Nyheter

SEC’s Game-Changing Move: Spot Price Bitcoin ETF Approval Marks a New Era for Cryptocurrency Investments

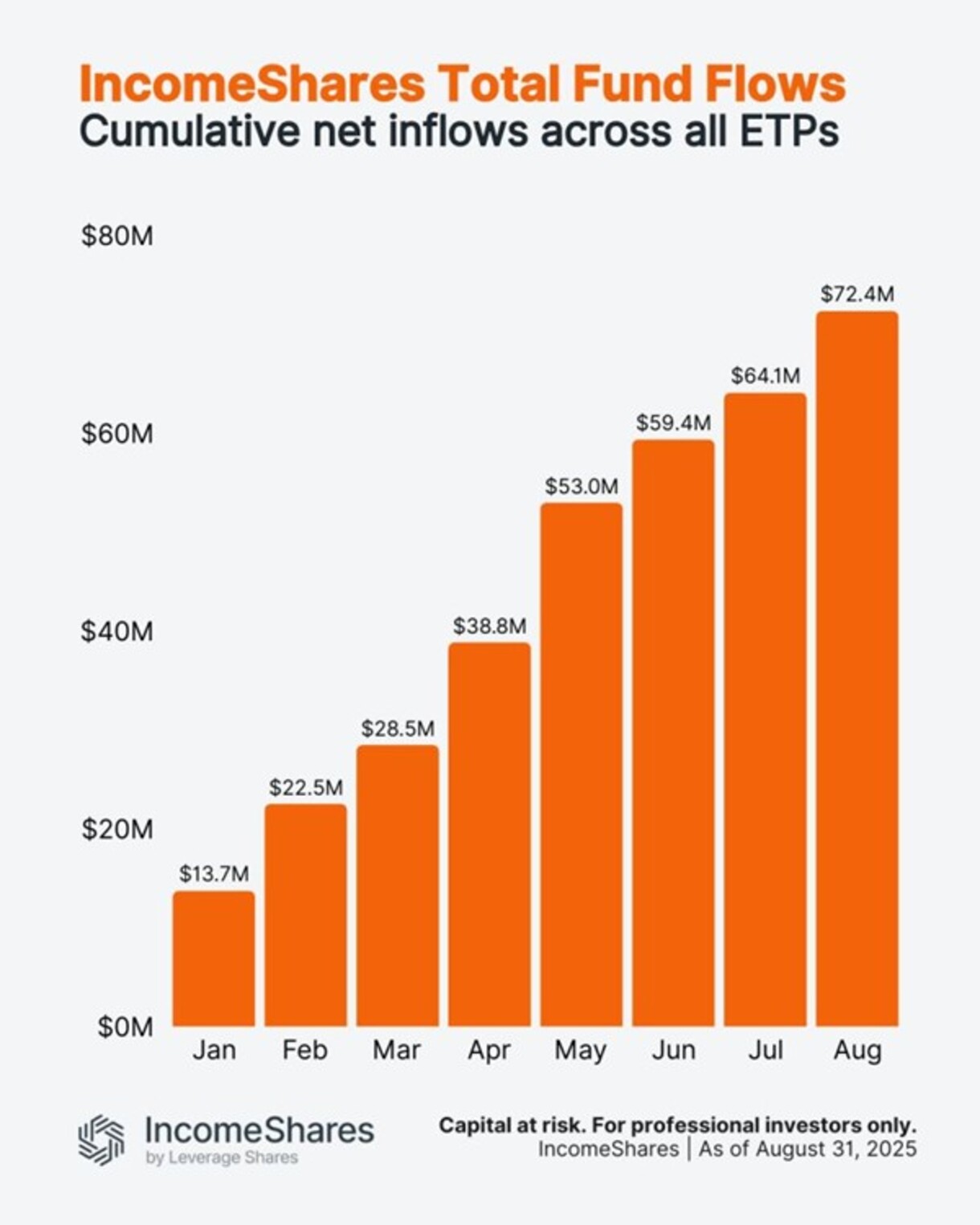

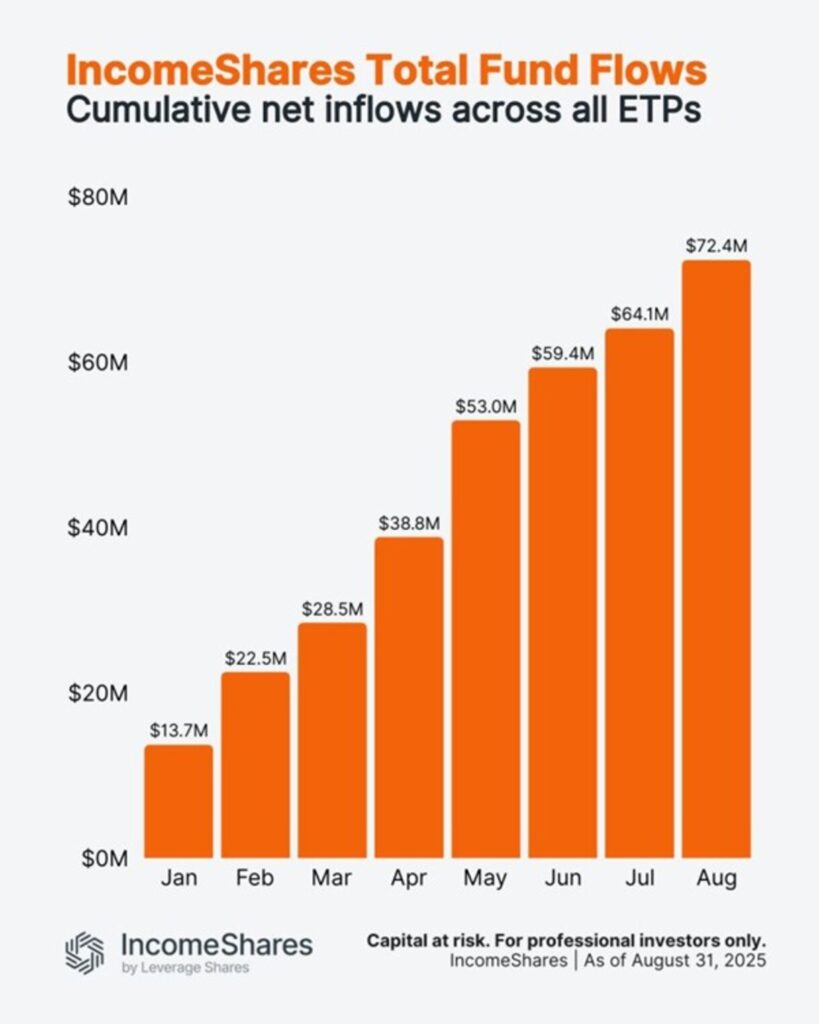

Fondflöden spårar hur mycket pengar investerare sätter in i eller tar ut från IncomeShares börshandlade produkter. Positiva fondflöden innebär att mer pengar kommer in än går ut – ett tecken på efterfrågan på börshandlade produkter.

Kumulativa fondflöden har ökat varje månad under 2025. I slutet av augusti nådde de 72,4 miljoner dollar. Det är över 8 miljoner dollar i nya pengar som tillkommit enbart i augusti – den största månatliga ökningen sedan maj.

Diagrammet nedan visar trenden.

Följ IncomeShares EU för fler uppdateringar.

XB28 ETF köper företagsobligationer med förfall 2028 och stänger sedan

IncomeShares fondflöden nådde en ny rekordnivå i augusti

JIGG ETF investerar i företagsobligationer från hela världen

JEQA ETF investerar i Nasdaq-100 i kombination med en derivatteknik

Bitwises Bradley Duke om marknadstrender och Bitcoin-utsikter

VALOUR ARB SEK spårar priset på kryptovalutan Arbitrum

Månadsutdelande ETFer uppdaterad med IncomeShares produkter

HANetfs analyserar hur ett fredsavtal kan påverka det europeiska försvaret

HANetfs VD kommenterar Trump-Putin-toppmötet

De bästa innovations-ETFerna

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanVALOUR ARB SEK spårar priset på kryptovalutan Arbitrum

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanMånadsutdelande ETFer uppdaterad med IncomeShares produkter

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanHANetfs analyserar hur ett fredsavtal kan påverka det europeiska försvaret

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanHANetfs VD kommenterar Trump-Putin-toppmötet

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanDe bästa innovations-ETFerna

-

Nyheter7 dagar sedan

Nyheter7 dagar sedanUtdelningar och försvarsfonder lockade i augusti

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanADLT ETF investerar bara i riktigt långa amerikanska statsobligationer

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanIncomeShares når 60 miljoner dollar i förvaltat kapital – Tillväxtöversikt 2025