Nyheter

Satoshi Unmasked? What’s At Stake?

Satoshi Nakamoto is the pseudonym used by the person or group who created Bitcoin and was active in the development of the blockchain until December 2010. Satoshi continues to live on in Bitcoin as units of BTC are called sats – short for Satosh, but their identity has been widely controversial. HBO’s documentary, Money Electric: The Bitcoin Mystery, premiering later today, is the most recent attempt at unmasking the Bitcoin creator. Although the identity of Satoshi will probably not be verified by this documentary, HBO’s production speaks volumes about Bitcoin’s mainstream prominence. It is a leap forward in the asset’s adoption trajectory.

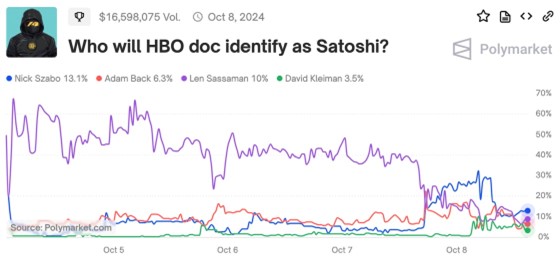

Figure 1 – Polymarket Bets on Who Will be Unmasked as Satoshi on the HBO Documentary

Source: Polymarket

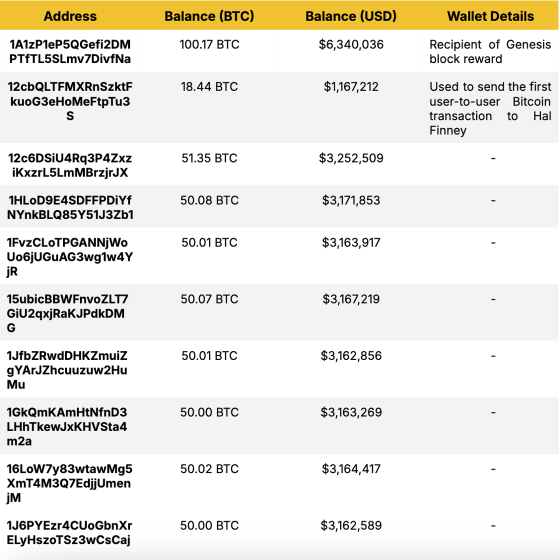

The fascination with uncovering Satoshi’s true identity has long captivated the crypto community. This curiosity isn’t solely about identifying the creator of Bitcoin; it’s also driven by the significant influence Satoshi could wield due to his reputed wealth. According to research from Sergio Demian Lerner, crypto entrepreneur and founder of BTC-based smart contract platform Rootstock, there are certain wallets exhibiting Satoshi-esque behavior, estimated to control around 1.1M BTC. Lerner’s report outlines a pattern of behavior across these wallets; they remain dormant, exhibit a 99% tendency not to spend their Bitcoin, and suddenly halted mining activities after Satoshi’s disappearance in 2011.

These so-called ’Patoshi’ wallets lend credibility to the theory that Satoshi’s holdings are distributed across multiple wallets. Although Lerner does not claim these wallets belong to Satoshi, their isolated behavior and long-standing inactivity make it plausible they could be tied to Bitcoin’s creator. Among these wallets, notable examples include one wallet that minted the Genesis Block, holding 100 BTC, and another associated with the historic first transaction to Hal Finney, as shown below:

Figure 2 – Possible Satoshi Wallets

Source: Blockchain.com

Regardless of who HBO’s documentary might hint at or identify as Satoshi, this isn’t the first time such claims have surfaced. Bitcoin has a history of similar unmasking attempts, which we’ll now explore in further detail.

Previous attempts to unmask Satoshi – who are the candidates?

The following people are said to have worked with Satoshi Nakamoto in some capacity. They were also part of the cypherpunk movement that started in the 1990s. This movement was a network of individuals interacting via mailing lists, advocating the widespread use of strong cryptography and privacy-enhancing technologies to effect social and political change.

