Nyheter

Nordiska ETFmarknaden mars 2016

Nordiska ETFmarknaden mars 2016 Under mars uppgick ETF-handeln till ca 13,7 Mdr SEK (drygt 20 Mdr SEK i februari), varav ca 10,6 Mdr SEK omsattes i den svenska marknaden. Av den totala nordiska ETF-omsättningen var Xacts marknadsandel ca 97%. Av den totala börsomsättningen i Sverige i mars svarade ETF-handeln för ca 3,4%.

Läs mer här

(Klicka på bilden för att göra den större)

(Klicka på bilden för att göra den större)

Viktig information

Xacts börshandlade fonder är juridiskt och skattemässigt klassade som fonder. Xacts börshandlande fonder med säte i Sverige förvaltas av Handelsbanken Fonder AB och står under Finansinspektionens tillsyn. De fonder som har sitt säte i Norge förvaltas av Handelsbanken Kapitalforvaltning AS och står under tillsyn av Finanstilsynet.

En fonds historiska avkastning är ingen garanti för framtida avkastning. De pengar som placeras i en fond kan både öka och minska i värde och det är inte säkert att du får tillbaka hela det insatta kapitalet. På www.xact.se finner du informationsbroschyrer och faktablad.

Hävstångsfonder uppför sig annorlunda jämfört med fonder utan hävstång. Hävstångsfonder är därför endast lämpliga som investering om du förstår egenskaperna hos hävstångsprodukter, förstår effekterna av daglig ombalansering samt arbetar aktivt med och kontinuerligt ser över din placeringsportfölj, då hävstången gör att värdet ändras snabbare än i motsvarande placeringar utan hävstång.

Källor: Bloomberg, NasdaqOMX, Burgundy, Oslo Börs, Fondbolagens Förening samt respektive utgivares hemsida.

Total omsättning avser handelsplatserna NasdaqOMX för både Stockholm och Helsingfors, Burgundy och Oslo Börs.

Att en ETF är korsnoterad innebär att den har sin primärnotering på en annan börs.

AUM står för Assets under Management.

Xacts ETF:er rapporteras in under kategorin Aktiefonder i statistiken hos Fondbolagens Förening.

Licensvillkor:

XACT OMXS30™, XACT OMXSB™ och XACT Norden 30, (the “Products”) are not sponsored, endorsed, sold or promoted by the NASDAQ OMX Group, Inc. or its affiliates (NASDAQ OMX, with its affiliates, are referred to as the “Corporations”). The Corporations have not passed on the legality or suitability of, or the accuracy or adequacy of descriptions and disclosures relating to, the Products. The Corporations make no representation or warranty, express or implied to the owners of the Products or any member of the public regarding the advisability of investing in securities generally or in the Products particularly, or the ability of the OMXS30™, OMXSB™ and VINX30™ (the “Index”) to track general stock market performance. The Corporations’ only relationship to the party which has, or parties which have, obtained a license to use the Indices in respect of the Products (“Licensee”) is in the licensing of the NASDAQ®, NASDAQ OMX®, OMX® and VINX30™ registered trademarks, and certain trade names of the Corporations and the use of the Index which is determined, composed and calculated by NASDAQ OMX without regard to Licensee or the Products. NASDAQ OMX has no obligation to take the needs of the Licensee or the owners of the Products into consideration in determining, composing or calculating the Index. The Corporations are not responsible for and have not participated in the determination of the timing of, prices at, or quantities of the Products to be issued or in the determination or calculation of the equation by which the Products is to be converted into cash. The Corporations have no liability in connection with the administration, marketing or trading of the Products. THE CORPORATIONS DO NOT GUARANTEE THE ACCURACY AND/OR UNINTERRUPTED CALCULATION OF THE INDICES (AS DEFINED) OR ANY DATA INCLUDED THEREIN. THE CORPORATIONS MAKE NO WARRANTY, EXPRESS OR IMPLIED, AS TO RESULTS TO BE OBTAINED BY LICENSEE, OWNERS OF THE PRODUCTS, OR ANY OTHER PERSON OR ENTITY FROM THE USE OF THE INDICES OR ANY DATA INCLUDED THEREIN. THE CORPORATIONS MAKE NO EXPRESS OR IMPLIED WARRANTIES, AND EXPRESSLY DISCLAIM ALL WARRANTIES OF MERCHANTABILITY OR FITNESS FOR A PARTICULAR PURPOSE OR USE WITH RESPECT TO THE INDICES OR ANY DATA INCLUDED THEREIN. WITHOUT LIMITING ANY OF THE FOREGOING, IN NO EVENT SHALL THE CORPORATIONS HAVE ANY LIABILITY FOR ANY LOST PROFITS OR SPECIAL, INCIDENTAL, PUNITIVE, INDIRECT, OR CONSEQUENTIAL DAMAGES, EVEN IF NOTIFIED OF THE POSSIBILITY OF SUCH DAMAGES.

