Nyheter

21Shares special report USDC

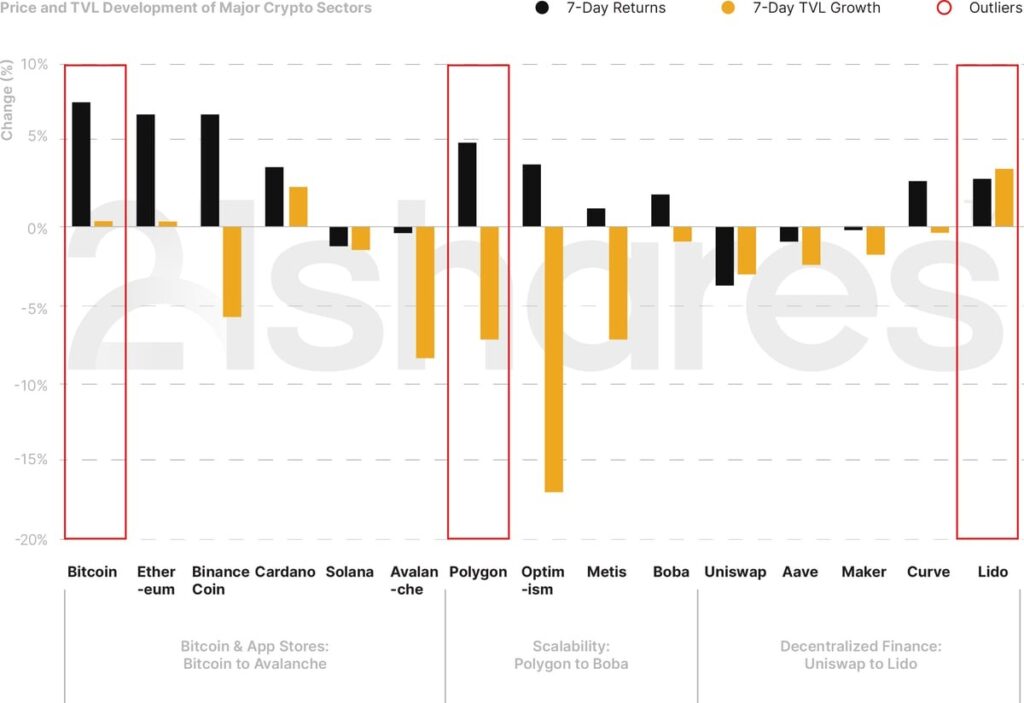

Two bank runs, which led to a short-lived depeg of USDC, shook the crypto market overnight yet increased the total crypto market cap by 5% over the past week. Bitcoin and Ethereum increased by 7.87% and 7.12%, respectively. Factors contributing to the resistance of the two largest cryptoassets by market cap could be attributed to the emerging narrative of Bitcoin as an alternative non-state monetary system alongside its growing ecosystem along with Ethereum’s anticipated Shanghai upgrade scheduled for next month. Coming in second and third in last week’s rally, Polygon (5.31%) within scaling solutions and Lido (3.09%) among decentralized applications.

This special report gives you a timeline of what happened over the past week, explains how it affected the market, and what to expect.

Figure 1: Weekly TVL and Price Performance of Major Crypto Categories

Source: 21Shares, CoinGecko, DeFi Llama. Close data as of March 13.

Key takeaways

• Three banks out of six banks holding USDC reserves collapsed last week, including a voluntary winddown from Silvergate and a takeover of Signature Bank and Silicon Valley Bank (SVB) from US financial regulators amid insolvency fears.

• Circle disclosed that SVB holds 8% of USDC cash reserves USDC depegs over the weekend, reaching an all-time low of 87 cents.

• US regulators stepped in to protect all SVB, Signature Bank depositors, and other potentially-affected banks.

What happened?

March 8

• Silvergate Capital announced on Wednesday that it will wind down operations and liquidate its bank on the back of developments covered in our previous newsletter.

March 10

• The US witnessed its second-largest bank failure. The US Federal Deposit Insurance Corporation (FDIC) took control of SVB after failing to pay depositors.

• Circle disclosed that $3.3B (8%) of reserves backing its USDC remain in SVB, increasing selling pressure.

• Coinbase and Binance paused USDC/USD conversions

March 11

• USDC depegged to $0.87. Circle announced they would stand behind USDC and cover any shortfall using corporate resources, involving external capital if needed.