• Wei Dai (2011): An early cryptographer whose work on b-money was referenced by Satoshi in the Bitcoin whitepaper. His influence and knowledge of cryptocurrencies made people think he was the creator of Bitcoin, which he has denied.

• Gavin Andresen (2011): A Bitcoin developer who took the lead after Satoshi stepped away. Andresen said that he worked closely with Satoshi without knowing their real identity. His commit access to Bitcoin Core was revoked in May 2016 when Craig Wright convinced him that he was behind Bitcoin, which Andresen later denied to the press, announcing his regret that he had ever trusted him.

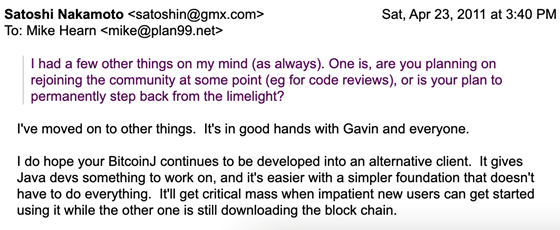

Figure 3 – Final (public) E-mail from Satoshi Nakamoto

Source: Mike Hearn

• Len Sassaman (2011): A cryptography expert who has worked with Finney on Pretty Good Privacy (PGP), a program used for signing, encrypting, and decrypting texts, e-mails, files, directories, and whole disk partitions and to increase the security of e-mail communications. Additionally, Len is known for his expertise in remailer technology, namely maintaining the code of Mixmaster. The remailer technology is debated as the foundation of Bitcoin and its intellectual history. Although his widow denied it, the suspicion grew when Len took his own life a few months after Satoshi’s final e-mail, shown in Figure 2.

• Nick Szabo (2013): The computer scientist and cryptographer behind Bit Gold, a precursor for Bitcoin, and the inventor of smart contracts. His previous work made him one of the prime suspects for being Satoshi, which Szabo has consistently denied.

• Hal Finney (2014): An early Bitcoin adopter, the first to receive a Bitcoin transaction from Nakamoto, and a key contributor to the Bitcoin network, making him one of the prime suspects. Finney was the creator behind the reusable Proof-of-Work, on which Bitcoin mining is based. He passed away in 2014 without publicly acknowledging that he was Satoshi.

Figure 4 – First Bitcoin Transaction from Nakamoto to Finney

Source: Blockchain.com

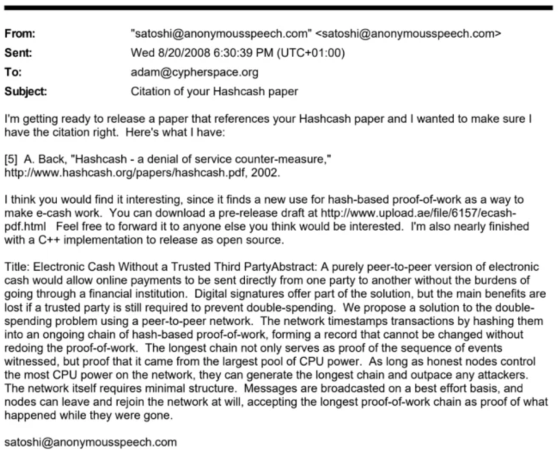

• Adam Back (2019): An early Bitcoin adopter and cryptographer who created the Hashcash proof-of-work system, which was also integral to Bitcoin mining, as shown in Figure 5 below. A documentary aired in 2019 suggested that Back could be Satoshi, which he later denied.

Figure 5 – E-mail Interaction Between Back and Satoshi

Source: Bitcoin Magazine

On the other hand, the following debunked suspects add some more to the story:

• Dorian Nakamoto (2014): born as Satoshi Nakamoto, is a Japanese-American who interestingly lived in the same town as Finney. He first surfaced in a Newsweek article in 2014 which featured claims that he later denied.

• Craig Wright (2015): A computer scientist and entrepreneur who publicly claimed to be Satoshi in 2016, a year after some publications suggested Wright might be Bitcoin’s creator, citing leaked e-mails and documents, which were later court-ruled as fabricated. Moreover, Wright failed to produce cryptographic proof that he had control of the Satoshi-labelled wallets.

