Nyheter

Big Tech, Liquidations, and an Outage: What happened in crypto last week?

Last week, Big Tech dominated the headlines with its earnings for the last quarter of 2023. In this report, we’ll talk about their correlation with crypto and how other macroeconomic indicators come into play. We’ll also shed light on liquidations the market is anticipating on the back of some bankruptcy proceedings. Finally, we’ll walk you through what we know about the Solana mainnet outage.

Earnings Week Spurs Optimism

Following the latest macroeconomic data, the Federal Reserve has opted to maintain interest rates within the range of 5.25% to 5.5%. In its recent statement, the central bank underscored the necessity for additional reassuring data before considering any reduction in borrowing costs. However, there are encouraging signs suggesting the U.S. economy is surpassing expectations. Notably, January witnessed robust job creation, with ~353K new positions added, exceeding the anticipated ~185K, holding the unemployment rate steady at 3.7% against the projected 3.8%. Moreover, wage growth surged annually to 4.5%, the highest increase in two years, while the U.S. manufacturing sector exhibited resilience and momentum, with the PMI index climbing from 47.1% to 49.1%.

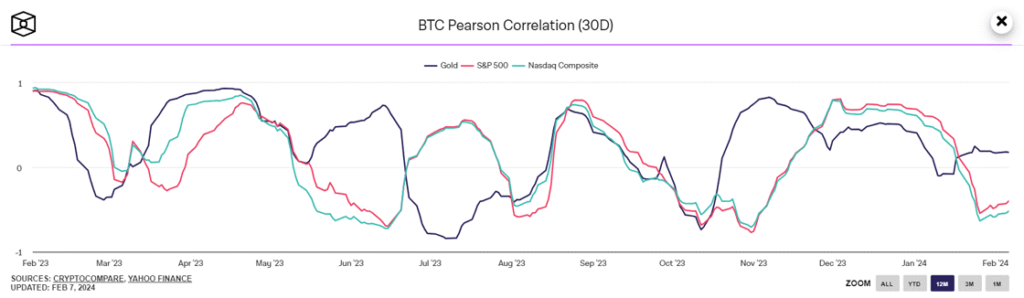

Additionally, the U.S. economy experienced significant growth in the last quarter, expanding by 3.3% compared to an estimated 2%. Further, strong earnings reports from major companies like Meta and Amazon also bolstered confidence, with growth estimates surpassing expectations at 7.8% versus 6.4%, leading the SP500 to hit an ATH. Despite these positive indicators highlighting the U.S. economy’s resilience relative to others, the data suggests limited prospects for a Fed interest rate cut in March. Chairman Jerome Powell echoed this, emphasizing that “it is probably not the most likely case or the base case” for a March cut. Given Bitcoin’s recent mild recovery in correlation with the S&P 500 and Nasdaq, shown below in Figure 1, it’s imperative to monitor economic indicators closely to gauge the potential spillover effects on the emerging asset. It’s also equally important to assess when the FED will cut interest rates as it’ll impact risk-on asset classes such as crypto since Quantitative Easing (QE) policies inject more capital and liquidity into the market while increasing investors’ risk appetite.

Figure 1: Bitcoin’s Correlation with Nasdaq and S&P 500

Source: TheBlock

Liquidations Anticipated as Part of Bankruptcy Proceedings of FTX and Genesis

After months of uncertainty, FTX will not relaunch its collapsed exchange and plans to pay its customers in total, which will be based on the prices of November 2022, when Bitcoin was priced at less than $17K as a consequence of the bankruptcy dollarization process. So far, FTX has recovered at least $7 billion in assets, which they are planning to liquidate to make their customers whole, which could take a toll on the market, similar to when FTX sold GBTC shares shortly following the approval of the spot Bitcoin exchange-traded funds (ETFs) in the U.S.

Additionally, Genesis is seeking court approval to sell $1.6 billion of its Grayscale Trust assets following a $21 million settlement agreement with the Securities and Exchange Commission (SEC). Users of FTX and Genesis form the two most significant headwinds along Mt. Gox creditors. Thus, It’s essential to realize any source of external selling pressure that could impact the market.

Funds Marked Safe Amid Solana’s Outage

After a year of stability, Solana experienced an outage lasting five hours on February 6 at 09:53 UTC. While over $3B in assets under management were reported safe, the outage only resulted in failed transactions. To resolve the issue that caused the network to halt, engineers from various ecosystem sectors collaborated to release a new validator software containing a critical patch. Validator operators were promptly instructed to upgrade their systems to initiate the network restart. By 14:57 UTC, Solana mainnet beta resumed block production following a successful upgrade to version 1.17.20 and a cluster restart managed by validator operators. Solana assured stakeholders that its engineering team is closely monitoring the network’s performance during the restoration process. Additionally, a post-mortem report investigating the root cause of the outage is currently in progress and will be shared on Solana’s communication channels once finalized.

This Week’s Calendar

Source: 21Shares, Forex Factory

Research Newsletter

Each week the 21Shares Research team will publish our data-driven insights into the crypto asset world through this newsletter. Please direct any comments, questions, and words of feedback to research@21shares.com

Disclaimer

The information provided does not constitute a prospectus or other offering material and does not contain or constitute an offer to sell or a solicitation of any offer to buy securities in any jurisdiction. Some of the information published herein may contain forward-looking statements. Readers are cautioned that any such forward-looking statements are not guarantees of future performance and involve risks and uncertainties and that actual results may differ materially from those in the forward-looking statements as a result of various factors. The information contained herein may not be considered as economic, legal, tax or other advice and users are cautioned to base investment decisions or other decisions solely on the content hereof.

Vilken typ av sektor ETFer finns det?

LVLD ETF investerar i ett urval av företag världen över med låg volatilitet

Den europeiska ETF-revolutionen: Skiftet som ritar om kartan för kapitalförvaltning

EEAK ETF investerar i eurodenominerade statsobligationer från eurozonen

HEQQ ETF mål är att ge långsiktig kapitaltillväxt

USA satsar 2 miljarder dollar på kvantdatorer – så kan investerare dra nytta av utvecklingen

Extrema skillnader: Varför presterar Europas kvantdator-ETFer så olika?

QQCC ETF följer företag världen över som är aktiva inom kvantberäkning

Fastställd utdelning i MONTDIV maj 2026

Varför Plus500 är en dröm för finans-affiliate

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanUSA satsar 2 miljarder dollar på kvantdatorer – så kan investerare dra nytta av utvecklingen

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanExtrema skillnader: Varför presterar Europas kvantdator-ETFer så olika?

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanQQCC ETF följer företag världen över som är aktiva inom kvantberäkning

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanFastställd utdelning i MONTDIV maj 2026

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanVarför Plus500 är en dröm för finans-affiliate

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanETFer för fotbolls-VM 2026

-

Nyheter1 vecka sedan

Nyheter1 vecka sedanDen osynliga flaskhalsen i AI-boomen: Varför elinfrastruktur är nästa stora megatrend

-

Nyheter4 veckor sedan

Nyheter4 veckor sedan21shares produkter nu finns tillgängliga hos Revolut