Nyheter

Special Report: What Does the Court’s Order Mean for XRP and the Broader Crypto Industry?

One of the main stories this week was a U.S. court decision in the Ripple case involving the U.S. Securities and Exchange Commission (SEC). Notably, U.S. District Court Judge Analisa Torres issued a summary judgment opinion holding that the XRP token, by itself, was not a security under U.S. law. Ripple’s XRP token soared by over 50% this past week. Before we elaborate on what happened, why it matters, and what to expect, here is an overview of the broader market last week.

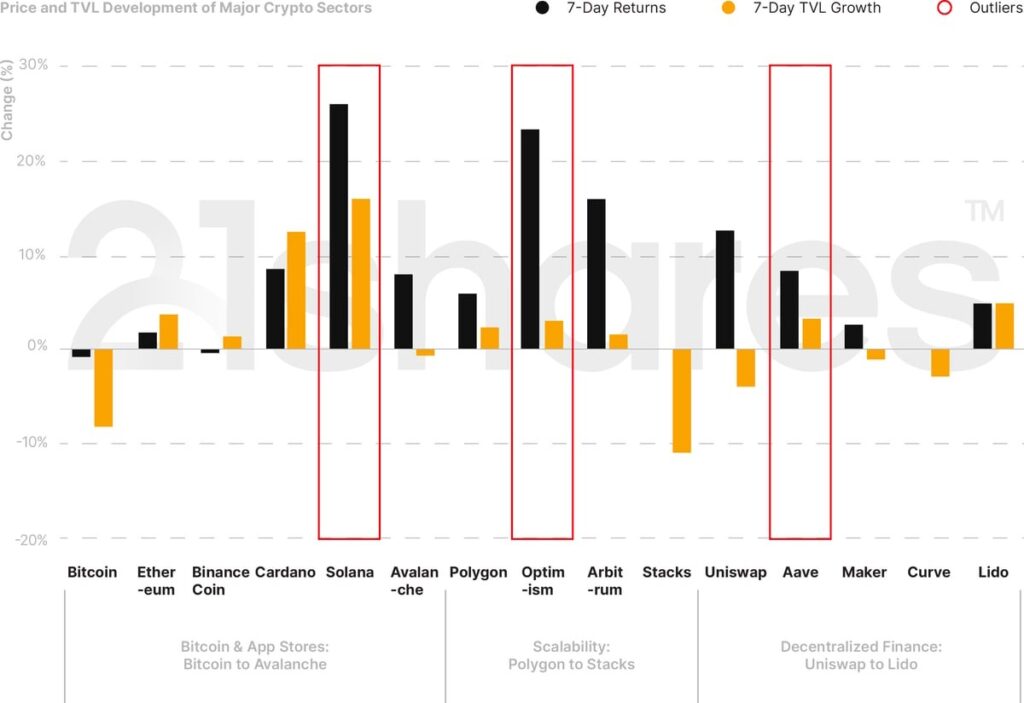

The biggest gainers of last week were Solana (+26%), Optimism (+23%), and Aave (+8%). Given it was classified as a security in recent lawsuit filings by the SEC, Solana, among other tokens like Cardano and Polygon, enjoyed a recovery following the news. Aave’s jump in price and assets under management, as shown in Figure 1, is influenced by the launch of Aave’s GHO stablecoin on the Ethereum Mainnet.

Figure 1: Weekly Price and TVL Developments of Cryptoassets in Major Sectors

Source: 21Shares, CoinGecko, DeFi Llama. Close data as of July 17, 2023.

What Happened

• For the Ripple case, on July 13, Judge Torres issued a summary judgment order that was partly in favor of the SEC and partly in favor of Ripple. Specifically, Judge Torres distinguished between the target of an investment contract (e.g., XRP as a token) versus the sale and marketing of that asset (e.g., the investment contract around the sale or offer of XRP). The former was not held to be a security, but the latter was in certain circumstances. Judge Torres’ decision also held that there were disputes of material fact that were not appropriate to resolve on summary judgment, so there could be a trial relating to a few additional issues (including whether Ripple’s founders aided and abetted Ripple’s securities law violations).

• Key takeaways from the order:

- Programmatic sales (e.g., those sold on exchanges) and certain other distributions of XRP (e.g., to employees, etc.) did not constitute a securities offering.

- Institutional sales constituted a securities offering.

- The Court left open the question of whether secondary market sales of XRP constituted a securities offering, explicitly stating that that question was not before the Court.