Figure 6 – Craig Wright’s Forged Correspondence

Source: Hackernoon

• Paul Le Roux (2019): A notorious criminal mastermind and former programmer who created encryption software and ran a global criminal empire. The suspicion about him being Satoshi was instigated by his reference in the Craig Wright case and was later picked up by Wired in 2019. The primary reason for suspicion was his Encryption for the Masses (E4M), an open-source disk encryption platform. Additionally, Le Roux’s arrest in 2012 also grew suspicion as it coincided with Satoshi’s online disappearance.

Don’t Trust, Verify

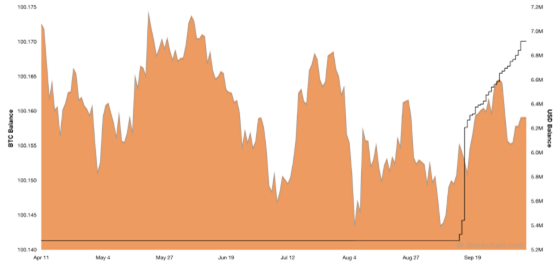

Over the years, claims that have surfaced about Satoshi’s identity haven’t stood up to scrutiny due to the crypto community’s ethos: Don’t trust, verify. Only cryptographic proof—such as signing a transaction from one of Satoshi’s known wallets—would be accepted as evidence. To date, no such action has ever occurred, with Satoshi’s wallets remaining dormant for nearly 14 years, as shown in Figure 7, by the Bitcoin Genesis Wallet. Until verifiable proof is presented, the community’s skepticism toward any new claims about Satoshi’s identity will persist.

Figure 7 – Bitcoin Genesis Wallet Holdings

Source: Blockchain.com

Interestingly, in January this year, a dormant wallet unexpectedly sent 26.9 BTC—worth nearly $2M —to the Genesis Wallet, raising intriguing possibilities. It could be interpreted as a gesture of burning the BTC or, alternatively, it might hint at the wake-up of Satoshi himself. The wallet’s origins point to the former, as most of the funds are traced back to a wallet labeled as belonging to Binance, according to Arkham Intelligence. Nevertheless, it does beg the question, what would happen should Satoshi awaken?

What if Satoshi wakes up or their wallets get hacked?

Discussions around Satoshi’s Bitcoin holdings often spark anxiety in the space, especially with estimates suggesting he holds around 1.1M BTC, valued at nearly $70B. While acknowledging the size of their holdings, it is merely an estimate and no evidence or proof points towards this. Furthermore, concerns that a sudden movement or potential hack would trigger major market disruption are largely overstated, thanks to several mitigating factors.

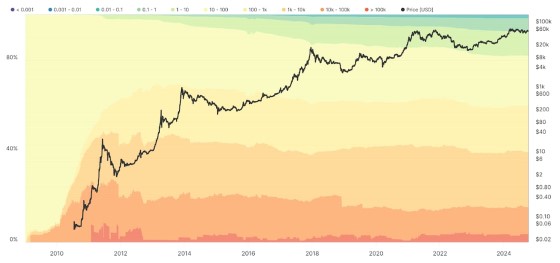

If we consider the upper estimate of Satoshi’s holdings at 1.1M BTC, this would account for approximately 5.2% of Bitcoin’s circulating supply. Glassnode’s on-chain data reveals that only 3.6% of the supply, less than 1M BTC, is currently held in wallets with over 100K BTC. Therefore, Satoshi distributed their holdings across multiple wallets, aligning with their mandate of maintaining privacy and security.

Figure 8 – Bitcoin Address Supply Distribution

Source: Glassnode

While a sudden sell-off of their holdings would have a substantial short-term impact on price, this scenario remains highly unlikely. Even if Satoshi coordinated sales from multiple wallets, Bitcoin’s deep liquidity should gradually absorb the shock. Additionally, the distributed nature of these holdings makes it extremely difficult for any potential hacker to compromise the funds, as breaching multiple wallets—many of which are offline and heavily protected—would be both challenging and time-consuming.

