in Major Sectors

Source: 21Shares, CoinGecko, DeFi Llama. Close data as of July 17, 2023.

5 Things to Remember in Markets this Week:

• Societe Generale Becomes Authorized to Bridge Institutions to Crypto

On the same day Nasdaq announced the halting of its crypto custody application due to regulatory uncertainty in the U.S., Societe Generale became the first company to receive a digital asset service provider (DASP) license in France. This instance speaks volumes of the dire need for legal clarity to streamline the adoption of this asset class, especially for institutions. The license allows Forge, the bank’s cryptoasset division, to operate digital asset custody, sell and purchase digital assets for legal tender, and trade digital assets. In April, Forge launched CoinVertible (EURCV), an institutional stablecoin on the Ethereum blockchain, with the euro as the denominator. Societe Generale hits two birds with one stone: addressing regulatory concerns over the hegemony of the euro with the rise of dollar-pegged stablecoins, as well as meeting the institutional need for an innovative settlement and cash management solution.

• Gnosis Launches Self-Custodial ATM Card at Ethereum Community Conference

Gnosis is a blockchain infrastructure provider known for its Ethereum Virtual Machine (EVM) execution-layer chain that utilizes Maker DAO’s DAI stablecoin to enable transactions and cover fees. Gnosis launched two products at the EthCC in Paris last week: Gnosis Card in partnership with Visa and Gnosis Pay to provide the community with a payment solution that would allow users to spend cryptoassets held in their custody, with KYC verification in partnership with Fractal. Gnosis Pay also allows crypto wallets to use their APIs and toolset to issue their debit cards. This payment solution was made possible thanks to an earlier partnership with Monerium, granting Gnosis access to the SEPA payment system. So far, people in Europe and the UK can open an account on Monerium, set up their Gnosis Card, trade Monerium’s euro-pegged stablecoin, and soon DAI. There are plans to expand to Mexico, Brazil, and Hong Kong. The U.S. is also on the roadmap for Q3. With a mobile app in the works, this self-custodial payment solution promises to solve key pain points ailing the crypto wallet subsector, mainly regarding regulations and user interface that stand in the way of mass adoption.

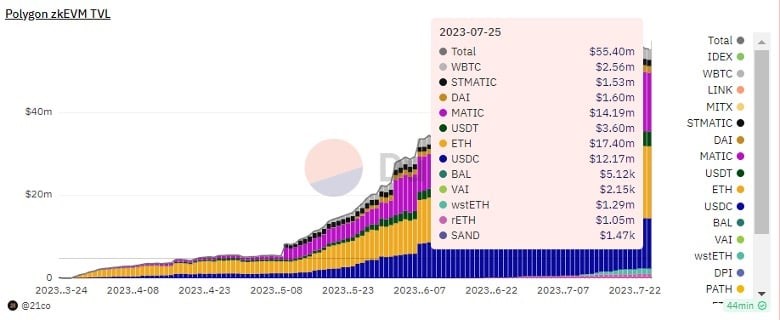

• Polygon unveils the last puzzle piece of its 2.0 network, focused on governance. Namely, the overall system will be compartmentalized into three distinctive branches: Protocol, Smart Contracts System, and Community Treasury Governance. The protocol level will expand the existing governance framework to all the networks that will plug into the Polygon network. On the Smart contracts level, Polygon proposes a community-governed ecosystem council to improve decision-making. Finally, the community treasury will aim to fund promising initiatives that help drive the evolution of the ecosystem, giving users a say in determining the trajectory of growth for the network. The decision to define the three governable pillars is designed to help establish clear responsibilities for the key decision-makers and an effective framework to administer the growing network. The announcement, culminating Polygon’s 6-week program to unveil its new network design, saw a steady growth in total number of users and an increase of close to 100% in AuM on the new scaling solution, climbing from ~$23M to ~$55M, as shown below.