• USDC was collateralized 77% ($32.4 billion) with short-dated US Treasury Bills via its BlackRock’s money market fund, and 23% ($9.7 billion) with cash held at a variety of US financial institutions, including, Silvergate, Signature Bank, and SVB.

• MakerDAO launched an emergency proposal to limit exposure to USDC

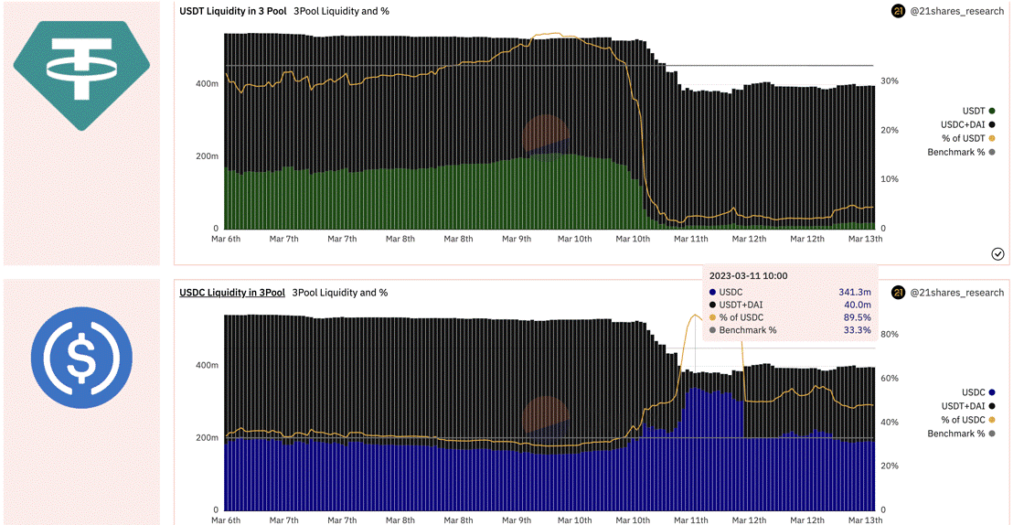

Figure 2: Aggressive Swapping of USDC for USDT on Curve

Source: 21shares on Dune Analytics

• Upon Circle’s disclosure on SVB, exchanges on Ethereum like Curve experienced record-level volumes of $6.7 billion as traders hedged against the USDC debacle for Tether.

March 12:

• US financial regulators took control over Signature Bank

• TheFederal Reserve, Treasury, and the FDIC issued a joint statement:

o SVB and other banks’ depositors will be made whole. SVB depositors would have access to all of their money starting Monday, March 13. The taxpayer will bear no losses associated with the resolution of Silicon Valley Bank.

o Shareholders and certain unsecured debt holders will not be protected.

March 13

• Circle’s CEO Jeremy Allaire confirmed that 100% of USDC reserves are safe and secure and that they will complete their transfer of remaining SVB cash to Bank of New York (BNY) Mellon once banks in the US are back at work after a turbulent weekend.

• USDC repegged to $1.

What to expect?

