Nyheter

Value Renaissance

ETF Securities Equity Research – Value Renaissance

Highlights

- The rebound of value stocks suggests the style shift is pricing a moderate recovery in earnings.

- Sector selection and sentiment has driven the shift in style bias in favour of growth stocks over the past decade.

- Widest historical Price to Book (P/B) spread confirms Value is trading at a steep discount to Growth.

- Global macro factors support the case for a return to value investing but there are risks on the horizon.

Value investors are anticipating a change in the cycle

The key to long term investment gains is ingrained in retaining a disciplined strategy. The main but contrasting investment approaches are value and growth investing. Value investing involves buying stocks at a discount to market price and such discounts can be identified by using multiples (of earnings, cash flow and book value). Growth investing involves buying companies undergoing above average growth in earnings and are identified by high profitability margins and return on equity. Owing to its inherently higher operating leverage, historically Value outperforms Growth ahead of a turn in the profit cycle (with a lead of about 2 years). As the global macro environment improves, we are seeing emerging signs of value stocks being bid up by investors as they try to capitalise on the recovery in global economic activity. ´

(Click to enlarge)

There has been a bias towards growth investing over the past decade, leading some to question if value investing is dead.

Sector selection held value back

Value oriented indices currently have a higher weighting to finance and energy sectors than growth oriented indices. Technology and consumer discretionary stocks account for the highest weights in growth oriented indices.

(Click to enlarge)

Falling oil prices, and difficulties in the banking sector since the global financial crisis, led to a period of earnings deceleration among the value oriented finance and energy sectors. On the other hand, technology and consumer discretionary stocks posted stronger earnings tilting investor preferences towards growth stocks since 2008. Consequently, sector selection was largely responsible for the recent style bias in favour of growth stocks. We don’t think that there has been a breakdown in the fundamentals of value investing but the style has been unpopular due to sector-specific reasons. During the dot com mania of the late 90’s, value investors suffered greatly as they missed out on the rally of technology stocks whose weighting was nearly 50% of the MSCI World growth index. However, as the bubble deflated, the weight of the technology sector reduced to around 20% and Value came back in favour.

Sentiment has had a part to play in the style shift since 2008, as investors have been exposed to the dominance of central bank policy, negative interest rates, lower commodity prices and weaker expectations of economic growth. In this scenario investors have resorted to investing in growth stocks and capturing yield via bond proxies within a mix of both value (utilities, telecom, real estate) and growth (consumer staples, and healthcare) equity sectors.

Value at a bargain but not for long

Value stocks are trading at their steepest discount in history to Growth. On analysing the P/B ratios of stocks across US, Europe and Japan, we found that the gap between the cheapest part of the global equity market and the most expensive is currently at its widest level since 1986. This suggests value stocks are trading at an unprecedented discount relative to its expensive peers. The last occasions we witnessed spreads come anywhere close were during the technology bubble of the late 90’s and prior to the global financial crisis in 2008.

(Click to enlarge)

Value will benefit from higher rates

Strong US economic data, coupled with Trump’s pro-growth mandate have raised expectations for higher global growth rates accompanied by increasing inflation. The imminent US rate hike in December has become a near certainty and a higher inflation outlook has fuelled the prospects of additional rate hikes by the Fed next year. We expect value to benefit as the rate tightening cycle continues in the US. History shows that, in the 6 to 12-month period following the start of the US rate tightening cycle, Value has outperformed Growth.

(Click to enlarge)

We are currently seeing early signs of Value outpacing Growth as the rhetoric for additional rate hikes in 2017 sets in, similar to 1986, 1999 and 2004.

Macro factors support Value’s reversion to the mean

The trajectory of bonds yields in the US and Europe have a strong relationship with the relative valuation spread of Value versus Growth, based on Price to Earnings (P/E). The recent rise in bond yields sparked by the risk-on environment, subsequent to Trump’s presidential victory, has been closely tracked by the rising performance of value versus growth stocks. We expect this trend to continue to benefit value stocks as they displace the defensive bond-proxy trades towards more cyclically oriented value stocks. In addition, we expect the steepening of the yield curve to benefit financial stocks that are known to represent a large part of the value style.