Figure 2: Polygon zkEVM Scaling Solution AuM

Source: 21co on Dune Analytics

• Google Feeling Warmer Towards Crypto

After long refusing to support advertisements on its search engine or on its play store application, Google is finally embracing the web3 ecosystem. The change of heart was laid out in their latest July 2023 policy updates, where the company modified set guidelines for developers looking to integrate blockchain-native content into their applications. Namely, they must maintain transparency and avoid glamorizing potential earnings revenue ensuing from crypto-based activities. That said, this is a turning point in the history of web3 as abstracting the complexity of the technology via integrating with existing systems should help accelerate the adoption of crypto, especially as it merges into the backend with existing backend infrastructure and becomes invisible for the user. It’s also a key step in promoting unique user-owned content and helping consumers retain the value of their data and time.

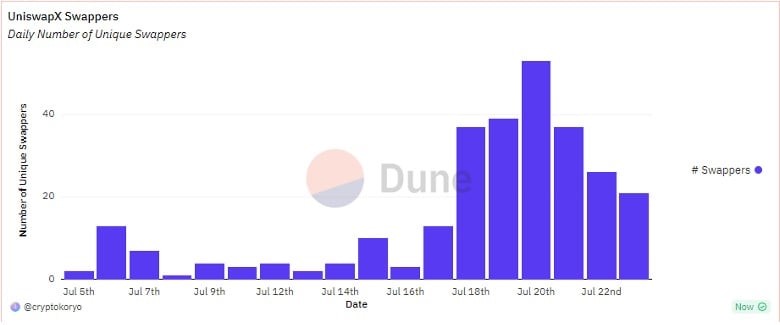

• UniswapX; an Upgrade Looking to Tackle Users’ Frustrations

Uniswap Labs announced the X upgrade during EthCC last week, a protocol enhancement merging on-chain and off-chain liquidity aggregation, internalizing Maximum Extractable Value (MEV) through price improvement, offering gas-free swaps, and opening the doors for supporting cross-chain trading. While some of the newly advanced features have long been incorporated into smaller exchanges, the upgrade nevertheless holds significant value for blistering the adoption of non-custodial infrastructure. Namely, abstracting away the toxic practice of MEV to safeguard users’ transactions has been a chronic problem hindering the adoption of decentralized exchanges. Thus, considering Uniswap’s position as the market leader, offering a refined experience that matches the intuitiveness of centralized platforms and prioritizes users’ needs is a key driver to help onboard new entrants and make them feel comfortable using blockchain-native applications.

Figure 3: Daily Number of Unique UniswapX Users

Source: @cryptokoryo on Dune

What You Should Pay Attention To

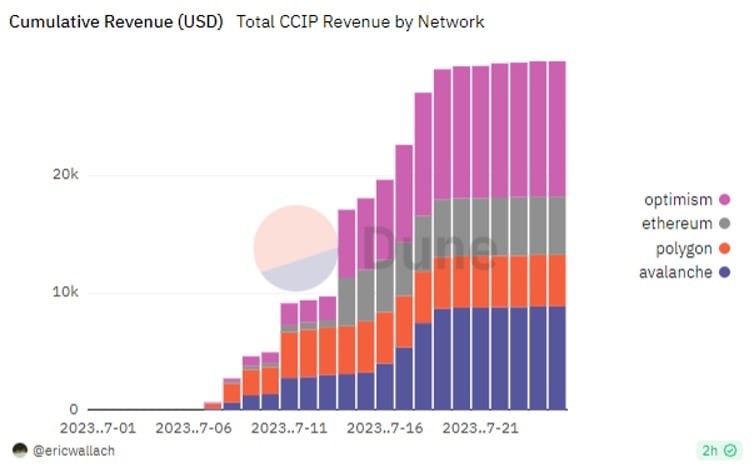

• Chainlink’s highly anticipated interoperability product finally launched on Mainnet. Announced at EthCC, Chainlink’s Cross Chain Interoperability Protocol (CCIP) is an inter-blockchain communication standard that helps with transferring data and value across a web of incompatible networks, with initial support for transfers between Ethereum, Polygon, Optimism, Avalanche, and Arbitrum at the start. Check out our State of Crypto Issue 8 for a deeper dive into the technology.

