Nyheter

Detrimental Allegations and a Regulatory Win: What Happened in Crypto This Week?

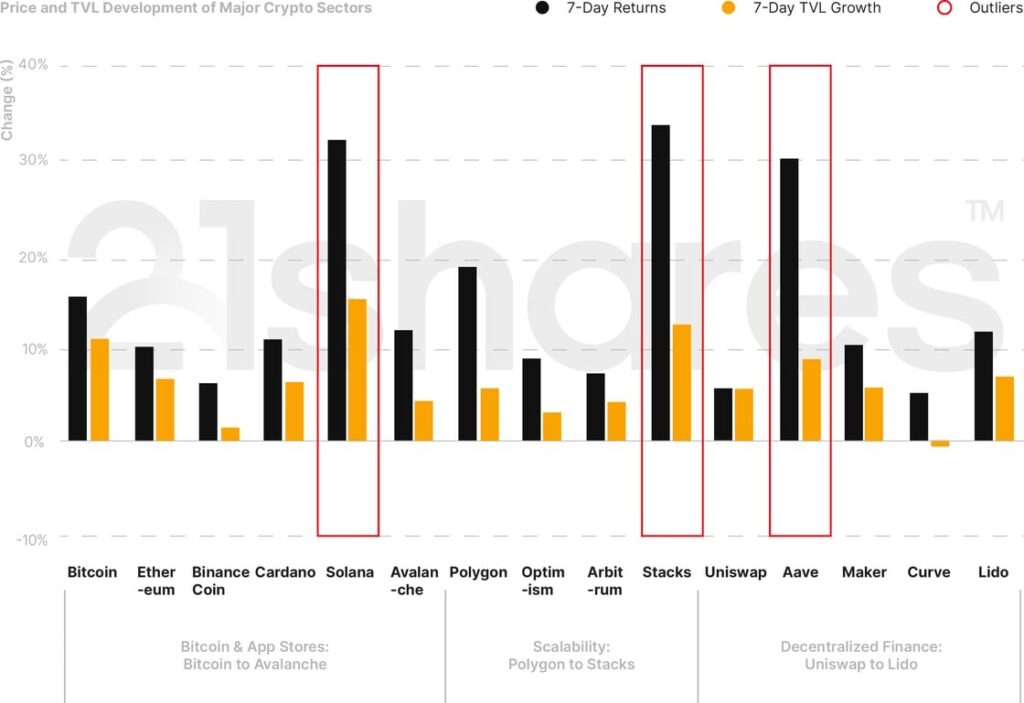

The U.S. government ran a $2.02 trillion deficit for the fiscal year through September, almost double last year’s. The Nasdaq Composite and S&P 500 are down by almost 3% over the past week. On the other hand, the top 15 cryptoassets by market cap have performed positively from last week. Bitcoin and Ethereum increased by nearly 16% and 10% over the past week, respectively. The biggest positive outliers of this week were Stacks, surging by 34%, Solana by 32.36%, and Aave, 30.37%.

Figure 1: Weekly Price and TVL Developments of Cryptoassets in Major Sectors

Source: 21Shares, CoinGecko, DeFi Llama. Close data as of October 23, 2023.

6 Things to Remember in Markets this Week

• Higher Yields Leave U.S. Banks with Massive Unrealized Losses

Bank of America’s unrealized losses on securities rose to $131.6B after the 10-year U.S. Treasury yield reached 4.93%, a figure not seen since 2007, before the Global Financial Crisis. Higher yields force bond prices to fall, ultimately leading to massive unrealized losses for prominent financial institutions betting on the bond market. On Thursday, Fed Chair Jerome Powell said that soaring bond yields could help the Fed slow the economy, further cooling inflation and possibly leading to the end of rate hikes. In this regard, a peak in real rates would be positive for risk assets. Many investors consider U.S. Treasuries the best proxy of a “risk-free” rate and thus view them as an opportunity cost – lower expected yields lead to lower discount rates, which result in a higher value for risky assets like stocks and crypto.