(Click to enlarge)

Fundamentals intact but risks linger

Despite the prolonged underperformance of value investing since the global financial crisis, we believe the fundamentals remain intact. The historical rotation of investing style bias is reflective of the performance of the main underlying sectors within each style. While Growth and Value are not trading at a significant discount to each other, Value is clearly trading at an unprecedented discount to its historical spread. Investors are picking up on the trend, evident from the sharp reversal in the performance of Value in 2016. Over time we have observed a shift towards value investing to serve as a timely indicator of an initial acceleration in global earnings. We feel the current shift in style is a precursor of a continued recovery.

While improving global macro data is a catalyst for Value, we acknowledge the risk to the scenario remains that the market could be overpricing the rate rising cycle and the recovery in earnings momentum. We also remain extremely cautious of the euphoria surrounding Trump’s victory and remain uncertain of his ability to implement all his pro-growth policies that are subject to raising the US debt ceiling. Also, the reversal of the bond proxy trades skewed towards value sectors such as utilities, telecom and real estate could negatively impact Value’s upside performance. Despite the looming risks, we maintain our stance that growth stocks have run ahead of its course and Value offers an attractive entry point with the potential for a meaningful recovery to the upside.

Important Information

General

This communication has been issued and approved for the purpose of section 21 of the Financial Services and Markets Act 2000 by ETF Securities (UK) Limited (“ETFS UK”) which is authorised and regulated by the United Kingdom Financial Conduct Authority (the “FCA”).

Bitcoin’s record-breaking rally and resilient investor base reveal a maturing market. Despite brief drawdowns, over 90% of holders remain in profit, and institutional inflows continue to absorb volatility. With downside risk compressing, even a modest Bitcoin allocation will meaningfully boost portfolio efficiency across cycles.

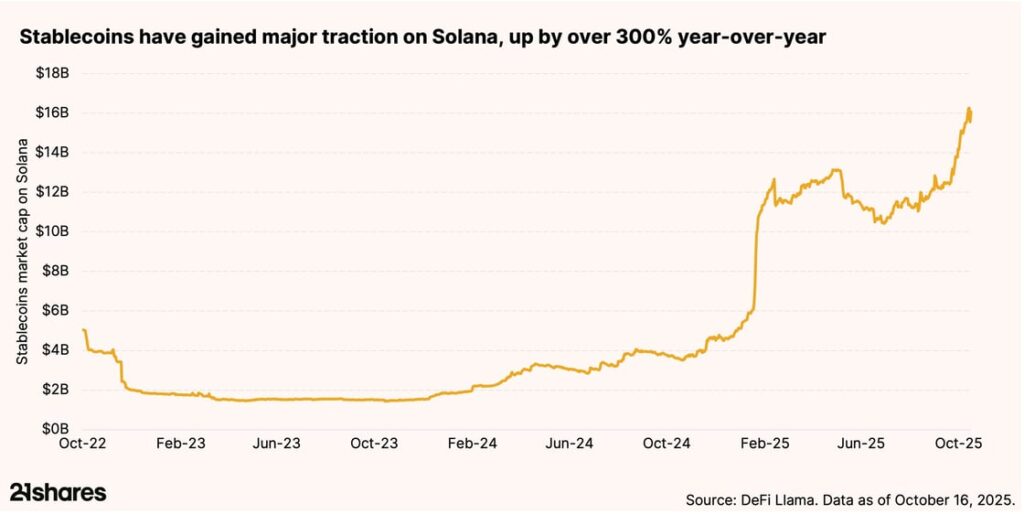

Why is retail finance booming on Solana?

Solana’s low fees and lightning-fast transactions are powering real-world payments. With $16 billion worth of stablecoins traded on the network, Solana is bridging crypto and commerce, driving retail adoption at an unprecedented scale. This is exactly why legacy companies like Shopify and PayPal have chosen to integrate the blockchain into their businesses.

