Nyheter

Är detta den enda säkra ekonomin som finns kvar?

Är detta den enda säkra ekonomin som finns kvar? Medan de flesta andra ekonomierna låter sina tryckpressar gå in absurdum för att producera ny pappersvaluta som sänker värdet på deras egen valuta finns det ett land som befinner sig i förarsätet och har en stark, stabil ekonomi, en växande exportmarknad och en rad starka och stabila företag.

Det finns en värld av möjligheter där ute, men det finns också allvarliga risker. Den amerikanska aktiemarknaden formligen exploderar när den når nya toppnoteringar, men USAs ekonomi befinner sig fortfarande under isen och det federala budgetunderskottet befinner sig fortfarande på förbluffande höga nivåer.

I Japan försöker regeringen överträffa den amerikanska politiken, och landets budgetunderskott är dubbelt så stort som i USA, precis som den monetära ”stimulansen”.

Storbritannien, precis som resten av EU är inlåst i en recession och det är definitivt bevisat att det inte fungerar med olika typer av åtstramningar heller. Dessa åtstramningar håller nu på att överges i takt med att penningpolitiken blir slappare och slappare och räntorna nu ligger långt under inflationen.

Har BRICs gått på pumpen?

Nej, det är ingen av de så kallade BRICs-länderna Brasilien, Ryssland, Indien eller Kina, som vi hört så mycket om och som alla har så pass höga förhoppningar om.

Ryssland har oljan, men landet har också ett politiskt system som kan beskrivas som kleptokratiskt, en inflation som ligger på 7 procent och stiger.

Kina har, i alla fall tror vi det, fortfarande den tillväxt som behövs, men landet har dessutom ett politiskt system som ingen vill leva under, ett berg av osäkra fordringar vilka gör att landets egentliga budgetunderskott är betydligt större än det som redovisas officiellt.

Indien som spås vara nästa land som kommer att dra världens ekonomi framåt har ett gigantisk budgetunderskott som växer värre än de ogräs varenda villaägare försöker undvika i sommar.

Brasilien är på många sätt det land som är värst av dessa fyra, tillväxten har mattats av och budgetunderskottet är långt högre än vad som redovisas officiellt då en stor del av all finansiering gömts i de statliga bankerna.

Den stora vinnaren är inte ett av de små länderna

Döm då vår glädje då vi ser att det finns ett land som rapporterar ett budgetöverskott, med räntor som överstiger inflationen samtidigt som det finns en minst sagt hygglig tillväxt i ekonomin som genererar ett handelsöverskott.

Det finns ett antal mindre länder med en stark eller i alla fall en anständig tillväxt, men det finns också ett rikt land med en stark aktiemarknad. Landet i fråga befinner sig i ett epicentrum för världens dynamiska tillväxt och landet har en balansräkning som måste betraktas som fantastisk i en tid när vi vant oss vid att global kris.

Landet i fråga är Sydkorea

Är detta den enda säkra ekonomin som finns kvar. Utöver en stark ekonomi så valde landet nyligen en ny borglig president, Park Geun-Hye, som skall vara i tjänst till i första hand 2017. Park Geun-Hye har en stabil majoritet i den sydkoreanska kongressen.

Viktigare av allt är att Sydkorea och landets ekonomi inte drivs framåt av konstgjord stimulans, landet har ett betydande budgetöverskott. Den korta räntan ligger på 2,75 procent, inflationen på låga 1,3 procent samtidigt som landets bytesbalans redovisar ett överskott på 4,5 procent av BNP. Det förväntas växa med 2,9 procent i år och med 3,8 procent under 2014. Dessa tillväxtsiffror låter kanske inte så pass imponerande, men det gör Sydkorea till världens snabbast växande land, i alla fall i den utvecklade världen.

Ger världen vad den vill ha

Sydkorea är en av världens tekniskt ledande nationer, särskilt inom så kallade displaysystem, vad sägs till exempel om bärbara datorer som kan rullas ihop som en tidning? Utöver detta har landet goda kunskaper om stamceller och andra biotekniska innovationer. Vad gäller genteknik kan landets tekniska försprång komma att bli en strategisk fördel då Sydkoreas lagstiftning inte sätter begränsningar för utvecklingen av biotechinnovationer som många länder i västvärlden gör.

Dessutom håller landet på att utvecklas till en kulturell ledare, bland annat efter det att musikfenomenet Gangnam Style sveper över världen som en epidemi. Detta ger visserligen – relativt sett mycket annat – inga stora omedelbara intäkter till Sydkorea, men det gör att landet kan locka till sig många av världens unga, stilmedvetna och rotlösa innovatörer, något som aldrig var möjligt för 20 år sedan.

Landets aktiemarknad värderas till ett genomsnittligt p/e tal på 16, att jämföras med 17 för den amerikanska aktiemarknaden och 13,8 på Stockholmsbörsen. Båda dessa länders ekonomier växer långsammare än den sydkoreanska. Sydkorea har emellertid inte använt sig av tryckpressar för att skapa tillväxt vilket gör att det är osannolikt att vi kommer få se omedelbara problem.