Figure 2: 10Y U.S Treasury Yield (2007-2023)

Source: St. Louis Fed

• Detrimental Allegations Against Gemini, Genesis, DCG, and Two Executives

New York Attorney General Letitia James filed a complaint against Gemini Trust and Genesis Capital, who both operated the troubled Gemini Earn product, on which the charges are based. The complaint is also against Digital Currency Group (DCG), owner and operator of Genesis, along with the latter’s CEO, Michael Moro, and DCG’s CEO, Barry Silbert, who are all facing criminal charges. The criminal charges include defrauding Gemini Earn investors, concealing a billion dollars in losses, and allegedly lying about their then-deteriorating financial condition. The key takeaway from the complaint was that Gemini lied to its Earn investors while allegedly siphoning millions of dollars taken from investor assets and handing them over to Genesis Capital, even after Earn was suspended. On June 13, 2022, one of Genesis’ largest borrowers, Three Arrows Capital, defaulted on billions of dollars in loans. The resulting losses created a “structural hole” at Genesis Capital that impaired its ability to repay its open-term liabilities—including to Earn investors.

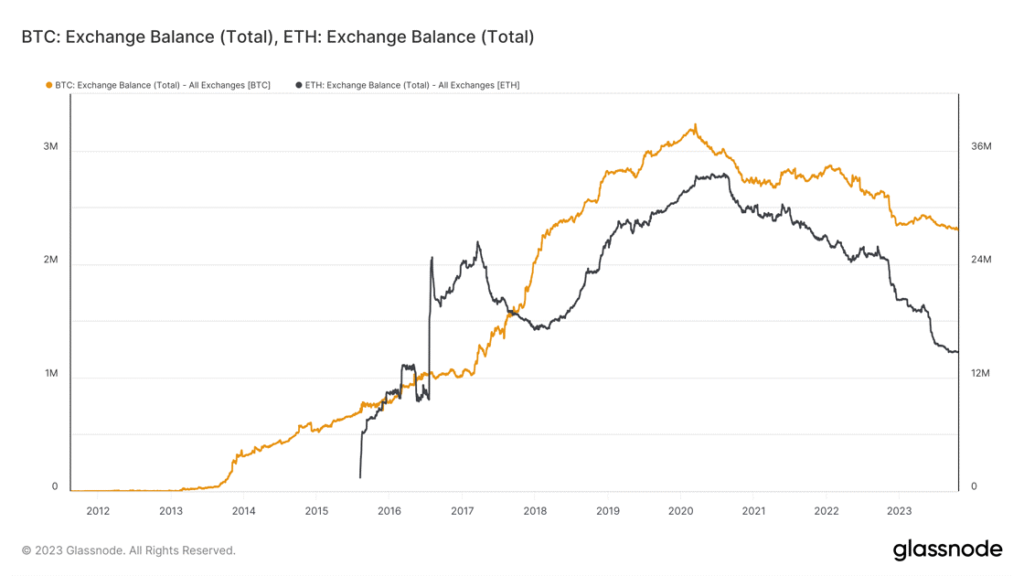

The complaint documented social media threads, later in June and September 2022, that falsely described the financial condition of Genesis Capital, which filed for bankruptcy last January. For its part, DCG told the Block that they intend to fight the claims against Silbert and its employees. The allegations in this lawsuit can further discourage users from leaving their assets on centralized exchanges or not engaging with them altogether. As shown in the figure below, Bitcoin and Ethereum’s balance on centralized exchanges is in steady and sharp decline, respectively.

