Nyheter

Visa is still committed to crypto, Coinbase lists EUROC, and More!

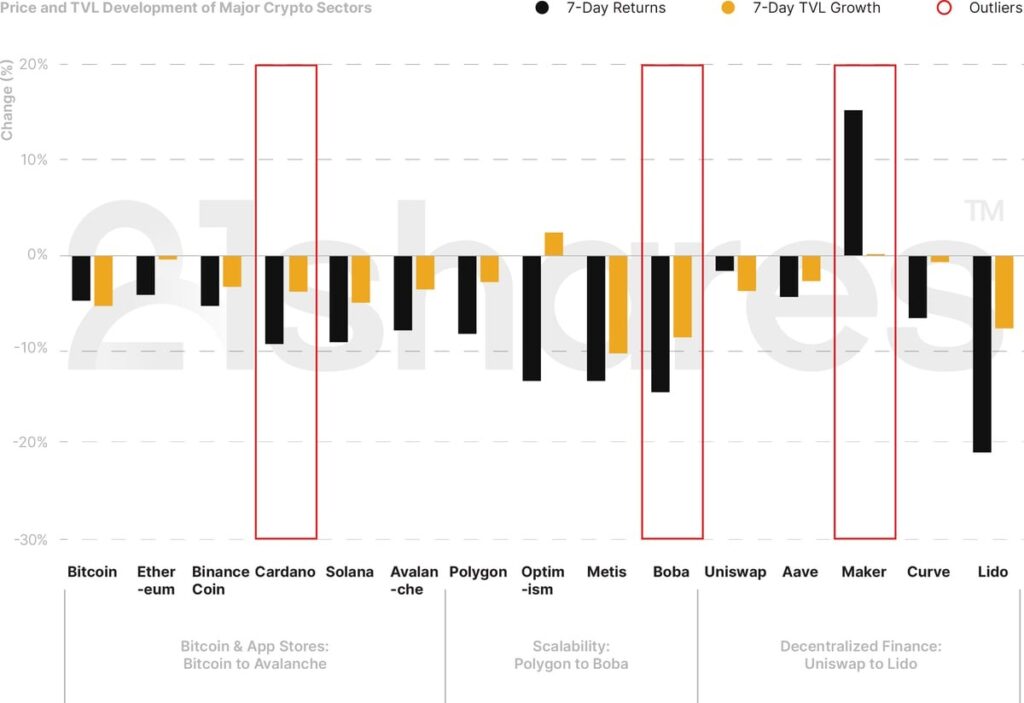

Markets suffered from increased selling pressure this week on the back of bankruptcy fears looming over crypto bank Silvergate which has been dragged down by the FTX collapse and the recent regulatory crackdown in the US. Over the past week, Bitcoin and Ethereum dipped by 4.7% and 4%, respectively. This week’s biggest winner was MakerDAO (ticker: MKR), which saw returns increase by 15%. The leading factor to MKR price action may be attributed to MakerDAO’s plans to allow users to borrow DAI against its governance token MKR. The paradox is that this yet-to-be-implemented move may cause a liquidity risk if the token drops significantly. Moreover, last month, we learned that MakerDAO registered $19M in profits in 2022. The cryptoassets that suffered the most losses last week were Boba (-14%) within scaling solutions and Cardano (-9%) among data platforms.

Figure 1: Weekly TVL and Price Performance of Major Crypto Categories

Source: 21Shares, CoinGecko, DeFi Llama. Close data as of March 7.

Key takeaways

• Bankruptcy fears loom over crypto bank Silvergate as it discontinues its exchange network platform in what they described as a risk-based decision.

• Account Abstraction arrives on Ethereum; Polygon releases web3 identification service

• Uniswap releases mobile wallet app, considering an expansion to Avalanche

• Magic Eden embarks on a month of “Mint Madness,” showcasing collections across Polygon, Ethereum, and Solana.

.