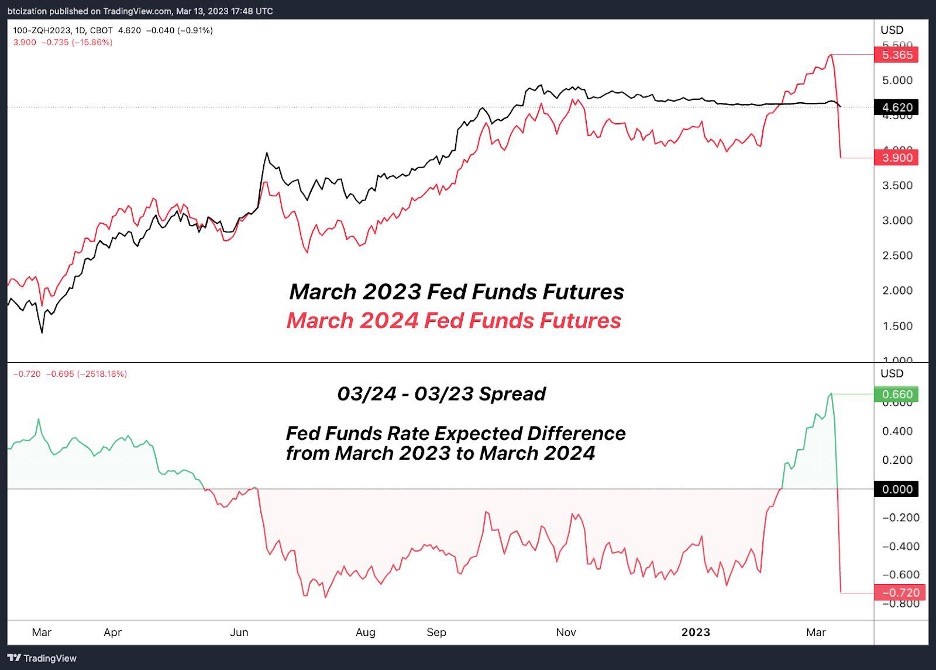

• Easing conditions to bootstrap liquidity: Banks will enjoy a slightly flexible environment allowing them to issue loans for up to one year, using bonds and treasuries as collateral, as part of the Bank Term Funding Program (BTFP).

This initiative is adopted, so the central bank doesn’t terminate its Quantitative Tightening (QT) Program and offset its efforts to dampen inflation. That said, a mild pivot from a high-interest rate to a plateauing rates regime as the liquidity tightening conditions played a role in destabilizing the banking system could come into play, evident by Goldman Sachs’s latest report. FED funds futures are now showing 60% odds of a 0 BPS rate hike in March, in conjunction with a lower estimate for the FED’s funding rate at 5.1%, down from 5.7% from last week.

Figure 3: FED Funds Futures

Source: TradingView

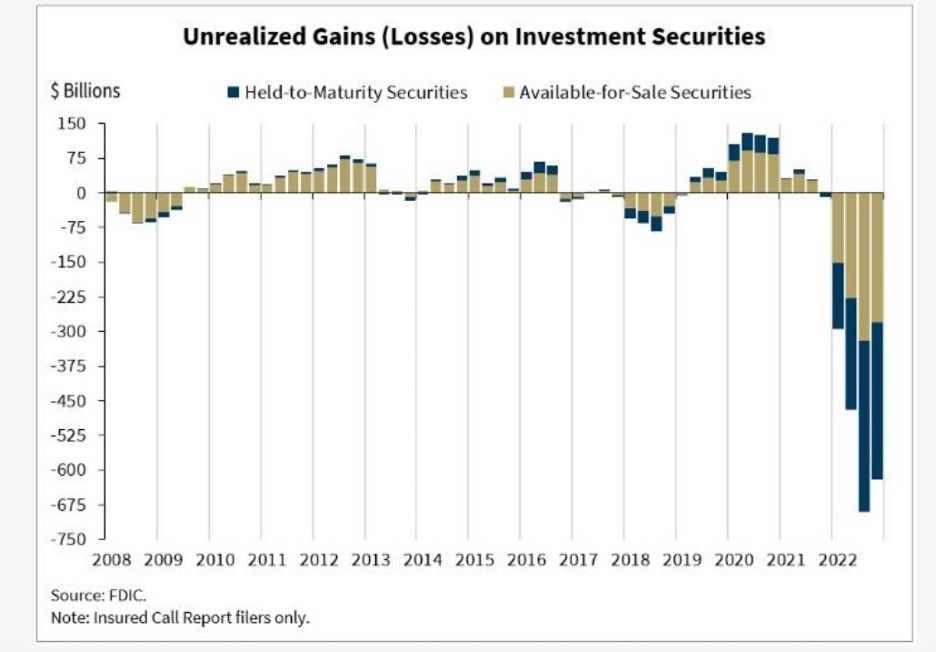

• Counterparty Exposure: More banks catering exclusively to Silicon Valley companies will probably be vulnerable, as last year’s worsening macro conditions have roiled the tech industry. The true extent of the contagion will likely reveal itself over the next few weeks, as the Luna and FTX contagion have demonstrated. This might make it quite challenging for crypto firms to continue operating as Signature and Silvergate provided an instant settlement network for onboarding institutions, let alone providing basic banking services. Last year’s soaring interest triggered the asset-liability maturity mismatch, and thus, more banks are prone to failure if they don’t hedge positions via swaps.

Figure 4: Unrealized Gains/Losses on Investment Securities

Source: FDIC

• Circle weather the storm: The high-interest rate environment benefits stablecoins issuers like Circle as they profit by reinvesting user fiat deposits into US treasuries. This design left them in a strong position where they could liquidate some of the bond portfolios to honor redemptions, which they’ve already begun by liquidating their short-term treasury. Further, their situation is strengthened by the fact that Circle doesn’t share profits on its deposits with token holders. Thus, Circle should be fine as long as there is an elevated circulation of the USDC and the three other banks holding custody of its assets remain solvent.