XACT Norden 30 är inte i något avseende garanterad, godkänd, emitterad eller understödd av OMX AB (publ) (”OMX”) eller Oslo Børs ASA (”OB”) och OMX eller OB lämnar inga, vare sig uttryckliga eller implicita, garantier med avseende på de resultat som användningen av VINX30™ index kan ge upphov till eller med avseende på värdet av VINX30™ index vid viss tidpunkt. VINX30™ index sammanställs och beräknas av en indexberäknare på uppdrag av OMX och OB. OMX eller OB respektive indexberäknaren skall i intet fall vara ansvarig för fel i VINX30™ index. OMX eller OB respektive indexberäknaren skall ej heller vara skyldig att meddela eller offentliggöra eventuella fel i VINX30™ index. VINX™ och VINX30™ index är varumärken tillhörande OMX och OB och används enligt licens från OMX eller OB.

XACT OBX är inte i något avseende garanterad, godkänd, emitterad eller understödd av Oslo Børs ASA (”Oslo Børs”) och Oslo Børs lämnar inga, vare sig uttryckliga eller implicita, garantier med avseende på de resultat som användningen av Oslo Børs index kan ge upphov till eller med avseende på värdet av nämnda index vid viss tidpunkt. Vidare ger Oslo Børs inga garantier för handeln eller användarvänlighet för ett bestämt ändamål eller användning vad gäller Oslo Børs index eller Oslo Børs varumärken. Oslo Børs index sammanställs och beräknas av en indexproducent som beräknar indexen på Oslo Børs vägnar och Oslo Børs ger inga garantier för noggrannheten och/eller fullständigheten av Oslo Børs index eller data som ingår i dessa. Oslo Børs och den som beräknar index skall i intet fall (varken vid oaktsamhet eller annat) vara ansvarig för fel i Oslo Børs index, och skall inte heller vara skyldig att meddela eller offentliggöra eventuella fel i dessa index. OBX®, OSEBX®, OSEFX®, OSEAX® och GFBX® är varumärken tillhörande Oslo Børs och används av Handelsbanken Fondforvaltning AS enligt licens från Oslo Børs.

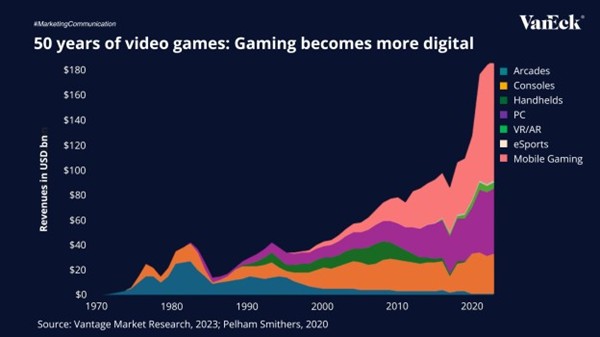

The global gaming industry has evolved into one of the world’s most dynamic entertainment sectors, expected to generate $188.9 billion in 2024 and surpass $200 billion by 2027, outpacing film and music combined.

From arcades to smartphones, the gaming industry has continuously evolved with each technological shift. Today, mobile gaming is a major player the market, currently accounting for the largest share of global revenues. As digital platforms, cloud gaming, and eSports continue to grow, gaming is establishing itself as a core part of the global entertainment economy.

Mobile gaming is leading this transformation, currently accounting for the majority of industry revenues and 40% of all global app downloads. With 5G adoption and 90% smartphone penetration expected by 2030, billions of new players will join the market, making gaming more accessible than ever.

However, the rollout of 5G also carries risks, uneven global infrastructure buildout, high capital costs for carriers, and potential fragmentation across networks could delay or limit the full realization of these benefits.

Source: Vantage Market Research, 2023; Pelham Smithers, 2020

To receive more Gold Investing insights, sign up to our newsletter.

IMPORTANT INFORMATION

This is marketing communication. Please refer to the prospectus of the UCITS and to the KID/KIID before making any final investment decisions. These documents are available in English and the KIDs/KIIDs in local languages and can be obtained free of charge at www.vaneck.com, from VanEck Asset Management B.V. (the “Management Company”) or, where applicable, from the relevant appointed facility agent for your country.

Is Mobile Powering the Future of Gaming?

Fyra nya börshandlade fonder från JP Morgan

AIFS ETF en satsning på infrastruktur för artificiell intelligens

J.P. Morgan Asset Management utökar sitt erbjudande med två nya aktiva ETFer

ISRU ETF köper aktier i stora amerikanska företag

HANetf och Infrastructure Capital Advisors samarbetar för att lansera aktivt förvaltad preferensavkastnings-ETF i Europa

De bästa lågvolatilitets ETFer på marknaden

Time in Bitcoin beats timing Bitcoin

HANetf kommenterar kopparuppgången

Fokus mot en helt ny börshandlad produkt i september 2025

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanHANetf och Infrastructure Capital Advisors samarbetar för att lansera aktivt förvaltad preferensavkastnings-ETF i Europa

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanDe bästa lågvolatilitets ETFer på marknaden

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanTime in Bitcoin beats timing Bitcoin

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanHANetf kommenterar kopparuppgången

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanFokus mot en helt ny börshandlad produkt i september 2025

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanBörshandlade fonder för europeiska small caps

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanM5TYs senaste utdelningstakt (55 %) belyser covered call-strategins inkomstpotential

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanCould Bitcoin be the key to your dream house?