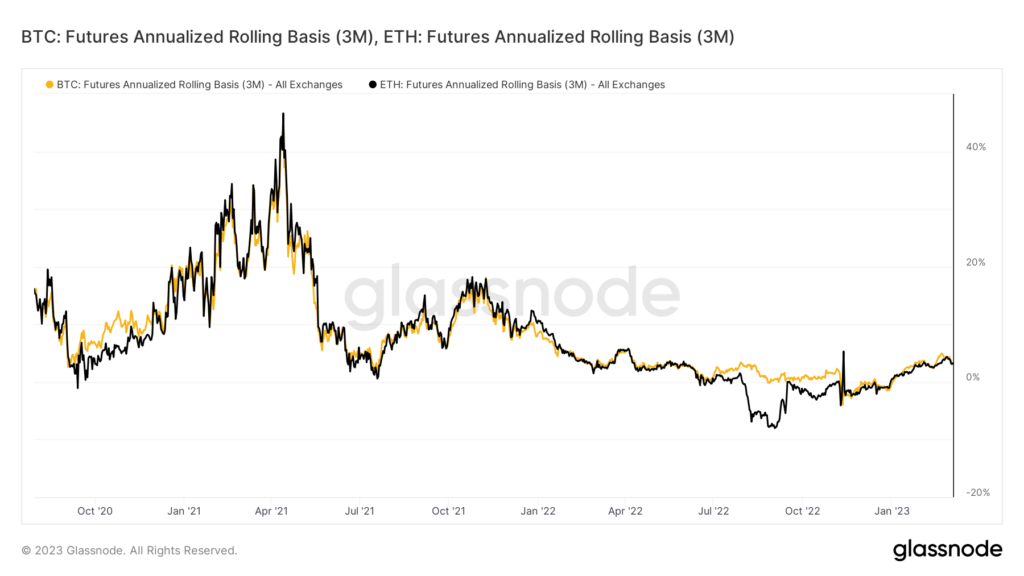

Spot and Derivatives Markets

Figure 2: Bitcoin and Ethereum Futures Annualized Rolling Basis

Source: Glassnode

The futures market for Bitcoin and Ethereum is in backwardation resulting in a positive annualized yield of 3% over the past three months. Traders profit from rolling over to cheaper long-dated futures contracts vs. the spot price of both BTC and ETH. Namely, the expected future price of both assets is cheaper than the current spot price, so investors get the same quantity of the underlying assets at a cheaper cost of capital. Backwardation can occur as a result of a higher demand for BTC and ETH in the spot market than the contracts maturing in the future through the futures market. This is a testament to a spot-driven rally since the start of the year.

On-chain Indicators

Figure 3: USDC, BUSD, and USDT Market Capitalization

Source: Glassnode

Over the past year, the channel size of the Lightning network has increased by over 80%. In other words, off-chain BTC transactions can now hold almost 0.072 BTC per channel, as shown in Figure 3. Moreover, Xapo Bank, a leading Bitcoin custodian, and licensed private bank announced that it has started using Lightspark to offer Lightning-based Bitcoin payments.

Next Week’s Calendar

Source: Forex Factory

Read our full report here

Research Newsletter

Each week the 21Shares Research team will publish our data-driven insights into the crypto asset world through this newsletter. Please direct any comments, questions, and words of feedback to research@21shares.com

Disclaimer

The information provided does not constitute a prospectus or other offering material and does not contain or constitute an offer to sell or a solicitation of any offer to buy securities in any jurisdiction. Some of the information published herein may contain forward-looking statements. Readers are cautioned that any such forward-looking statements are not guarantees of future performance and involve risks and uncertainties and that actual results may differ materially from those in the forward-looking statements as a result of various factors. The information contained herein may not be considered as economic, legal, tax or other advice and users are cautioned to base investment decisions or other decisions solely on the content hereof.

WDAF ETF investerar i Asiens försvarsindustri

BlackRock utökar tillgången till systematisk aktiv investering för europeiska investerare

JEIE ETF är en eurohedgad månadsutdelare som investerar i USA

Tre av ARK Invests UCITS-ETFer deltar i SpaceX-börsintroduktionen, den största noteringen i historien

XGLA ETF syftar till att uppnå kapitaltillväxt

USA satsar 2 miljarder dollar på kvantdatorer – så kan investerare dra nytta av utvecklingen

Extrema skillnader: Varför presterar Europas kvantdator-ETFer så olika?

Fastställd utdelning i MONTDIV maj 2026

QQCC ETF följer företag världen över som är aktiva inom kvantberäkning

Varför Plus500 är en dröm för finans-affiliate

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanUSA satsar 2 miljarder dollar på kvantdatorer – så kan investerare dra nytta av utvecklingen

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanExtrema skillnader: Varför presterar Europas kvantdator-ETFer så olika?

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanFastställd utdelning i MONTDIV maj 2026

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanQQCC ETF följer företag världen över som är aktiva inom kvantberäkning

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanVarför Plus500 är en dröm för finans-affiliate

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanETFer för fotbolls-VM 2026

-

Nyheter3 veckor sedan

Nyheter3 veckor sedan21shares produkter nu finns tillgängliga hos Revolut

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanOlja och Hormuzsundet fick flest sökningar i maj 2026