• Rising support for decentralized stablecoins: Although fiat-backed stablecoins are considered the safest, they are still centralized, as issuers can run into trouble if their hosting banks fail. Moreover, the reliance and intertwinement with the traditional financial system will continue to cast a shadow over how durable these stablecoins can be during systemic shock. Thus, the crypto economy needs a durable stablecoin that can withstand failures in the traditional banking system while at the same time providing assurances of stability that honor users’ redemptions. In that regard, there will be increased calls for new stablecoin designs backed by a mixture of high-quality, uncorrelated, and censorship-resistant assets.

For instance, Maker is discussing revamping DAI’s collateral to reduce its reliance on USDC, while FRAX is proposing to switch its backing from USDC to sfrxETH (new ETH liquid-staking derivative of Frax protocol).

• Certain service providers will pursue becoming a bank or a secure FMA: Much like WeChat and Alipay have accounts at the Chinese central bank (PBOC), Circle could also push for a similar move that would supplement their users with federal insurance that can be used to keep customers whole during turbulent times. Kraken is also moving ahead to become a bank as it secured Wyoming’s approval to become a special purpose depository institution (SPDI) back in 2020 and is now on track to launch ‘very soon’ according to the exchange’s chief legal officer.

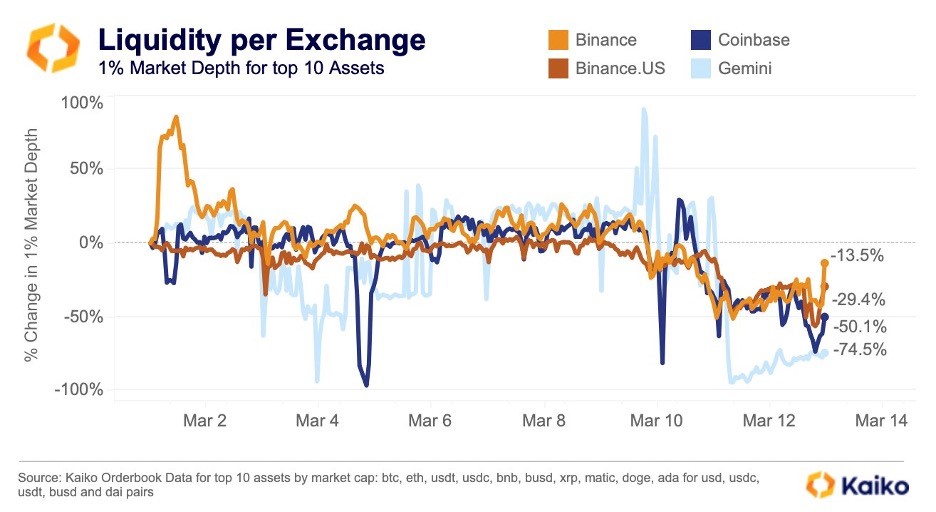

• Increased volatility: Until new banking partners emerge, liquidity will be limited across the board, resulting in higher spreads and potential aggressive market movements. Although USDC is almost fully re-pegged and is the preferred go-to for many investors, there will be increased skepticism towards holding a fully-US-based stablecoin due to the regulatory and political risk. An outflow of stablecoins leaving the ecosystem may translate to tighter liquidity conditions. Exchanges could scramble for liquidity until they fill the gap left by the collapse and takeover of SBV, Signature, and Silvergate banks.

Figure 5: Liquidity per exchange

Source: Kaiko

• Flight-to-safety: Although Bitcoin isn’t risk-free, its decentralization traits characterize it as a safe haven since the network is independent of any governing entities and, thus from potential political and economic meddling. That said, the failure of banks has reignited BTC’s value proposition as a non-state monetary system and emerging store of value. Binance already adopted this approach as its founder articulated that the exchange will swap the remaining BUSD in the $1B industry recovery fund into native assets like BTC, ETH, BNB, and others.