Det stora hotet är emellertid Nordkorea, och det måste betraktas som ett betydande sådant.

Tre sätt att gå lång i Sydkorea

Det finns ett antal olika sätt att köpa in sig i den sydkoreanska aktiemarknaden. Den största Korea-fokuserad ETF noterad i USA är iShares MSCI Sydkorea Index ETF (NYSE: EWY). Med nettotillgångar på $ 3,2 miljarder kronor och ett kostnadsförhållande på endast 0,61% det är ett effektivt sätt att få exponering mot marknaden som helhet. För närvarande har denna ETF ett p/e-tal på endast 10 gånger vinsten, men ett en direktavkastning på endast 0,6%.

Sydkoreanska banker är mycket rimligt värderad i nettotillgångarna, men är för närvarande mycket lönsamma. Den största finanskoncern är Woori Finance Holdings (NYSE: WF), moderbolaget till Woori Bank. Detta företag handlas i dag till 48 procent av det bokförda värdet och till ett p/e ta på 5,7. Baserat på föregående års utdelning har Woori Finance Holdings en direktavkastning på 2,2 procent.

Appe förlorar ständigt marknadsandelar när det gäller mobiltelefoner och surfplattor till Sydkoreanska Samsung. Samsung är litet svårare att handla, men det finns globala depåbevis i London där de handlas under tickerkoden SMSN. I dag värderas Samsung till ett p/e tal på 7,6 på innevarande år och 1,7 gånger det bokförda värdet. Det känns inte dyrt med den tillväxten.

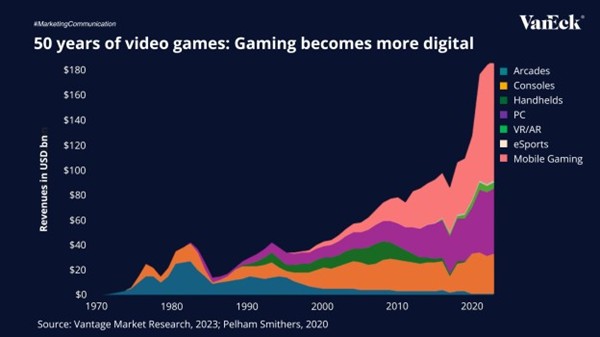

The global gaming industry has evolved into one of the world’s most dynamic entertainment sectors, expected to generate $188.9 billion in 2024 and surpass $200 billion by 2027, outpacing film and music combined.

From arcades to smartphones, the gaming industry has continuously evolved with each technological shift. Today, mobile gaming is a major player the market, currently accounting for the largest share of global revenues. As digital platforms, cloud gaming, and eSports continue to grow, gaming is establishing itself as a core part of the global entertainment economy.

Mobile gaming is leading this transformation, currently accounting for the majority of industry revenues and 40% of all global app downloads. With 5G adoption and 90% smartphone penetration expected by 2030, billions of new players will join the market, making gaming more accessible than ever.

However, the rollout of 5G also carries risks, uneven global infrastructure buildout, high capital costs for carriers, and potential fragmentation across networks could delay or limit the full realization of these benefits.

Source: Vantage Market Research, 2023; Pelham Smithers, 2020

To receive more Gold Investing insights, sign up to our newsletter.

IMPORTANT INFORMATION

This is marketing communication. Please refer to the prospectus of the UCITS and to the KID/KIID before making any final investment decisions. These documents are available in English and the KIDs/KIIDs in local languages and can be obtained free of charge at www.vaneck.com, from VanEck Asset Management B.V. (the “Management Company”) or, where applicable, from the relevant appointed facility agent for your country.

Is Mobile Powering the Future of Gaming?

Fyra nya börshandlade fonder från JP Morgan

AIFS ETF en satsning på infrastruktur för artificiell intelligens

J.P. Morgan Asset Management utökar sitt erbjudande med två nya aktiva ETFer

ISRU ETF köper aktier i stora amerikanska företag

HANetf och Infrastructure Capital Advisors samarbetar för att lansera aktivt förvaltad preferensavkastnings-ETF i Europa

De bästa lågvolatilitets ETFer på marknaden

Time in Bitcoin beats timing Bitcoin

HANetf kommenterar kopparuppgången

Fokus mot en helt ny börshandlad produkt i september 2025

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanHANetf och Infrastructure Capital Advisors samarbetar för att lansera aktivt förvaltad preferensavkastnings-ETF i Europa

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanDe bästa lågvolatilitets ETFer på marknaden

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanTime in Bitcoin beats timing Bitcoin

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanHANetf kommenterar kopparuppgången

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanFokus mot en helt ny börshandlad produkt i september 2025

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanM5TYs senaste utdelningstakt (55 %) belyser covered call-strategins inkomstpotential

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanBörshandlade fonder för europeiska small caps

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanCould Bitcoin be the key to your dream house?

Pingback: Sydkoreansk ETF kan vara ett verktyg för att satsa inför en won intervention - ETF-marknaden