• Short-lived recovery following a prolonged decline: Over the past few months, Bitcoin has been experiencing a slow recovery after over a year of decline. On July 13, Bitcoin reached $31.45K, the highest since May 2022. Ethereum, on the other hand, surpassed the $2K, a level last seen in April following the Shanghai upgrade.

Figure 2: Bitcoin and Ethereum’s Price (3 Years)

Source: Glassnode

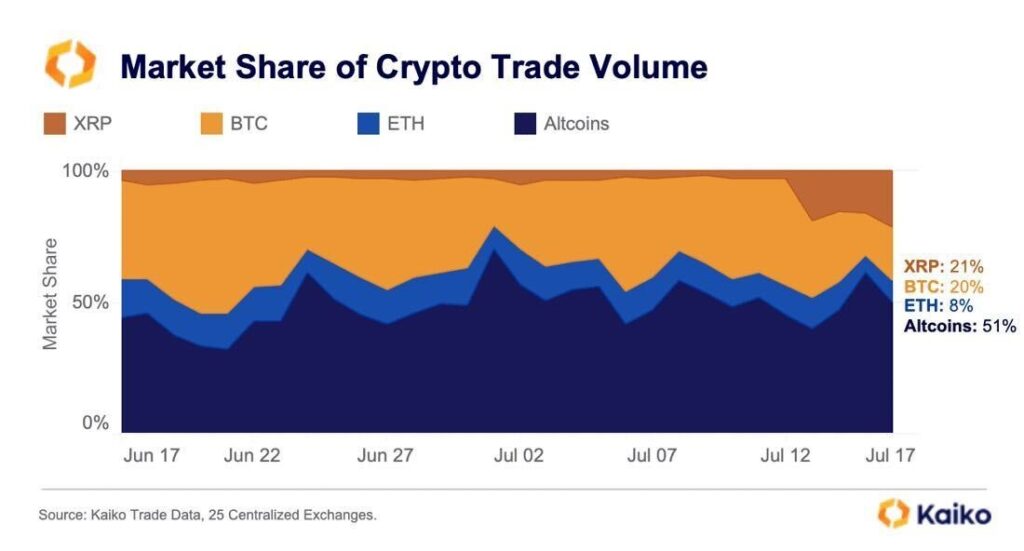

• How did “altcoins” react? XRP led the market-wide recovery, increasing close to 100%, generating more volume than Bitcoin and Ethereum, as shown in Figure 2. Other assets previously deemed securities, such as Solana, Cardano, and Polygon, were also positively impacted. The news of the ruling led them to soar by roughly close to 30% each over the following 48 hours, to then retrace over the weekend. Finally, XRP surpassed BNB in its ranking by market value to regain its position as the fourth largest cryptoasset, while its open interest for XRP futures soared by more than 90% following Judge Torres’ verdict.

Figure 3: Market Share of Crypto Trade Volume

Source: Kaiko

What to Expect

• Potential Relisting of XRP Across US-Based Exchanges

Given the recent court decision, we may expect a reversal on relisting the XRP token. The impact could extend along to include the suite of the other assets allegedly deemed as a security by the SEC in their legal dispute against Coinbase and Binance, such as Solana, Matic, Cardano, and a dozen others.

• Revised Valuations

The implications of this case have the potential to fundamentally reshape the strategies employed by foundations and developers when bootstrapping their services and products. In a scenario where projects choose to launch their applications without a token, they would likely opt for fundraising through traditional venture capital (VC) and angel rounds. Furthermore, bypassing the token in the initial stages of the project could trigger a significant shift in investor valuations of existing protocols, prompting a closer examination of the project’s underlying fundamentals. Key factors such as recurring revenue and user retention, measured through active and returning users, would take precedence in this revised valuation framework.

For further insights on applying valuation frameworks to digital assets, refer to our State of Crypto Issue 7.

• New Token Economics and Go-To-Market Strategies

If the ruling remains unchanged, projects will likely be encouraged to adopt community-owned governance models, driven by the need to accommodate ‘asset morphing.’ The latter is a concept argued as part of the unconcealed Hinman documents that outline how certain assets can transition from reflecting security characteristics to representing commodities as decentralization progresses.

Moreover, as the sale of XRP to institutional investors was deemed an unregistered sale of securities, projects may reconsider raising equity through primary (non-exempt) sales involving private and venture capital. Instead, they might prioritize a sustainable protocol path that generates additional revenue from the outset, with less emphasis on subsidized demand to incentivize user adoption and capital migration during the early growth stages.