Next Week’s Calendar

Source: Forex Factory, CoinMarketCal

Research Newsletter

Each week the 21Shares Research team will publish our data-driven insights into the crypto asset world through this newsletter. Please direct any comments, questions, and words of feedback to research@21shares.com

Disclaimer

The information provided does not constitute a prospectus or other offering material and does not contain or constitute an offer to sell or a solicitation of any offer to buy securities in any jurisdiction. Some of the information published herein may contain forward-looking statements. Readers are cautioned that any such forward-looking statements are not guarantees of future performance and involve risks and uncertainties and that actual results may differ materially from those in the forward-looking statements as a result of various factors. The information contained herein may not be considered as economic, legal, tax or other advice and users are cautioned to base investment decisions or other decisions solely on the content hereof.

• Global crypto asset adoption rates are significantly higher than previously estimated.

• The data generally suggest that both the US and Europe may be at the cusp of mass retail adoption – a situation often referred to as “Hyperbitcoinization” in the context of Bitcoin.

• Chances are that the growth of adoption will surprise to the upside due to the fact that we are most likely at the inflection point from ”Early Adopters” to ”Early Majority”.

Trump recently made a public statement implying that 50 million Americans already held ”crypto”. The most recent surveys among US consumers seem to support this number.

It is no surprise that cryptoassets have become a major topic during the US presidential election as the parties have become increasingly aware that cryptoasset users could play a significant role at the ballot.

Both Trump and Robert Kennedy Jr. are scheduled to deliver a pro-Bitcoin speech at the upcoming Bitcoin conference in Nashville over the weekend.

It seems as if cryptoasset users are not a small minority anymore that can be ignored.

Here are some recent US bitcoin and crypto adoption surveys for comparison (% of total population in brackets):

• Security.org: 93 mn (28%)

• Unchained: 86 mn (26%)

• Statista: 53.6 mn (16%)

• Morning Consult: 44.2 mn (13%)

• Finder: 38.4 mn (11%)

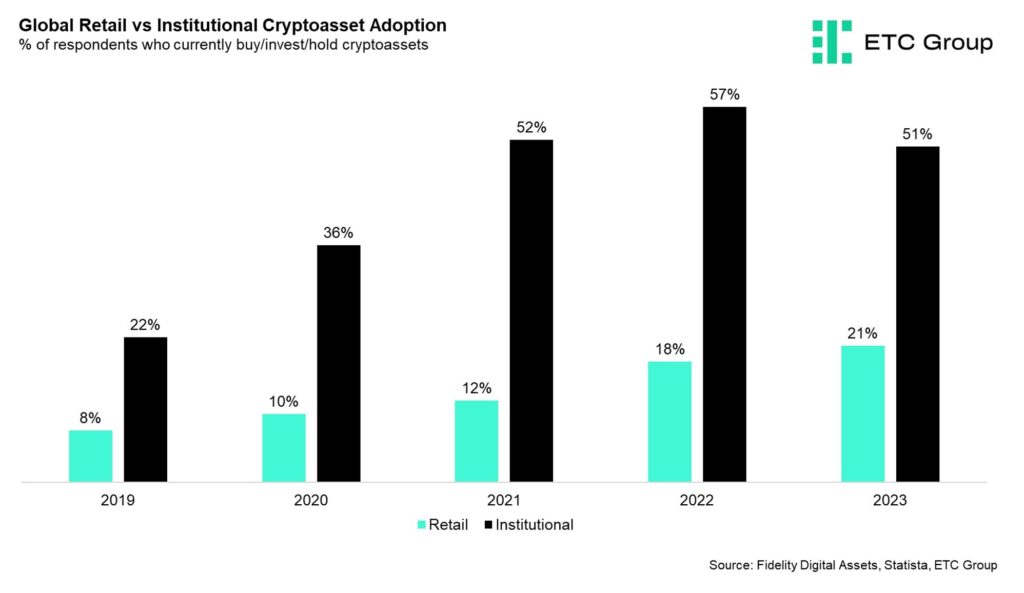

In general, cryptoasset adoption has been on the rise globally.

A recent global survey among institutional investors conducted by Fidelity even implies that 51% of surveyed institutional investors have already invested into cryptoassets such as Bitcoin.

Another recent consumer survey by Statista implies that approximately every 5th person (21%) worldwide has already invested into cryptoassets.