That said, four features will be incorporated into CCIP to address the shortcomings of the existing bridging solutions. The first feature is an Active Risk Management (ARM) Network that can detect malicious activity and automatically pause the transfer of data per achieving a certain threshold. The second is programmatic transfers, transactions with a set of preconfigured instructions that execute automatically once a condition is satisfied. Three, rate limits, a mechanism to prevent transfers from surpassing a predefined maximum amount of tokens to address unauthorized access, and finally, smart execution, enabling the execution of cross-chain activities without incurring multiple payments using a pre-funded escrowed account.

Chainlink’s product is a major step forward for the growth of the ecosystem as it tackles fundamental weaknesses crippling crypto’s infrastructure. Cross-chain bridges with weak security designs have been a prime target for hackers, which have, over the past two years, led to the exploitation and siphoning of Close to $2.5B worth of value. Thus, it’s a pivotal milestone to have an internet of contracts, similar to how the TCP/IP unified the global internet, facilitating liquidity to be globally accessible and the value of applications to flow across networks to be established on battle-tested infrastructure that enabled more than $8T in transactional value.

Further, due to the wide applicability of interoperability across the crypto landscape, CCIP will likely be Chainlink’s biggest and most consequential product. For context, applications using Chainlink’s CCIP can pay in either LINK or a set of ERC20 tokens to transact cross-chain, with a 10% premium set on the latter to incentivize LINK usage. This distinction positions the network’s native token as a universal gas currency across all chains. It eliminates the operational necessity of selling the token for node operators and incites the foundation to switch off its subsidization program.

With a fee-based revenue model in place, the protocol can now grow sustainable earnings for the nodes participating in Chainlink’s Decentralized Oracle of Networks (DONs), which are the security backbone of all of Chainlink’s services. That said, although Chainlink accrued only $30K in fees over the first few days due to the limited partners at launch, with only Synthetic and Aave employing CCIP for transferring tokens and cross-chain governance, we could see substantial growth as Chainlink expands its partner network. The integration with SWIFT further solidifies CCIP’s potential as the go-to solution for cross-chain interoperability for crypto and traditional players, eventually allowing connectivity between both financial systems.

Figure 4: Total Revenue Accrued by CCIP

Source: @Ericwallach on Dune

• Solana Attempting to Claw Back

Solana experienced a rough start to the year stemming from the collapse of FTX, then recently, due to its involvement in the SEC’s legal actions against Coinbase and Binance. However, the network has welcomed a series of developments that could help catalyze its recovery. First, Solana Labs has unveiled Solang at EthCC, a new compiler designed to allow Ethereum developers to deploy their applications using the native ETH-based programming language, Solidity, on the Solana operating system, bridging the gap between both ecosystems. In addition, Neon EVM went live on Solana’s mainnet, introducing the first Ethereum-compatible smart contract allowing developers to seamlessly migrate their ETH apps onto Solana without incurring significant modifications for the codebase. Finally, Solana Labs revealed GameShift, a unifying web3 game development API that aggregates all the necessary tools to streamline the developmental process for building games on the network.