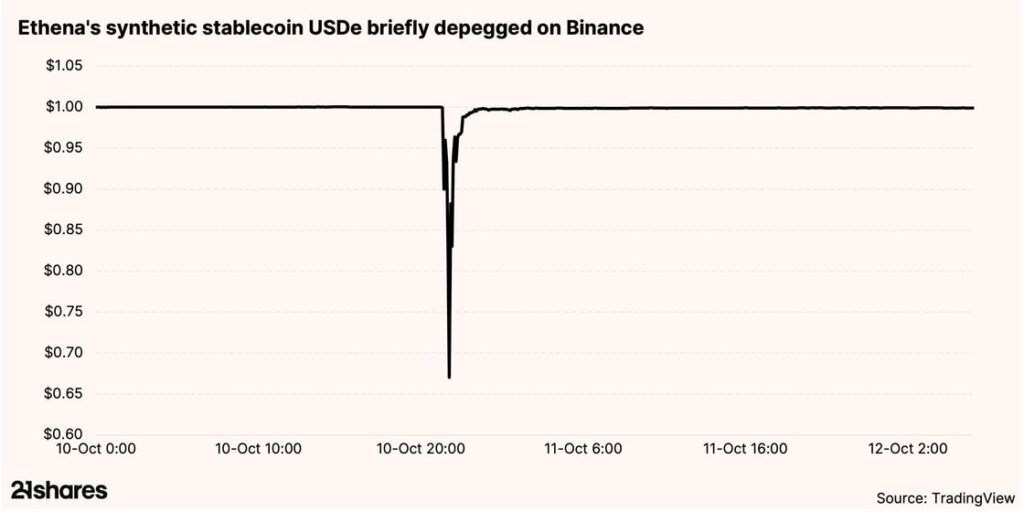

Why did Ethena’s stablecoin remain stable onchain but depegged on Binance?

On October 10, Ethena’s USDe saw a sharp depeg on Binance’s centralized exchange, plunging to $0.65, while staying stable across all decentralized finance platforms. The cause wasn’t a protocol flaw but thin centralized liquidity. The incident highlights how decentralized systems can better withstand volatility, offering transparency and resilience during market stress.

Research Newsletter

Each week the 21Shares Research team will publish our data-driven insights into the crypto asset world through this newsletter. Please direct any comments, questions, and words of feedback to research@21shares.com

Disclaimer

The information provided does not constitute a prospectus or other offering material and does not contain or constitute an offer to sell or a solicitation of any offer to buy securities in any jurisdiction. Some of the information published herein may contain forward-looking statements. Readers are cautioned that any such forward-looking statements are not guarantees of future performance and involve risks and uncertainties and that actual results may differ materially from those in the forward-looking statements as a result of various factors. The information contained herein may not be considered as economic, legal, tax or other advice and users are cautioned to base investment decisions or other decisions solely on the content hereof.

33GI ETF köper bara eurodenominerade företagsobligationer som förfaller 2033

Tre nya börshandlade fonder från Xtrackers

Bitcoin within 15% of its all-time high: Should you still allocate?

HANetfs Hector McNeil förklarar hur ETFer genererar hög avkastning med covered calls

JPEY ETF högavkastande företagsobligationer vautasäkrade till Euro

De bästa lågvolatilitets ETFer på marknaden

Fokus mot en helt ny börshandlad produkt i september 2025

M5TYs senaste utdelningstakt (55 %) belyser covered call-strategins inkomstpotential

Could Bitcoin be the key to your dream house?

Börshandlade fonder för europeiska small caps

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanDe bästa lågvolatilitets ETFer på marknaden

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanFokus mot en helt ny börshandlad produkt i september 2025

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanM5TYs senaste utdelningstakt (55 %) belyser covered call-strategins inkomstpotential

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanCould Bitcoin be the key to your dream house?

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanBörshandlade fonder för europeiska small caps

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanLevler noterar ytterligare fyra börshandlade fonder i Sverige

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanThe Investment Case for TLT (Long-Dated Treasury Bonds)

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanMiners Find Their Mojo as Gold Consolidates