Figure 3: Bitcoin and Ethereum’s Balance on Exchanges

Source: Glassnode

• New Win for Ripple Boosts XRP Returns

The Securities and Exchanges Commission (SEC) dropped lawsuits against two executives at Ripple Labs, claiming that Chief Executive Brad Garlinghouse and co-founder Chris Larsen aided and abetted sales of Ripple’s native token XRP which a judge had found amounted to unregistered sales of securities only in the case of institutional sales. However, the programmatic sales of XRP, those sold on exchanges and distributed to employees, did not constitute a securities offering, in the judge’s opinion. XRP was up by 7.6% in the 24 hours following the news and 10% over the past week. The SEC and Ripple Labs have until November 9, as requested by the former, to reach a resolution regarding the institutional sales of the token.

• Stablecoins on Bitcoin

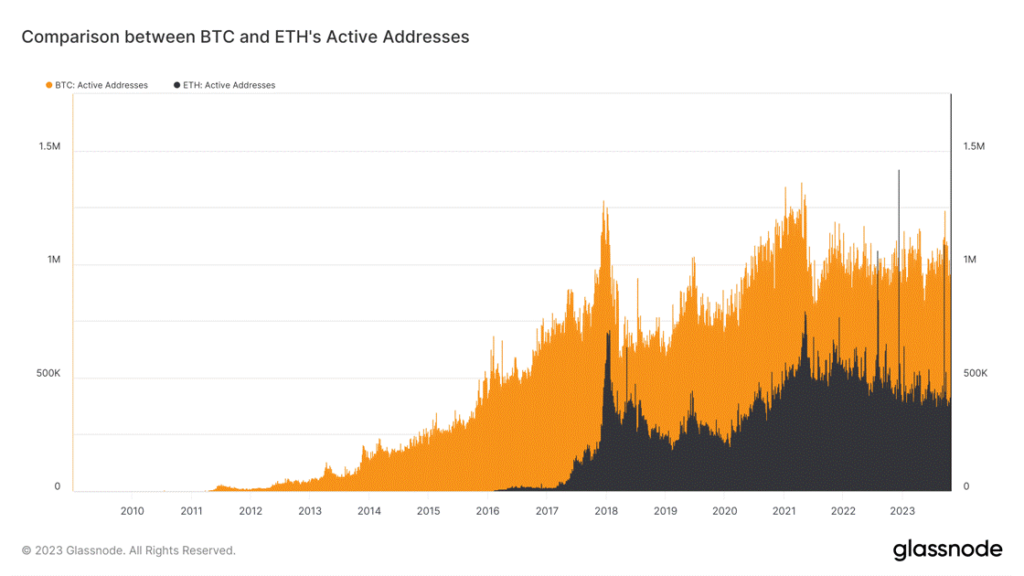

Lightning Labs is bringing stablecoins and real-world assets (RWA) to Bitcoin via Taproot Assets upgrade, aiming to make Bitcoin “the global routing network for the internet of money.” With this release, developers can issue financial assets on-chain in a scalable manner, providing a feature-complete developer experience for issuing, managing, and exploring stablecoins or other assets on the Bitcoin blockchain. With this upgrade, Bitcoin would be competing with Ethereum, the largest settlement layer for stablecoins. Over 56% of the $124B stablecoin market value is built on Ethereum and its compatible scaling solutions. However, with its first-mover advantage, Bitcoin has had historically more active users on the network in comparison to Ethereum’s.

It is worth noting that the Lightning Network has experienced a new class of attacks on Bitcoin’s mempool, which signaled alarms in the developer community building on the network. The fix has to be done on the base layer, specifically adding a memory-intensive history of all-seen transactions or some consensus upgrade, according to a suggestion made by Antoine Riard, a Bitcoin core developer who allegedly stepped back from the Lightning Network due to this “hard dilemma,” and will continue to shift his focus on Bitcoin core development.