Uniswap is a compelling case study where they refrained from launching a token until after an extensive two-year period dedicated to refining their platform through user iterations. This meticulous approach has proven instrumental in establishing Uniswap as one of the most prosperous decentralized exchanges, boasting a substantial user base with consistently high daily activity levels.

Consequently, we foresee two potential outcomes resulting from this anticipated shift in market behavior. First, more projects at the application layer could postpone token launches until they establish alignment between their product’s core services and market demand. Tokens would then serve as a must-have utility, enabling users access to a given product suite rather than solely serving as governance tokens. The argument changes regarding smart-contract platforms as a token is needed to maintain security, decentralization, and stakeholders’ alignment. So instead, we could see more emphasis on secondary market sales for these types of tokens instead of the token-as-fundraising model witnessed in 2017.

Finally, established projects may overhaul their entire business models to enhance token value capture. A notable example is Polygon, which has unveiled a new network architecture where the token plays a more prominent and active role within the ecosystem. Within the emerging ecosystem, POL will serve as the essential asset for validating interconnected chains across the interoperable Polygon universe, thereby fostering increased engagement and participation among token holders.

Bookmarks

• Want to learn more about Ripple? Read our investment thesis here.

• Celsius has been selling its assets as part of its bankruptcy proceedings. You can track the massive sales in our dashboard here.

• Learn more about Ethereum’s Liquid Staking Derivatives, which now constitute the largest DeFi sector by AUM and are expected to continue proliferating as the ETH staking ratio grows. Check out our dashboard here.

• We had Blockdaemon as our guest in last week’s Analyst Call. Watch here.

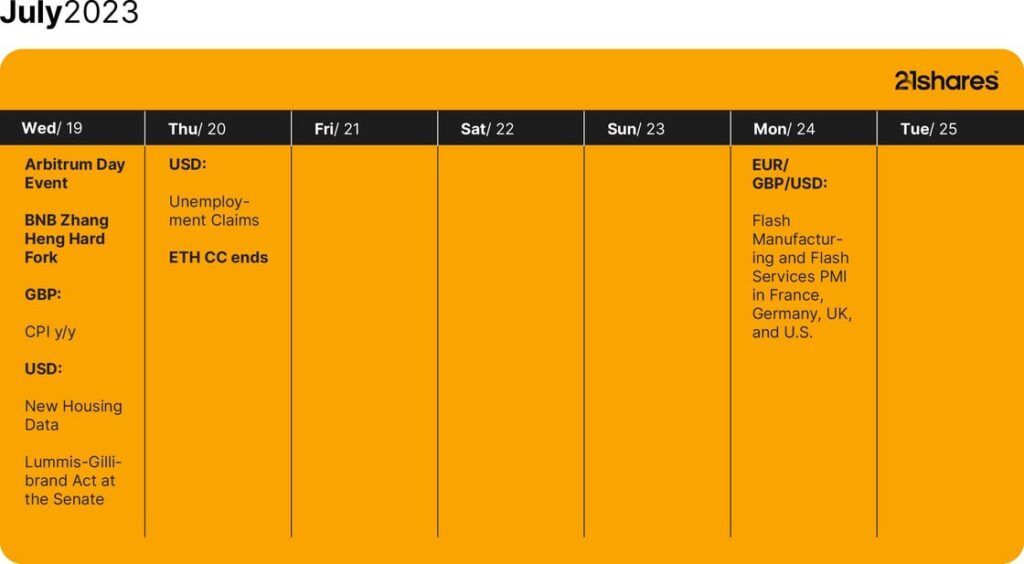

Next Week’s Calendar

These are the top 3 events we’re monitoring for next week.

• Polygon 2.0 last week of announcements: we should learn more about Polygon’s new governance system.

• ETH CC: the largest ETH annual conference, which ends on the 20th, should continue to reveal more details about the exciting new primitives and technologies of the Ethereum ecosystem.

• Lummis-Gillibrand Act: Sens. Cynthia Lummis and Kirsten Gillibrand will bring a revised version of their comprehensive crypto regulatory bill to the Senate on Wednesday.