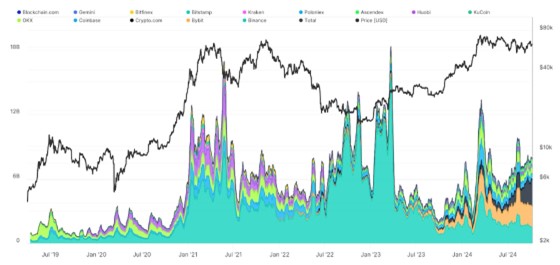

Further supporting this view is the significant liquidity available in Bitcoin markets today. According to Glassnode, daily trading activity across major exchanges regularly averages over $6B daily. Even if a portion of Satoshi’s BTC were to move, the sheer depth of Bitcoin’s liquidity ensures that such activity could be managed without causing market disruptions or extreme price fluctuations.

Figure 9 – Bitcoin’s Centralized Exchange Volume

Source: Glassnode

Further, only two Satoshi wallets are labeled and ever recorded activity, collectively holding just 120 BTC, or $7.6M. If this were sold today, it would not cause a significant impact, as they represent a negligible amount relative to Bitcoin’s daily exchange volumes. The most liquid exchanges could easily handle the sell-off without moving Bitcoin’s price by 2%, as shown below.

Figure 10 – Bitcoin’s Centralized Exchange % Depth

Source: Coingecko

While there are occasional murmurs about potentially banning early-day UTXOs (unspent transaction outputs) from being used—essentially proposing a fork to exclude these coins from the network—this idea hasn’t managed to gain traction. Such a move would fundamentally contradict Bitcoin’s core value proposition of being censorship-resistant. Furthermore, much of the Bitcoin community believes that Satoshi is entitled to their BTC, even if they choose to sell their holdings, given their foundational role in creating Bitcoin.

Bitcoin’s Value Proposition Remains Intact

Despite controversy regarding Satoshi’s identity, Bitcoin’s fundamental value proposition remains unchanged. Satoshi has not been heard from in almost 14 years and—to public knowledge—hasn’t signed any transactions since the earliest days of Bitcoin. It is highly unlikely that they would suddenly become active in a way that would disrupt the market. Bitcoin’s role as a hedge against currency debasement and a decentralized store of value remains firmly intact.

Whether or not someone emerges proving to be Satoshi or that HBO has cracked the code, Bitcoin’s core principles remain unaffected as a platform free from centralized control. Even if Satoshi were to reappear, he wouldn’t control Bitcoin’s codebase, relinquishing ownership once he disappeared. Bitcoin’s evolution is now driven by a global community, ensuring that no individual, not even its creator, can unilaterally alter its principles.

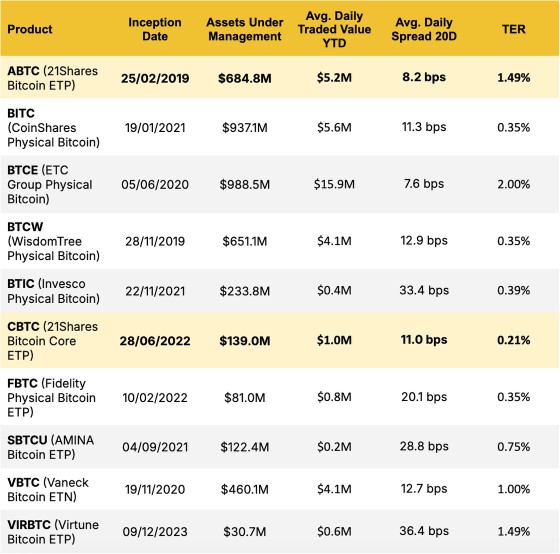

For investors looking to gain exposure to the pioneer cryptoasset and capitalize on the latest developments, 21Shares offers the following Bitcoin ETPs on the European market. These investment products provide a regulated way to capture Bitcoin’s growth potential as it solidifies its role as a digital store of value. With the increasing adoption of Bitcoin, these ETPs offer a strategic opportunity to participate in the ongoing evolution of the world’s leading cryptoasset.