Figure 4: Comparison between Active Addresses on Bitcoin and Ethereum’s Networks

Source: Glassnode

• Binance Enters Data Storage Space

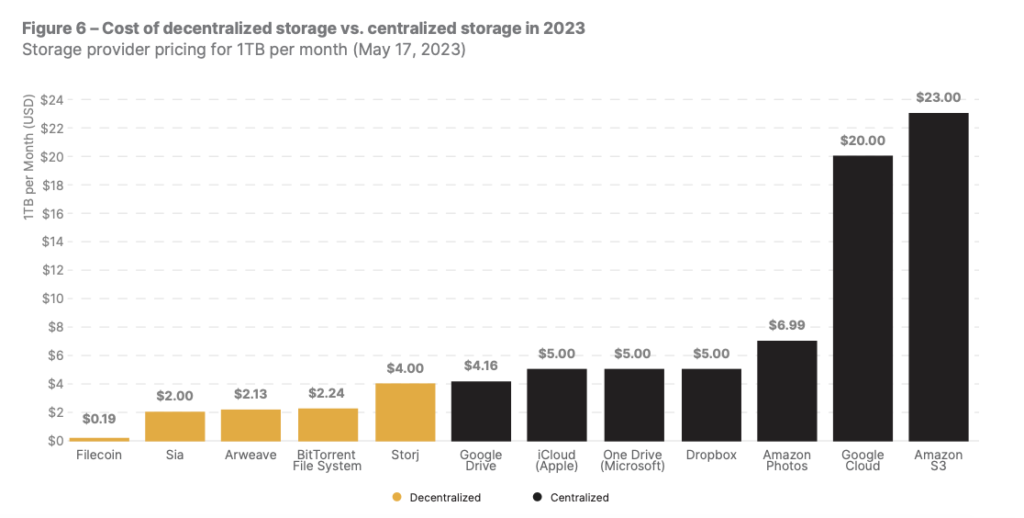

Binance’s venture into the decentralized storage space commenced last week with the launch of BNB Greenfield mainnet, focused on programmability, speed, and data control. BNB Greenfield aims to facilitate the decentralized data economy by simplifying the process of storing and managing data access, as well as linking data ownership with the massive DeFi context of the BNB Smart Chain (BSC). It enables Ethereum-compatible addresses to create and manage data and token assets seamlessly. It natively links data permissions and management logic onto BSC as exchangeable assets and smart contract programs, in turn providing developers with a more efficient and flexible way of managing their data and permissions. It provides similar API primitives and performance as popular existing Web 2 cloud storage systems.

With that said, BNB Greenfield not only competes with Web 2 counterparts like Amazon S3 and Google Cloud but with decentralized file storage applications like Arweave and Filecoin. In our latest State of Crypto, we delve deeper into the use case of data storage and how decentralized data storage blockchains have the potential to disrupt this space on the back of its permanent nature and the staggering cost discrepancies, which pour into the favor of decentralized data storage providers.

