Nyheter

Transforming DeFi: The Strategic Leap of Unichain

• Uniswap Labs announced Unichain, whose testnet launched on October 10 and mainnet is launching in November, relying on the tech infrastructure from Ethereum layer-2 Optimism’s OP Stack, and block builder Flashbots.

• Unichain is a DeFi-specific scalability solution aiming to offer a universal liquidity hub, with an emphasis on transaction speed and superior security.

• Uniswap’s token UNI will be used, or staked, to validate Unichain transactions and earn part of the network’s sequencer fees – of which the stack will be decentralized using what’s known as the Unichain Validation Network.

• This is a key development, as it will transform UNI from a governance token into a utility token, thereby completely changing its investment case.

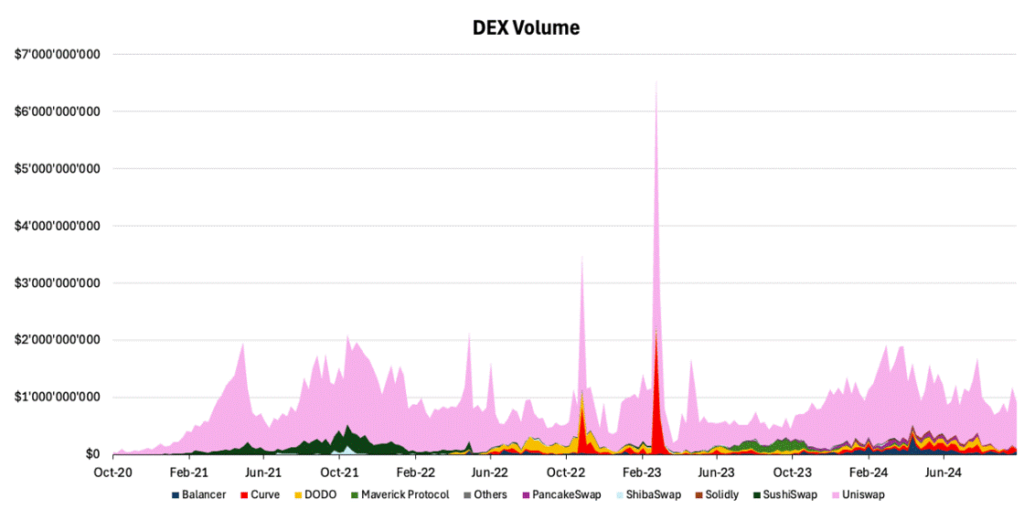

Uniswap is the crypto market’s largest decentralized exchange (DEX) and the pioneer of the crypto-native automated market maker (AMM), which later became an industry standard for most DEXs. While Uniswap has maintained over 46% of the market share, its dominance has been eaten away by emerging DEXs, as shown below in Figure 1, that offer revenue sharing with token holders rather than just for liquidity providers.

Figure 1 – Decentralized Exchanges Volume

Source: Dune

Driven by this increasing competition, Uniswap Labs revealed Unichain, a Layer 2 (L2) Superchain, built using OP Stack, which is a modular, open-source software stack developed by Optimism, one of Ethereum’s leading scalability solutions. The primary goal of the OP Stack is to create scalable, secure, and interoperable blockchains, with Unichain being a prime example.

What is Unichain?

In essence, it’s a DeFi-centric Ethereum scaling solution designed to cater to users’ financial activities. By integrating advanced cross-chain functionality through technologies like cross-chain intents (ERC-7683), which we’ll delve into later, and the LayerZero bridge, Unichain addresses key challenges in the DeFi ecosystem:

- Transaction Speed: Block times are reduced to one second, with plans for 250ms sub-blocks – faster than many other L2s.