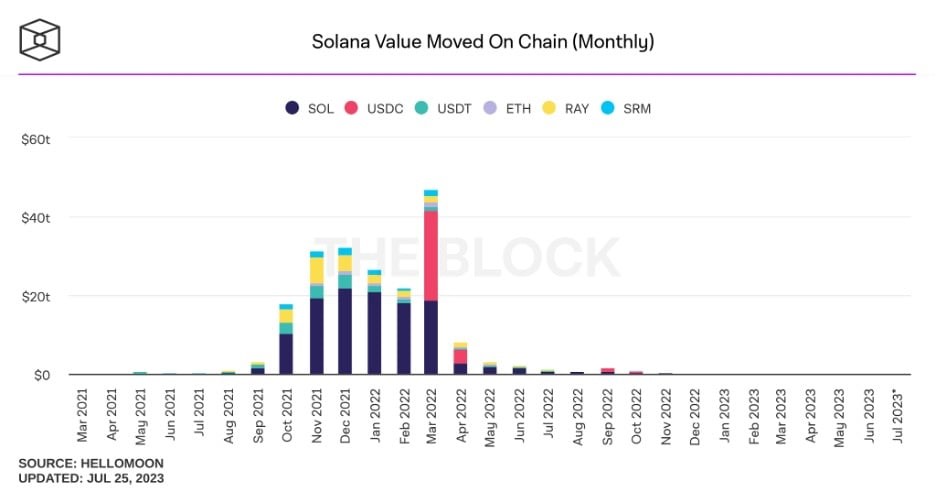

Overall, Solana’s activity is showing signs of hopeful recovery, with the total number of active addresses rebounding from the June lows to grow by 25% over the past ~7 weeks, while the total AuM locked into the network reached its highest level over the past year. That said, there are plenty of catalysts that could trigger further excitement about the network, from the Jump Crypto’s Firedancer validator client designed to diversify node software and combat network outages to the flurry of highly demanding applications like Hiver, Teleport and Helium that wouldn’t be feasible on networks with less throughput. Nonetheless, there’s still a lot of work to do to encourage users to move their capital back to Solana, especially as the total value transferred on the network remains at relatively muted levels.

Figure 5: Monthly Value Moved on Solana

Source: TheBlock

Next Week’s Calendar

These are the top events we’re monitoring for next week.

• Earning week across the board

• FOMC rate decision, Fed Chair Powell news conference, Wednesday

Source: Forex Factory

Research Newsletter

Each week the 21Shares Research team will publish our data-driven insights into the crypto asset world through this newsletter. Please direct any comments, questions, and words of feedback to research@21shares.com

Disclaimer

The information provided does not constitute a prospectus or other offering material and does not contain or constitute an offer to sell or a solicitation of any offer to buy securities in any jurisdiction. Some of the information published herein may contain forward-looking statements. Readers are cautioned that any such forward-looking statements are not guarantees of future performance and involve risks and uncertainties and that actual results may differ materially from those in the forward-looking statements as a result of various factors. The information contained herein may not be considered as economic, legal, tax or other advice and users are cautioned to base investment decisions or other decisions solely on the content hereof.

Vilken typ av sektor ETFer finns det?

LVLD ETF investerar i ett urval av företag världen över med låg volatilitet

Den europeiska ETF-revolutionen: Skiftet som ritar om kartan för kapitalförvaltning

EEAK ETF investerar i eurodenominerade statsobligationer från eurozonen

HEQQ ETF mål är att ge långsiktig kapitaltillväxt

USA satsar 2 miljarder dollar på kvantdatorer – så kan investerare dra nytta av utvecklingen

Extrema skillnader: Varför presterar Europas kvantdator-ETFer så olika?

QQCC ETF följer företag världen över som är aktiva inom kvantberäkning

Fastställd utdelning i MONTDIV maj 2026

Varför Plus500 är en dröm för finans-affiliate

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanUSA satsar 2 miljarder dollar på kvantdatorer – så kan investerare dra nytta av utvecklingen

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanExtrema skillnader: Varför presterar Europas kvantdator-ETFer så olika?

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanQQCC ETF följer företag världen över som är aktiva inom kvantberäkning

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanFastställd utdelning i MONTDIV maj 2026

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanVarför Plus500 är en dröm för finans-affiliate

-

Nyheter1 vecka sedan

Nyheter1 vecka sedanDen osynliga flaskhalsen i AI-boomen: Varför elinfrastruktur är nästa stora megatrend

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanETFer för fotbolls-VM 2026

-

Nyheter4 veckor sedan

Nyheter4 veckor sedan21shares produkter nu finns tillgängliga hos Revolut