Figure 5: Cost of Decentralized vs. Centralized Storage in 2023

Source: Coingecko, from State of Crypto issue 10

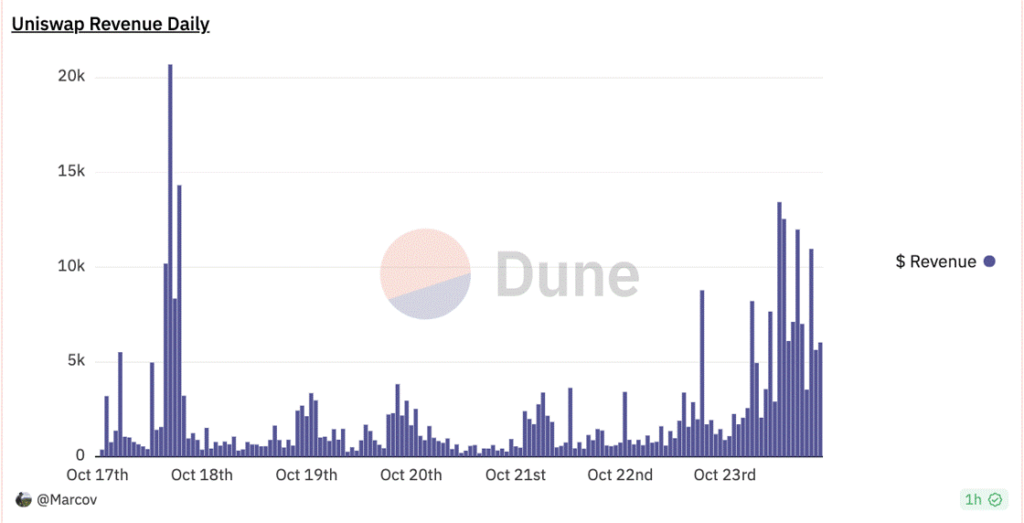

• Are Uniswap’s New Fees a Double-Edged Sword?

Uniswap Labs will charge 0.15% fee for swaps executed on Uniswap’s interface and wallet specifically for these pairs: ETH, USDC, WETH, USDT, DAI, WBTC, agEUR, GUSD, LUSD, EUROC, XSGD, while excluding inter-stablecoin trades. The new swap fees are being imposed on traders to fund ongoing development and research of the largest decentralized exchange by assets under management. Revenue from Liquidity Providers (LPs) will remain untouched since they are essential for the liquidity of Uniswap. However, the fee accrual does not benefit holders of UNI, which remains to be a low utility governance token. From October 17 to 24, Uniswap Labs has earned over $350K. However, we anticipate exchange aggregators to increase their market share moving forward as they don’t incur Uniswap’s front-end fees and can allocate users the best prices from different venues with the lowest costs.