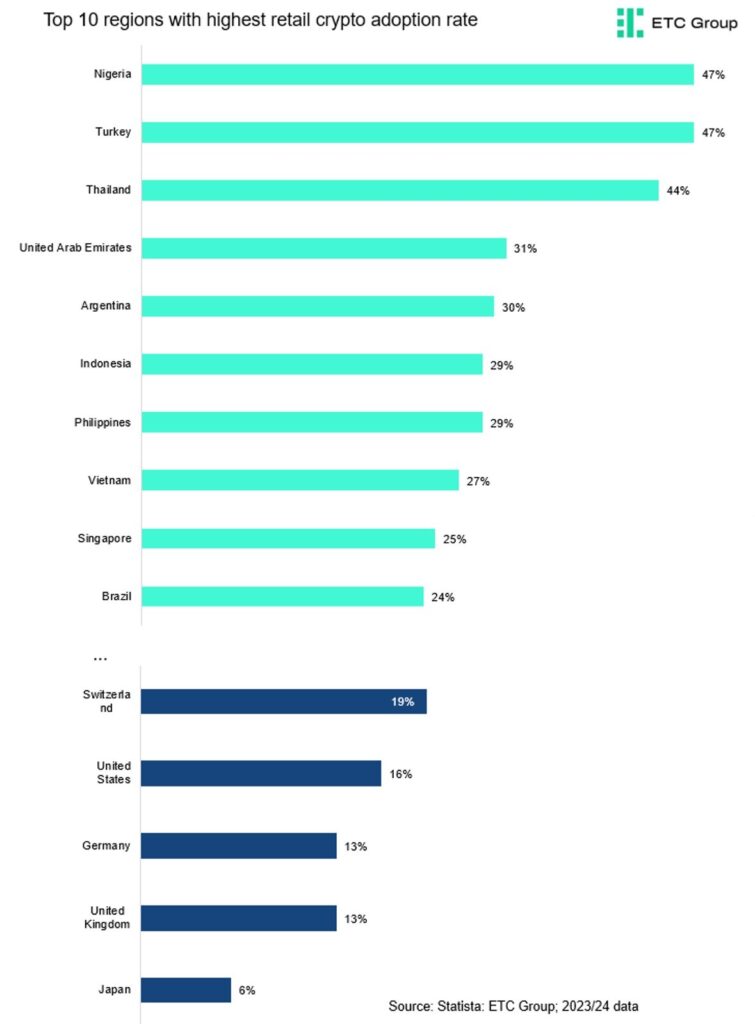

However, it’s important to highlight that among the top 10 regions with the highest adoption rates, 8 regions are developing countries.

So, cryptoasset adoption rates are even significantly higher among developing countries than in developed countries that often suffer from chronically high inflation rates and weak domestic currencies.

That being said, the data generally suggest that both the US and Europe may be at the cusp of mass retail adoption – a situation often referred to as “Hyperbitcoinization” in the context of Bitcoin.

