Jan van Eck, CEO, provides an update on his investment outlook for 2016. The rally in commodities has done more than provide an investment opportunity; it has also driven positive performance in a number of other asset classes. Commodities Stand Out.

https://youtube.com/watch?v=ve_FNl8AsJQ

TOM BUTCHER: Jan, commodities have seen a rebound in 2016. What’s your outlook for the rest of the year?

JAN VAN ECK: We’re very happy about the first quarter rebound. We do think commodities have bottomed and there are a couple of factors to consider. What we always stress, because I think it’s the most important thing for people to understand, is the supply response. We think there has always been a growing demand for commodities around the world, whether it’s energy, natural gas, oil, or metals, such as copper. What caused prices to fall was an oversupply situation, which we think has been corrected. We’re glad to see that demand has caught up with supply.

I think the way for investors to think about this current environment is to consider this as an opportunity if one takes a much longer term perspective. We investors tend to be very focused on the short term. Energy is now very low as a percent of the overall S&P 500® Index. At its peak it was close to 16% and it’s near 6% now. Taking a multi-decade perspective tells us that energy is relatively cheap right now. Similarly, if you look at gold shares over a longer period of time, you may see that while they’ve risen a great deal this year, they may still have much further to go because they fell so far.

My Message to Investors: This is a Great Opportunity

That is my number one message to investors: This is a great longer term opportunity. Don’t obsess about the correct entry point.

BUTCHER: But global growth has been slow, debt levels have been high, and some governments have actually resorted to negative rates.

VAN ECK: We’ve seen this year a real inflection point, as Japan brought some of its interest rates negative. The question is how do you get economic growth going? After the financial crisis in the U.S., we had the same response: zero interest rates to try to stimulate economic growth. I think central banks are now basically taking it to the next level, i.e., negative interest rates. Federal Reserve Chair Janet Yellen spoke about this in her recent testimony, and former Fed Chair Ben Bernanke has been speaking about negative interest rates as well.

Negative Interest Rates May Cause Investors to Disengage

We think negative rates can be dangerous. Rather than stimulating the economy, negative interest rates, I believe, can cause people to withdraw from participating. Think about it from an investor’s perspective. It is very worrisome when a bank will only give you 99 cents at the end of the year when you gave it a dollar in January. I think that can make people take less risk rather than engage in order to help stimulate growth.

Negative interest rates are fantastic for gold because gold doesn’t pay a coupon, unlike bonds or stocks that pay dividends. Gold always has to compete with other financial assets but if financial assets are costing you money in a negative interest rate environment, we see no reason not to own gold. We think that’s one of the reasons why gold has been rallying this year.

VAN ECK: China is the second largest economy in the world and we think that every investment committee needs to have a view on China. Our view has been that, while there are some growing pains, and the devaluation of the renminbi was a major event last year, there are no systemic risks [i.e., risks inherent to China’s entire economy, rather than a single segment of the economy].

One of the things that we love to talk about is new China versus old China. New China is characterized by the consumer-driven and healthcare sectors; old China is steel, coal, and heavy manufacturing. Old China is continuing to face profitability issues. Another matter that we’ve recently been discussing is the growth of China’s overall debt levels, which are particularly concentrated in old China. There is between $1 to $2 trillion of bad debt in China right now. China’s economy amounts to $10 trillion and its overall debt level is approximately $20 trillion. These are large numbers. However, not every bad debt goes to zero, but the bad debt is very concentrated in the old economy sectors.1

We don’t think that causes a systemic risk but it may cause lumpiness in the performance of some of China’s financial assets. Because various regions will be badly affected, people who have fixed income exposure to those regions will likely be badly impacted. There are likely to be some defaults. Still, we think it’s a good thing because it’s a healthy process.

What’s Changed in our Outlook Since January

BUTCHER: Jan, you described your outlook at the beginning of 2016. How has it changed since January?

VAN ECK: Several important things happened in the first quarter. First of all, we thought that credit was very cheap, meaning interest rates had risen on MLPs [master limited partnerships] and on high yield bonds, which were almost showing signs of distress. We also said that this represented a great investment opportunity. In fact, high yield has outperformed the U.S. equity market2. Right now, I think that high risk bonds are a little less appealing today than they were when we first started the year.