Source: Forex Factory

Research Newsletter

Each week the 21Shares Research team will publish our data-driven insights into the crypto asset world through this newsletter. Please direct any comments, questions, and words of feedback to research@21shares.com

Disclaimer

The information provided does not constitute a prospectus or other offering material and does not contain or constitute an offer to sell or a solicitation of any offer to buy securities in any jurisdiction. Some of the information published herein may contain forward-looking statements. Readers are cautioned that any such forward-looking statements are not guarantees of future performance and involve risks and uncertainties and that actual results may differ materially from those in the forward-looking statements as a result of various factors. The information contained herein may not be considered as economic, legal, tax or other advice and users are cautioned to base investment decisions or other decisions solely on the content hereof.

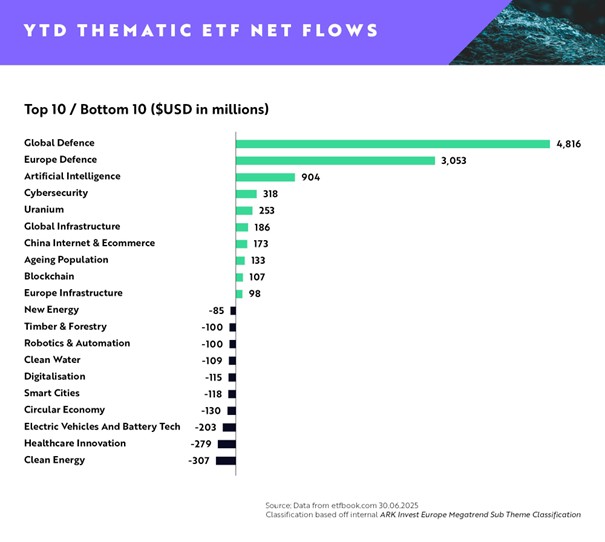

• Top Performer: Defence (+$7.87 billion)

• Emerging Themes: Cybersecurity (+$318 million), Uranium (+$253 million)

European thematic UCITS ETFs posted a dramatic resurgence in the first half of 2025, with net inflows of $8.73 billion year-to-date, according to ARK Invest Europe’s latest quarterly update detailing H1 2025 European thematic ETF flows.

The turnaround marks a decisive reversal from the muted flows of 2024 ($308 million net outflows for the whole of 2024), as investors rotate back into forward-looking, innovation-driven themes with clearer earnings visibility.

Defence remains the dominant thematic allocation, capturing $7.87 billion in combined net inflows between Global ($4.81 billion) and European ($3.05 billion) defence ETFs underscoring its evolution from a tactical trade to a structural portfolio allocation. Maintaining its position as the defining technological theme, AI ETFs saw $904 million in net inflows, with investor appetite fuelled by relentless innovation in large language models, robotics, and autonomous systems.

In the same period, Cybersecurity ETFs continued to rebuild momentum after significant outflows in 2024 ($311 million net outflows for H1 2024), drawing $318 million, reflecting growing investor conviction in cybersecurity as a structural necessity amid rising digital threats.

Clean Energy ETFs saw outflows of $307 million. As policy momentum stalls in key markets, investors are increasingly selective within the energy transition space. Capital is rotating toward subsectors with clearer economic moats, such as nuclear and grid infrastructure. Supporting this sentiment, Uranium ETFs rank fifth at $253 million, reflecting growing investor interest in the nuclear sector as a potential solution to global energy needs.

Healthcare Innovation ETFs recorded net outflows of $279 million. The drawdown reveals investor caution around legacy biotech firms with uncertain drug pipelines and reimbursement risks. Interest is shifting toward AI-driven healthcare platforms offering faster innovation cycles and more scalable business models.

Electric Vehicles and Battery Tech ETFs saw net outflows of $203 million as investor enthusiasm cools amid subsidy rollbacks and plateauing EV demand in major markets. Persistent concerns around battery raw materials and production bottlenecks have further weighed on the theme.

Rahul Bhushan says, “After a cautious 2024, it’s evident that investors are re-engaging with innovation themes that offer clearer earnings visibility and resilience in an increasingly complex macro landscape. We’re seeing investor conviction in megatrends with structural tailwinds, particularly defence, AI, and energy security. Thematics are no longer just tactical bets, they’re core strategic exposures.”

2025/2024 Comparative Study

Thematics are back

After a weak 2024, investor appetite for thematic risk has returned in force:

• H1 2025 total net inflows: +$8.74B

• That’s a sharp reversal from -$791M in H2 2024 and only +$483M in H1 2024

• The rotation is clear: capital is moving back into forward-looking themes with stronger earnings visibility.

