Nyheter

Is dovishness dead at the Fed?

{kind=link}

Nyheter6 timmar sedan

GTIS ETF satsar på small caps med fokus på grön teknologi

Nyheter7 timmar sedan

Amundi lanserar globalfond med hävstång

Nyheter8 timmar sedan

CEME ETF investerar på den japanska aktiemarknaden

Nyheter1 dag sedan

Bitwises Bradley Duke om Bitcoin och guld på nya rekordnivåer

Nyheter1 dag sedan

JSDE ETF investerar i företag från Europa som tar hänsyn till EUs direktiv om klimatskydd

Nyheter3 veckor sedan

HANetf och Infrastructure Capital Advisors samarbetar för att lansera aktivt förvaltad preferensavkastnings-ETF i Europa

Nyheter3 veckor sedan

IN0A ETF spårar S&P 500 med fokus på företag med höga ESG-betyg

Nyheter4 veckor sedan

Vägen tillbaka till rekordnivåer är kantad av Fibonacci-motståndsnivåer

Nyheter4 veckor sedan

YSLV ETP ställer ut köpoptioner på silver för att skapa en löpande avkastning

Nyheter4 veckor sedan

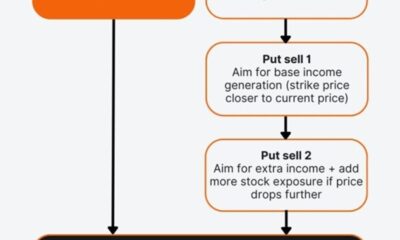

Så här fungerar strategin med kontantsäkerhet och aktier

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanHANetf och Infrastructure Capital Advisors samarbetar för att lansera aktivt förvaltad preferensavkastnings-ETF i Europa

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanIN0A ETF spårar S&P 500 med fokus på företag med höga ESG-betyg

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanVägen tillbaka till rekordnivåer är kantad av Fibonacci-motståndsnivåer

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanYSLV ETP ställer ut köpoptioner på silver för att skapa en löpande avkastning

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanSå här fungerar strategin med kontantsäkerhet och aktier

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanDe bästa lågvolatilitets ETFer på marknaden

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanPLTY ETP utfärdar optioner mot aktier i Palantir

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanTime in Bitcoin beats timing Bitcoin