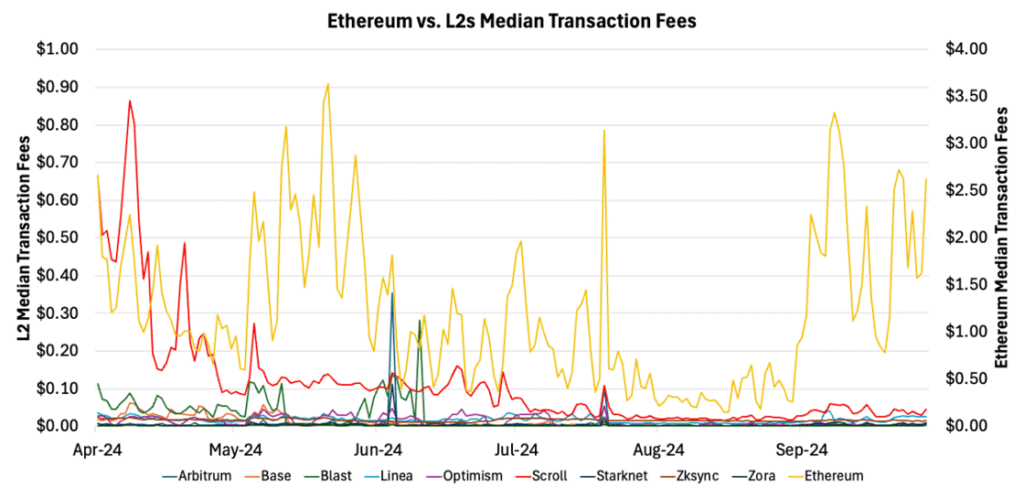

- Cost Efficiency: Transaction costs are projected to decrease by approximately 95% compared to Ethereum’s Layer 1, as can be observed below in Figure 2.

- Cross-Chain Liquidity: Unichain aims to create a unified ecosystem for seamless multi-chain asset trading, all whilst abstracting the technology’s complexity away from the user. Otherwise, users are required to utilize third-party bridging solutions and asset wrappers, which exposes them to heightened smart-contract risk.

- Incentive Structure: A robust reward system that compensates both token holders and liquidity providers for their liquidity and security contributions.

While Unichain aims to tackle liquidity fragmentation across networks, this gradual process will stretch beyond the initial mainnet launch. The protocol will need to incentivize users and liquidity providers to migrate their liquidity to Unichain as the premier network over time. Thus, liquidity fragmentation could worsen in the short term as this reorganization takes place.

Figure 2 – Average transaction speed vs. Fees of Ethereum’s Layer 2s

Source: Dune

What makes Unichain stand out?

- Interoperable and a Multi-Chain Cohesive Ecosystem:

The quest of lowering transaction costs came at the expense of fragmented liquidity, complicating the user experience. Unichain is designed to simplify swapping across different chains. They worked with OP Labs, the builders behind Optimism (Ethereum’s third largest L2 by TVL of $680M), to make it easy to send messages between L2s in the Optimism Superchain using the network’s stack native interoperability technology. For other chains, Uniswap Labs is improving cross-chain compatibility through initiatives like the Cross-Chain Intents standard, known as ERC-7683.

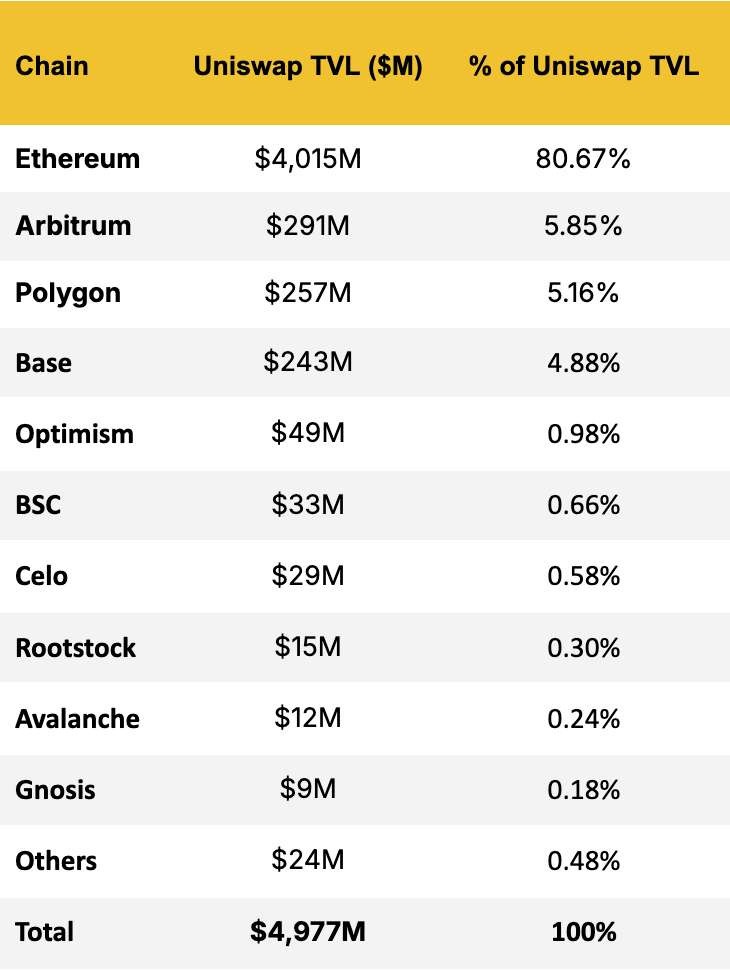

In this view, Unichain’s Total Addressable Market can have a target of $4.9B, illustrated below in Figure 3.