Defence is now a structural trade

• Global and Europe Defence saw a combined $7.87B in inflows in H1 2025 and $1.59B in June alone.

• This continues a multi-quarter surge as geopolitical tensions, rising military budgets, and renewed industrial policy drive long-term allocations.

• Defence is no longer a tactical trade—it’s becoming a core exposure.

AI inflows normalise, but conviction remains

• Artificial Intelligence ETFs drew $904M in H1 2025, following $1.47B in H1 2024.

• Inflows may be slowing, but investor conviction is holding firm.

• With earnings delivery now catching up to narrative, AI remains a centrepiece of thematic portfolios.

Cybersecurity shows signs of stabilisation

After brutal outflows in 2024 (-$311M H1, -$260M H2), cybersecurity ETFs finally saw inflows:

• $318M in H1 2025, including $67M in June.

• This rebound suggests investors are once again prioritising digital resilience in an AI-driven world.

Infrastructure themes are quietly regaining traction

• Global and Europe Infrastructure ETFs pulled in $284M in H1 2025, following modest gains in H2 2024.

• Infrastructure is benefiting from government stimulus, defence modernisation, and the reshoring trade.

Uranium’s steady climb continues

• $253M in H1 2025, after $216M in H2 2024 and $67M in June alone.

• Indeed, the $67M in June alone nearly matches the $66M pulled in during the entirety of H1 2024.

• A rare clean energy theme that’s bucking the downtrend, reflecting growing recognition of nuclear as a pragmatic decarbonisation solution.

Clean Energy sentiment is so bad, it might be investable

• Outflows across all periods: -$307M (H1 2025), -$505M (H2 2024), -$409M (H1 2024)

• June 2025: A mere -$8M

• Sentiment is arguably as negative as it’s ever been—yet structural drivers remain in place. The setup for a contrarian rebound is building.

About ARK Invest Europe

ARK Invest International Ltd (”ARK Invest Europe”) is a specialist thematic ETF issuer offering investors access to a unique blend of active and index strategies focused on disruptive innovation and sustainability. Established following the acquisition of Rize ETF in September 2023 by ARK Investment Management LLC, ARK Invest Europe builds on over 40 years of expertise in identifying and investing in innovations that align financial performance with positive global impact.

Through its innovation pillar and the ”ARK” range of ETFs, ARK Invest focuses on companies leading and benefiting from transformative cross-sector innovations, including robotics, energy storage, multiomic sequencing, artificial intelligence, and blockchain technology. Meanwhile, its sustainability pillar, represented by the ”Rize by ARK Invest” range of ETFs, prioritises investment opportunities that reconcile growth with sustainability, advancing solutions that fuel prosperity while promoting environmental and social progress.

Headquartered in London, United Kingdom, ARK Invest Europe is dedicated to empowering investors with purposeful investment opportunities. For more information, please visit https://europe.ark-funds.com/

Defence and AI dominate as European Thematic ETF flows hit record $8.73 billion H1 2025

UBS Asset Management lanserar sin första aktivt förvaltade ETF

AZEH ETF är en aktivt förvaltad ETF som investerar i Asien ex Japan

Regan Capital debuterar i Europa med aktivt förvaltad totalavkastande inkomst-ETF

EUPD ETF köper aktier i undervärderade sektorer i USA

De bästa ETFer som investerar i europeiska utdelningsaktier

YieldMax® lanserar sin andra produkt för europeiska investerare

Big News for Nuclear Energy—What It Means for Investors

Svenska investerare — 21Shares Nasdaq Stockholm-sortiment har just blivit starkare

3EDS ETN ger tre gånger den negativa avkastningen på flyg- och försvarsindustrin

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanDe bästa ETFer som investerar i europeiska utdelningsaktier

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanYieldMax® lanserar sin andra produkt för europeiska investerare

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanBig News for Nuclear Energy—What It Means for Investors

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanSvenska investerare — 21Shares Nasdaq Stockholm-sortiment har just blivit starkare

-

Nyheter4 veckor sedan

Nyheter4 veckor sedan3EDS ETN ger tre gånger den negativa avkastningen på flyg- och försvarsindustrin

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanNordea Asset Management lanserar nya ETFer på Xetra

-

Nyheter1 vecka sedan

Nyheter1 vecka sedanHetaste investeringstemat i juni 2025

-

Nyheter1 vecka sedan

Nyheter1 vecka sedan12 000 artiklar om börshandlade fonder