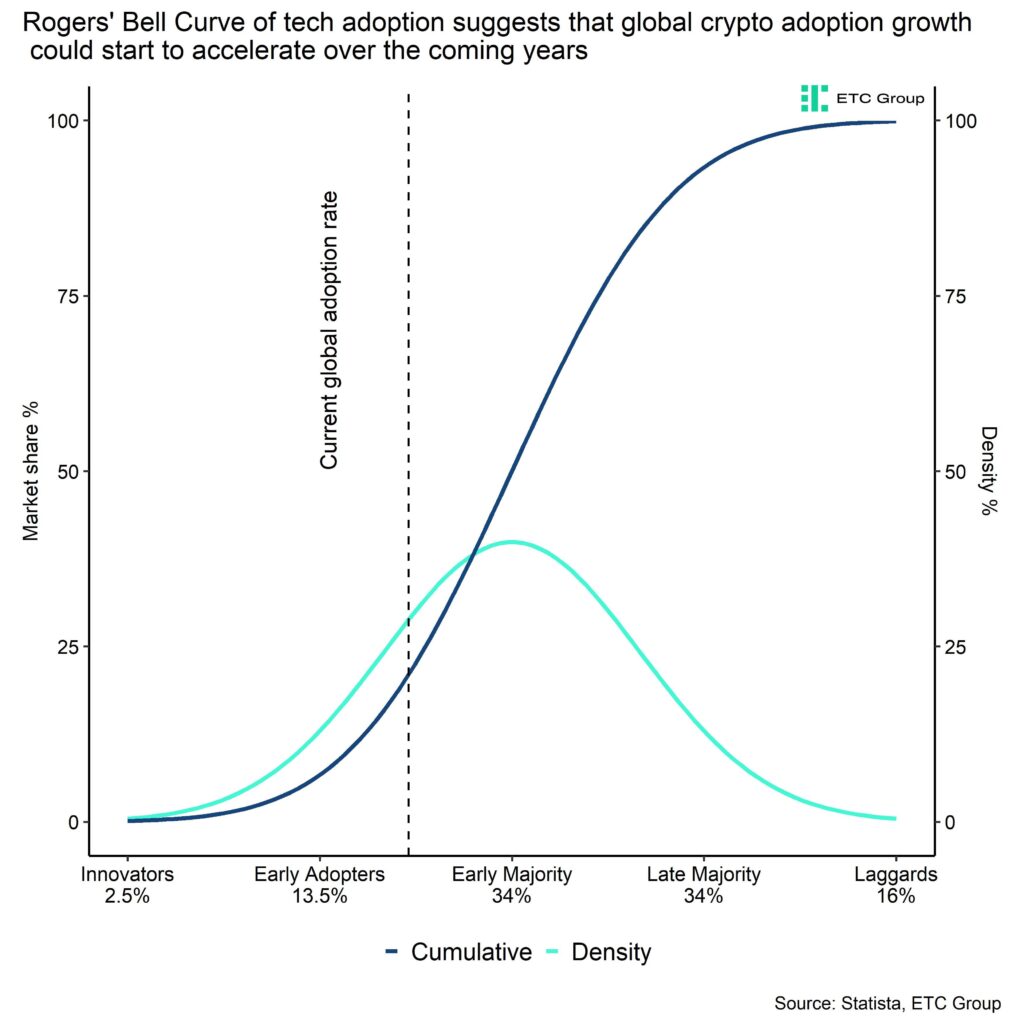

The reason is that technological adoption in general tends to accelerate at the threshold from the so-called “early adopters” to the “early majority” which is around 16% adoption rate based on the model of technological adoption famously put forth by Rogers (1962).

Global adoption rates are already at 21% while adoption rates in the US and Europe are at around 16% and 14%, respectively. So, there is a strong case for an acceleration of adoption rates in these regions and globally over the coming years.

Recent political developments in the US also imply that Bitcoin and cryptoassets are gradually becoming mainstream.

Trump has recently endorsed domestic Bitcoin mining in the US and both Democrats and Republicans have started accepting crypto payments for campaign financing.

The big success of the spot Bitcoin ETFs this year and the fact that additional types of spot crypto ETFs are being launched marks a significant shift in sentiment among US regulators in this regard.

In short, chances are that the growth of adoption will surprise to the upside due to the fact that we are most-likely at the inflection point from ”Early Adopters” to ”Early Majority”.

Bottom Line

• Global crypto asset adoption rates are significantly higher than previously estimated.

• The data generally suggest that both the US and Europe may be at the cusp of mass retail adoption – a situation often referred to as “Hyperbitcoinization” in the context of Bitcoin.

• Chances are that the growth of adoption will surprise to the upside due to the fact that we are most likely at the inflection point from ”Early Adopters” to ”Early Majority”.

To read more about suitable investment solutions by ETC Group, please click the button below:

This is not investment advice. Capital at risk. Read the full disclaimer

© ETC Group 2019-2024 | All rights reserved

Are we about to enter “Hyperbitcoinization”?

Investera i Optimism med en börshandlad produkt

JPGH ETF investerar i amerikanska tillväxtaktier

Bitcoin as a hedge against geopolitical risks?

DFND ETF investerar i flyg- och försvarsindustrin

Vilka var juni månads populäraste EFTer?

Harwood Capital Management samarbetar med HANetf för att lansera sin första UCITS ETF

Att tajma marknaden är en förlorande strategi

Börshandlade fonder ser inflöden på mer än en halv miljon troy ounce platina

The Bitcoin Macro Investor

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanVilka var juni månads populäraste EFTer?

-

Nyheter1 vecka sedan

Nyheter1 vecka sedanHarwood Capital Management samarbetar med HANetf för att lansera sin första UCITS ETF

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanAtt tajma marknaden är en förlorande strategi

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanBörshandlade fonder ser inflöden på mer än en halv miljon troy ounce platina

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanThe Bitcoin Macro Investor

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanInvestera i koppar med hjälp av börshandlade produkter

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanCETH ETP en börshandlad produkt på Ethereum som ger staking intäkter

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanSyntetiska börshandlade fonder: Vad det är, hur det fungerar