Figure 3 – UNI’s TVL Across Chains

Source: DeFiLlama

What is ERC-7683, and what is its impact?

Introduced in April 2024, the Cross-Chain Intents standard enhances blockchain interoperability by standardizing off-chain messages and on-chain settlement. This framework simplifies cross-network transactions for users, allowing them to submit a general request—such as swapping Token X on Ethereum for Token Y on Arbitrum—without needing to choose specific bridges, DEXs or solutions. Once a request is made, specialized agents called ”fillers” compete to execute the transaction efficiently. This approach streamlines the process, making it easier for users to trade across several networks like they would in a traditional fintech application that has multiple currency accounts, all whilst fostering competition among service providers across the crypto ecosystem. This will ultimately improve the user experience, which is one of the most important factors in driving mainstream adoption.

- Vertical Integration:

Unichain represents a strategic shift in Uniswap’s operational model, enhancing its control over revenue streams and transaction processing. By evolving into an execution network similar to Base and Arbitrum, Unichain now captures additional value through:

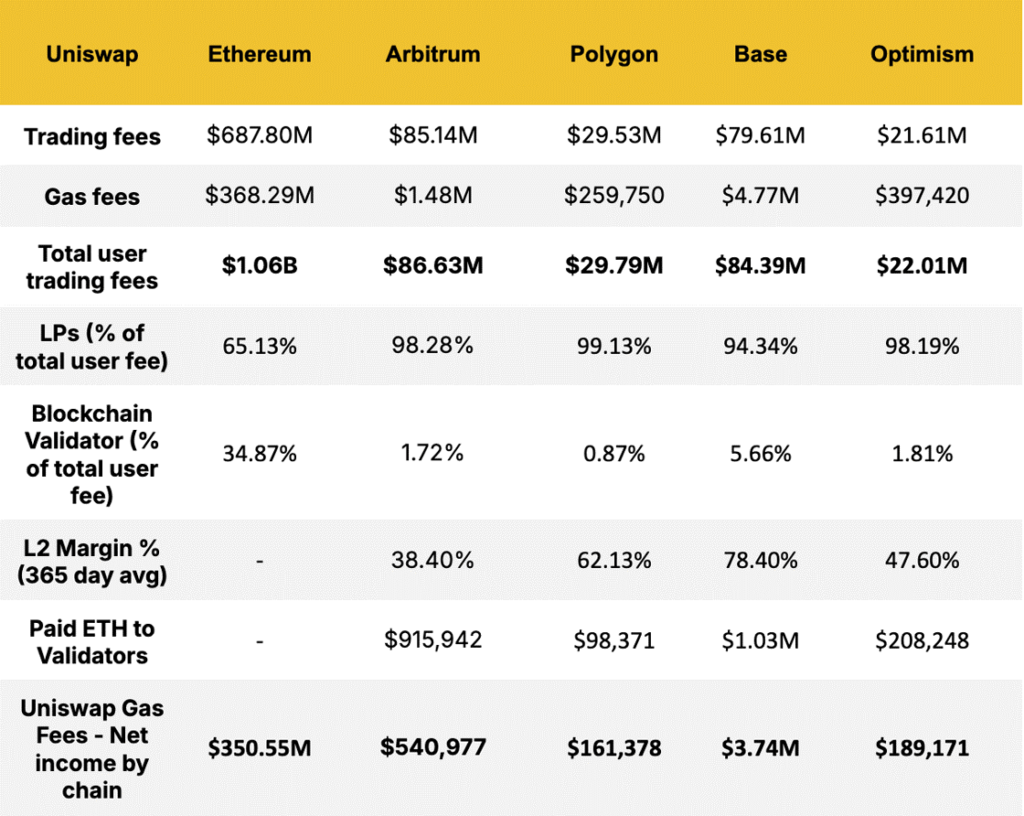

o Transaction / Gas Fees – previously allocated to the networks Uniswap lives on. As shown below in Figure 4, Uniswap will be able to preserve about close to $374M in fees, once they’re able to settle these transitions on its own network.