Figure 11 – European Bitcoin ETPs Ordered by Ticker

Source: Bloomberg, Data as of October 7, 2024.

Avg. Daily Spread 20D: refers to the best daily average bid/ask spread over the last 20 days across European exchanges.

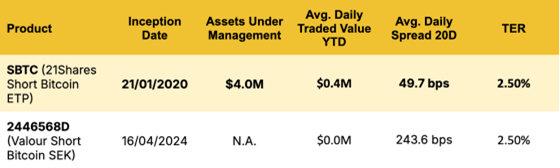

Figure 12 – European Short Bitcoin ETPs Ordered by Ticker

Source: Bloomberg, Data as of October 7, 2024.

Avg. Daily Spread 20D: refers to the best daily average bid/ask spread over the last 20 days across European exchanges.

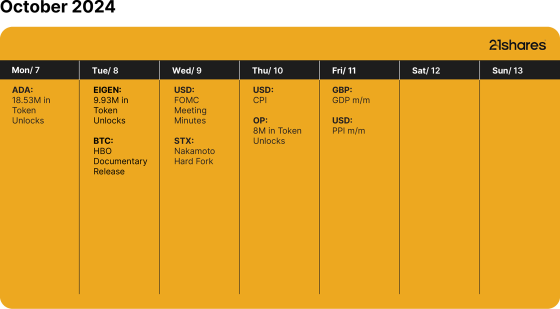

What’s happening this week?

Source: Forex Factory, 21Shares

Research Newsletter

Each week the 21Shares Research team will publish our data-driven insights into the crypto asset world through this newsletter. Please direct any comments, questions, and words of feedback to research@21shares.com

Disclaimer

The information provided does not constitute a prospectus or other offering material and does not contain or constitute an offer to sell or a solicitation of any offer to buy securities in any jurisdiction. Some of the information published herein may contain forward-looking statements. Readers are cautioned that any such forward-looking statements are not guarantees of future performance and involve risks and uncertainties and that actual results may differ materially from those in the forward-looking statements as a result of various factors. The information contained herein may not be considered as economic, legal, tax or other advice and users are cautioned to base investment decisions or other decisions solely on the content hereof.

Nyheter

BlackRock lanserar ST4R ETF för att erbjuda snabb tillgång till möjligheter inom rymdekonomin

Nya ETF- och ETP-noteringar den 9 juni 2026 på Deutsche Börse

UONS ETF spårar den amerikanska dagslåneräntan

BlackRock lanserar ST4R ETF för att erbjuda snabb tillgång till möjligheter inom rymdekonomin

DJIW ETF investerar i Sharia-kompatibla globala företag utanför USA

Nya ETF- och ETP-noteringar den 8 juni 2026 på Deutsche Börse

USA satsar 2 miljarder dollar på kvantdatorer – så kan investerare dra nytta av utvecklingen

De bästa ETFerna för att investera i emerging markets

Fastställd utdelning i MONTDIV maj 2026

Varför Plus500 är en dröm för finans-affiliate

Extrema skillnader: Varför presterar Europas kvantdator-ETFer så olika?

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanUSA satsar 2 miljarder dollar på kvantdatorer – så kan investerare dra nytta av utvecklingen

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanDe bästa ETFerna för att investera i emerging markets

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanFastställd utdelning i MONTDIV maj 2026

-

Nyheter1 vecka sedan

Nyheter1 vecka sedanVarför Plus500 är en dröm för finans-affiliate

-

Nyheter1 vecka sedan

Nyheter1 vecka sedanExtrema skillnader: Varför presterar Europas kvantdator-ETFer så olika?

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanASWF ETF är en aktivt förvaltad fond som investerar i Kanada

-

Nyheter2 veckor sedan

Nyheter2 veckor sedan21shares produkter nu finns tillgängliga hos Revolut

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanOlja och Hormuzsundet fick flest sökningar i maj 2026