Commodities Q1 Rally Creates Positive Inflection Point

Additionally, I think the equity markets still have a lot of struggling to do because price-to-earnings ratios are very high. Earnings fell last year in the U.S. They should be recovering now, looking forward over the next 12 months. Part of the reason is the strong U.S. dollar. Overall, we think equities are so-so and the U.S. economy, as well as the global economy, will muddle along.

Commodities were the big story in the first quarter. They dragged up other asset classes. For example, they helped emerging markets debt; they’ve helped Latin America. A good amount of high yield U.S. debt was energy-related, and it has rallied tremendously. It is interesting that what can be characterized as a bottom-up phenomenon of supply cuts kicking in within the commodities sector has helped other asset classes from a macro perspective.

Overall, we believe that commodities are the standout from a multi-year view. This is a great time for investors to look at them, given that we believe this is an inflection point.

BUTCHER: Thank you very much.

Market Insights

by Jan van Eck, CEO

An innovator of investment solutions, Jan van Eck has created a multitude of strategies spanning international, emerging markets, and commodities opportunities. He plays an active role in shaping the firm’s actively managed and ETF investment offerings. Jan’s research focus is on developments in China and technology’s effect on the financial services industry.

IMPORTANT DISCLOSURE

1Source: CEIC, HSBC. Data as of December 2015.

2Source: Bloomberg, March 31, 2016.

This content is published in the United States for residents of specified countries. Investors are subject to securities and tax regulations within their applicable jurisdictions that are not addressed on this content. Nothing in this content should be considered a solicitation to buy or an offer to sell shares of any investment in any jurisdiction where the offer or solicitation would be unlawful under the securities laws of such jurisdiction, nor is it intended as investment, tax, financial, or legal advice. Investors should seek such professional advice for their particular situation and jurisdiction. You can obtain more specific information on VanEck strategies by visiting Investment Strategies.

The views and opinions expressed are those of the speaker(s) and are current as of the posting date. Commentaries are general in nature and should not be construed as investment advice. Opinions are subject to change with market conditions. All performance information is historical and is not a guarantee of future results.

Please note that Van Eck Securities Corporation offers investment portfolios that invest in the asset class(es) mentioned in this post and video. You can lose money by investing in a commodities fund. Any investment in a commodities fund should be part of an overall investment program, not a complete program. Commodities are assets that have tangible properties, such as oil, metals, and agriculture. Commodities and commodity-linked derivatives may be affected by overall market movements and other factors that affect the value of a particular industry or commodity, such as weather, disease, embargoes or political or regulatory developments. The value of a commodity-linked derivative is generally based on price movements of a commodity, a commodity futures contract, a commodity index or other economic variables based on the commodity markets. Derivatives use leverage, which may exaggerate a loss. A commodities fund is subject to the risks associated with its investments in commodity-linked derivatives, risks of investing in wholly owned subsidiary, risk of tracking error, risks of aggressive investment techniques, leverage risk, derivatives risks, counterparty risks, non-diversification risk, credit risk, concentration risk and market risk. The use of commodity-linked derivatives such as swaps, commodity-linked structured notes and futures entails substantial risks, including risk of loss of a significant portion of their principal value, lack of a secondary market, increased volatility, correlation risk, liquidity risk, interest-rate risk, market risk, credit risk, valuation risk and tax risk. Gains and losses from speculative positions in derivatives may be much greater than the derivative’s cost. At any time, the risk of loss of any individual security held by a commodities fund could be significantly higher than 50% of the security’s value. Investment in commodity markets may not be suitable for all investors. A commodity fund’s investment in commodity-linked derivative instruments may subject the fund to greater volatility than investment in traditional securities.

Investing involves risk, including possible loss of principal. An investor should consider investment objectives, risks, charges and expenses of any investment strategy carefully before investing. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission of Van Eck Securities Corporation.

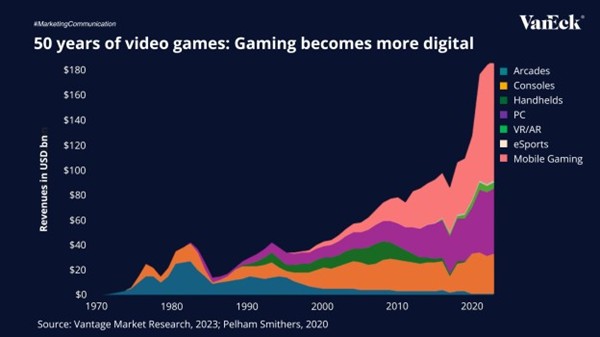

The global gaming industry has evolved into one of the world’s most dynamic entertainment sectors, expected to generate $188.9 billion in 2024 and surpass $200 billion by 2027, outpacing film and music combined.