Figure 4 – Uniswap Economics by Blockchain

Source: TheDeFiReport, TokenTerminal

o Swap fees: allocated to liquidity providers (LPs), which had previously been managed and distributed to contributors.

o Front-end fees: the protocol’s only source of revenue that it retains. It has already been in place and managed by the exchange’s front-end interface, as shown below in Figure 5. Uniswap has generated close to $50M in front-end fees since inception.

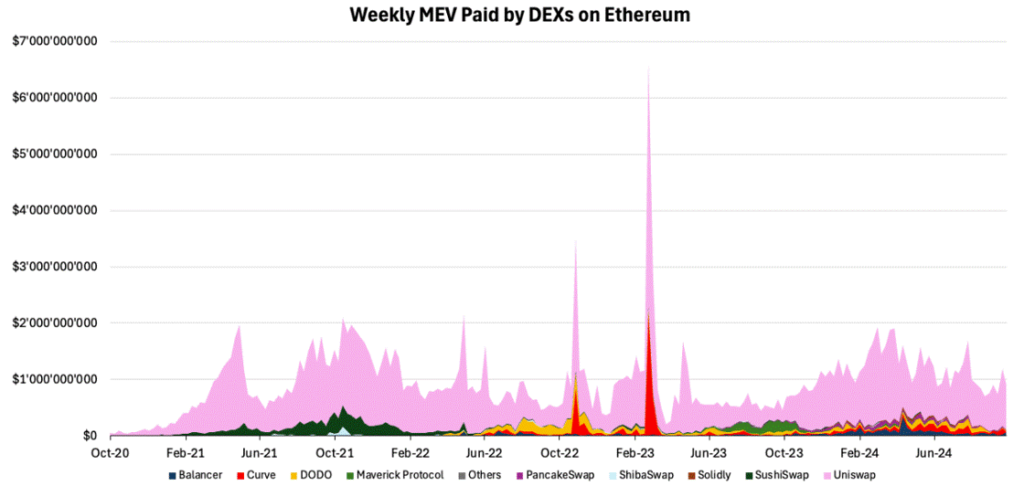

o Maximal Extractable Value (MEV): previously absorbed by the networks Uniswap was deployed on. Unichain could retain a significant portion of the $83B paid on Ethereum if they had internalized MEV from the offset, as seen below in Figure 5.

Figure 5 – Total Volume of Sandwich attacks on Ethereum, via Uniswap

Source: Dune

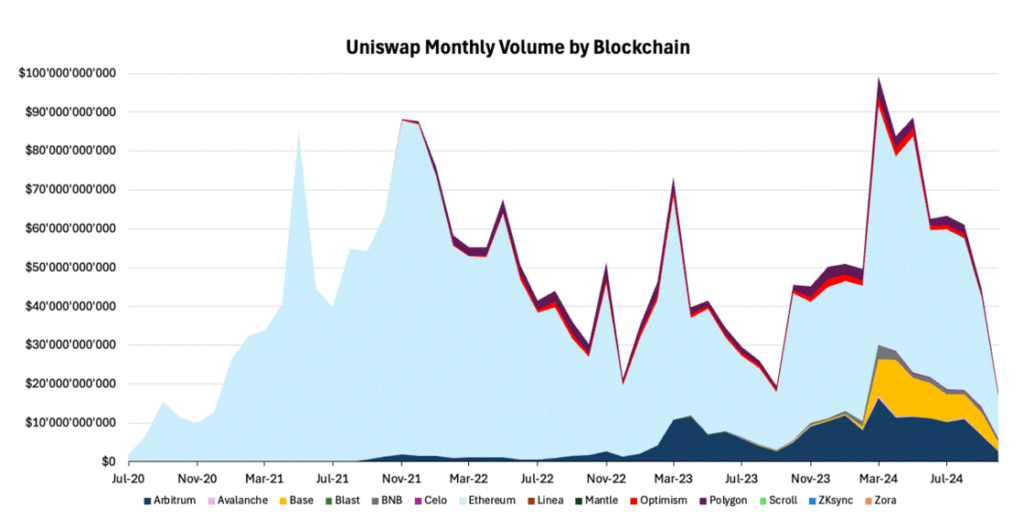

This transformation allows Uniswap to optimize its revenue structure and maintain greater oversight of the entire transaction lifecycle, from execution to settlement. The new model not only improves Uniswap’s economic efficiency but also positions it to offer enhanced services and potentially lower costs for users, all while retaining more value within its ecosystem. Uniswap’s substantial DEX volume across multiple networks, as illustrated in Figure 6, positions the new network for significant growth. By consolidating this activity within its ecosystem, Unichain stands to benefit from a powerful network effects.

Figure 6 – Uniswap Volume Across Different Chains

Source: Dune

Unichain’s architecture also enhances the platform’s capabilities with features like fair transaction ordering, which helps prevent market manipulation strategies such as front-running and back-running. Additionally, by utilizing a dedicated validator set on Ethereum, Unichain can effectively mitigate toxic flows, thereby reducing Maximal Extractable Value (MEV) losses, which we talk about next, helping to foster a fairer trading environment.

- Lower MEV Loss: Unichain’s collaboration with Flashbots introduces an advanced block production system that enhances market efficiency and mitigates MEV concerns. By utilizing Trusted Execution Environments (TEEs), this system achieves faster block times, improved transaction ordering transparency, and reduced failed transactions. While TEEs do not replace decentralized consensus, they provide enhanced trust and security compared to traditional block builders. This approach effectively limits validators’ ability to manipulate transaction order for profit, creating a more equitable environment.

- Unichain Validation Network: UNI stakers will form a decentralized network of full nodes that replace the actions of the centralized sequencer. Overall, they will provide several key benefits, including:

o Enhanced Decentralization: An additional layer of security that allows independent nodes of operators (token stakers) to verify the state of the blockchain – helping to reduce the risks associated with single sequencer architecture commonly found in other L2 solutions.

o Faster Finality: Quicker settlement of cross-chain transactions, driven by the flashblock technology.

o Increased Token Utility: Instead of simply serving as a governance token, UNI will now play a critical part in the ecosystem. Validators will have to stake the token to participate in the network validation – allowing token holders and not just liquidity providers to earn rewards.

So, what does that mean for Uniswap, Ethereum and the other L2s Uniswap was deployed on?

Unichain’s launch will introduce seamless cross-chain swaps directly through the Uniswap Interface and Wallet, significantly enhancing accessibility to cross-chain markets and their liquidity.

The platform will utilize UNI tokens for network security, with staking occurring on the Ethereum mainnet. This integration increases UNI’s utility and potential demand. However, it’s important to note that the staking yield from transaction fees is distinct from the pending fee switch affecting the broader Uniswap community. Both mechanisms serve to incentivize token holders.

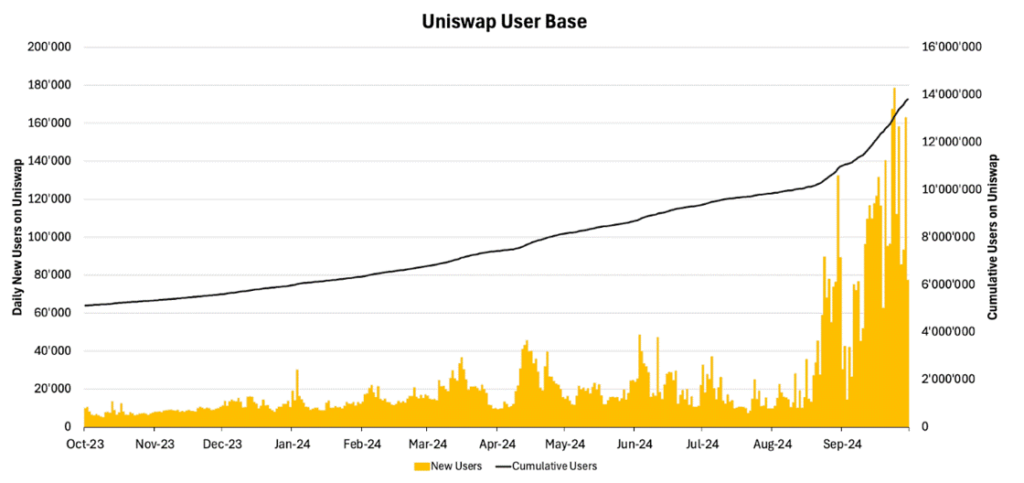

Unichain’s introduction may signal a shift towards app-specific chains retaining substantial user activity. This could create a network effect, attracting more users and liquidity and potentially drawing in other DeFi protocols focused on multi-network presence rather than developing proprietary chains. As seen below, Uniswap has about 14M cumulative users spread across the multiple networks it is deployed on, depicted below in Figure 7. Thus, consolidating this user base could create an unmatched DeFi hub.

Figure 7 – Uniswap Users and New Users

Source: Dune

For Ethereum, Unichain’s launch may lead to a reduction in revenue, as Uniswap has been a significant contributor to transaction fees on the mainnet. Consequently, this could further decrease Ethereum’s deflationary activity. However, if an explosion of activity occurs, we can expect a surge in the amount of ETH used by L2s to settle their activity on the mainnet.