From arcades to smartphones, the gaming industry has continuously evolved with each technological shift. Today, mobile gaming is a major player the market, currently accounting for the largest share of global revenues. As digital platforms, cloud gaming, and eSports continue to grow, gaming is establishing itself as a core part of the global entertainment economy.

Mobile gaming is leading this transformation, currently accounting for the majority of industry revenues and 40% of all global app downloads. With 5G adoption and 90% smartphone penetration expected by 2030, billions of new players will join the market, making gaming more accessible than ever.

However, the rollout of 5G also carries risks, uneven global infrastructure buildout, high capital costs for carriers, and potential fragmentation across networks could delay or limit the full realization of these benefits.

This is marketing communication. Please refer to the prospectus of the UCITS and to the KID/KIID before making any final investment decisions. These documents are available in English and the KIDs/KIIDs in local languages and can be obtained free of charge at www.vaneck.com, from VanEck Asset Management B.V. (the “Management Company”) or, where applicable, from the relevant appointed facility agent for your country.

JPM Nasdaq Hedged Equity Laddered Overlay Active UCITSETF förvaltas aktivt och investerar i en portfölj av aktier från Nasdaq 100 med en overlay-strategi. Denna strategi implementeras genom köp- och säljoptioner, med positioner som innehas under en period av tre månader. ETFen finns i både ackumulerande och utdelandeandelsklasser.

JPM US Hedged Equity Laddered Overlay Active UCITSETF förvaltas aktivt och investerar i en portfölj av aktier från S&P 500 med en overlay-strategi. Denna strategi implementeras genom köp- och säljoptioner, med positioner som innehas under en period av tre månader. ETFen finns i både ackumulerande och utdelandeandelsklasser.

nxtAssets ripple direct ETP ger enkel tillgång till utvecklingen av kryptovalutan Ripple (XRP). ETPen är fysiskt säkerställd av de underliggande kryptovalutorna. Handel är möjlig antingen i euro eller amerikanska dollar.

WisdomTree Physical Stellar Lumens ger enkel tillgång till utvecklingen av kryptovalutan Stellar. ETPen är fysiskt säkerställd av de underliggande kryptovalutorna.

Produktutbudet inom Deutsche Börses ETF- och ETP-segment omfattar för närvarande totalt 2 595 ETFer, 203 ETCer och 282 ETNer. Med detta urval och en genomsnittlig månatlig handelsvolym på cirka 25 miljarder euro är Xetra den ledande handelsplatsen för ETFer och ETPer i Europa.

iShares AI Infrastructure UCITSETF USD (Acc) (AIFS ETF) med ISIN IE000X59ZHE2, försöker spåra STOXX Global AI Infrastructure-index. STOXX Global AI Infrastructure-index spårar prestanda för företag över hela världen som är engagerade inom området AI-infrastruktur. Aktierna som ingår filtreras enligt ESG-kriterier (miljö, social och bolagsstyrning).

Den börshandlade fondens TER (total cost ratio) uppgår till 0,35 % p.a. iShares AI Infrastructure UCITSETF USD (Acc) är den enda ETF som följer STOXX Global AI Infrastructure-index. ETFen replikerar det underliggande indexets prestanda genom full replikering (köper alla indexbeståndsdelar). Utdelningarna i ETFen ackumuleras och återinvesteras.

Denna ETF lanserades den 5 december 2024 och har sin hemvist i Irland.

Investeringsmål

Fonden strävar efter att uppnå avkastning på din investering, genom en kombination av kapitaltillväxt och inkomst på fondens tillgångar, vilket återspeglar avkastningen från STOXX Global AI Infrastructure Index, fondens jämförelseindex (”Index”).

Det betyder att det går att handla andelar i denna ETF genom de flesta svenska banker och Internetmäklare, till exempel DEGIRO, Nordnet, Aktieinvest och Avanza.

Nyheter4 veckor sedan

Nyheter4 veckor sedan

Nyheter3 veckor sedan

Nyheter3 veckor sedan

Nyheter3 veckor sedan

Nyheter3 veckor sedan

Nyheter3 veckor sedan

Nyheter3 veckor sedan