To recap, Uniswap’s evolution into Unichain represents a pivotal shift for the UNI token, transforming it from a governance-focused asset into a multifaceted, value-generating instrument. This transition elevates UNI’s status in the crypto ecosystem, positioning it competitively alongside established proof-of-stake tokens like ETH.

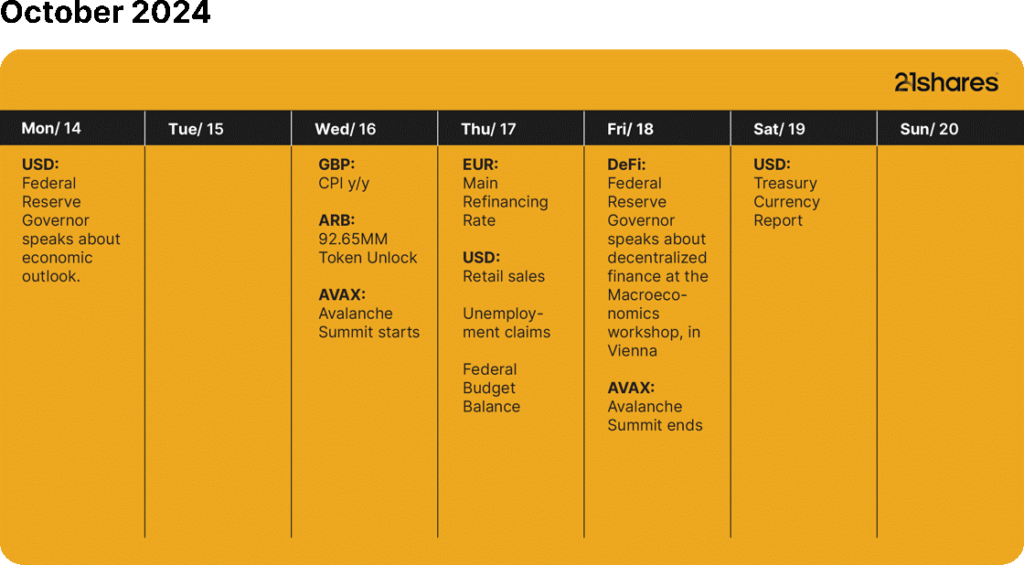

What’s happening this week?

Source: Forex Factory, 21Shares

Research Newsletter

Each week the 21Shares Research team will publish our data-driven insights into the crypto asset world through this newsletter. Please direct any comments, questions, and words of feedback to research@21shares.com

Disclaimer

The information provided does not constitute a prospectus or other offering material and does not contain or constitute an offer to sell or a solicitation of any offer to buy securities in any jurisdiction. Some of the information published herein may contain forward-looking statements. Readers are cautioned that any such forward-looking statements are not guarantees of future performance and involve risks and uncertainties and that actual results may differ materially from those in the forward-looking statements as a result of various factors. The information contained herein may not be considered as economic, legal, tax or other advice and users are cautioned to base investment decisions or other decisions solely on the content hereof.

JRWE ETF en globalfond valutasäkrad i Euro

Single-stock options income ETPer finns nu tillgängliga i Nederländerna för första gången

QQQY ETP dagliga optioner på indexet och månadsvis utdelning

Is Mobile Powering the Future of Gaming?

Fyra nya börshandlade fonder från JP Morgan

HANetf och Infrastructure Capital Advisors samarbetar för att lansera aktivt förvaltad preferensavkastnings-ETF i Europa

De bästa lågvolatilitets ETFer på marknaden

Fokus mot en helt ny börshandlad produkt i september 2025

HANetf kommenterar kopparuppgången

Börshandlade fonder för europeiska small caps

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanHANetf och Infrastructure Capital Advisors samarbetar för att lansera aktivt förvaltad preferensavkastnings-ETF i Europa

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanDe bästa lågvolatilitets ETFer på marknaden

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanFokus mot en helt ny börshandlad produkt i september 2025

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanHANetf kommenterar kopparuppgången

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanBörshandlade fonder för europeiska small caps

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanM5TYs senaste utdelningstakt (55 %) belyser covered call-strategins inkomstpotential

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanCould Bitcoin be the key to your dream house?

-

Nyheter1 vecka sedan

Nyheter1 vecka sedanLevler noterar ytterligare fyra börshandlade fonder i Sverige