Figure 6: Cumulative Daily Revenue of Uniswap

Source: Marcov on Dune Analytics

What You Should Pay Attention To

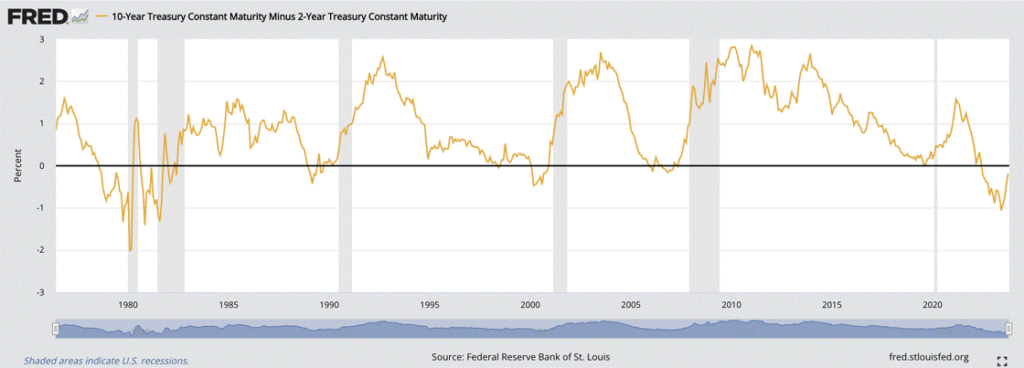

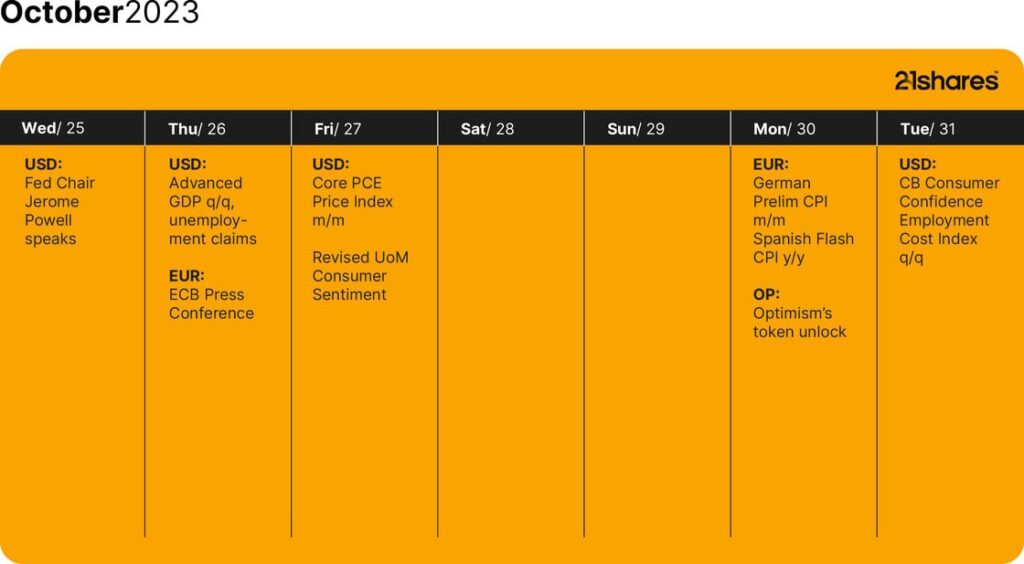

• Next Week’s FOMC Meeting: Can the Fed Impart Stability to the Bond Market?

The next Federal Open Market Committee (FOMC) meeting will be held on November 1, 2023. This is one of the key dates that investors should mark on their calendars due to the potential impact on global markets, including cryptoassets. The Fed held rates steady during their most recent meeting in September 2023, and Jerome Powell has hinted that the central bank may introduce one more 25 bps rate hike this year to moderate inflation to its 2% target. However, despite Powell’s signaling, the Fed must carefully balance the negative effects that increasing interest rates will have on global markets, particularly the banking sector, which already experienced turmoil in March. Figure 5 shows that the yield curve (10-year Treasury yield minus 2-year Treasury yield) is still inverted but close to going back to normal. Historically, this type of move has preceded global recessions, such as the 2008-9 Financial Crisis and the early 2000s recession after the dot-com bubble. How cryptoassets perform in such an environment remains to be seen, but recent history suggests that investors may turn to Bitcoin as a flight to quality due to its property of being a neutral, international, and censorship-resistant asset outside central banks’ control.

Figure 7: Yield Curve Inversion

Source: Federal Reserve Bank of St. Louis

• Solana’s Breakpoint 2023 Conference is Next Week

The annual gathering of the Solana community will take place in Amsterdam from October 30 to November 3. Some of the planned programming includes keynotes from industry leaders like Circle, Google Cloud, Visa, and Greenpeace. Investors should be on the lookout for announcements regarding new innovations and products, as it’s the norm for this type of event. Earlier this year, the Ethereum Community Conference (EthCC) was filled with exciting announcements, including Lens Protocol V2, Gnosis Pay’s self-custodial Visa card, Solang, UniswapX, and Chainlink’s CCIP. Solana remains one of the most vibrant ecosystems outside of Ethereum with almost 1,000 monthly active developers, demonstrating that it has retained a loyal community despite the challenges experienced by the ecosystem in the past year, such as the FTX collapse. Crucially, Solana has also attracted the attention of non-crypto native players like Fintech giants Visa and Shopify.

• Our Very Own Researcher Karim Saber Will Speak at DuneCon 2023

On November 2, data enthusiasts will gather in Lisbon for DuneCon 2023, Dune Analytic’s annual community conference. Our researcher, Karim, will deliver an insightful keynote on behalf of 21.co, parent company of 21Shares. Through our real-time dashboards, 21.co has pushed the industry standard to help investors stay ahead of the curve with key fundamental and momentum on-chain metrics related to Bitcoin, Ethereum, and the broader crypto ecosystem. For instance, we recently released seven dashboards to follow the evolution of the tokenization space across various assets, such as government securities, equities, and real estate. Although the conference will not be live-streamed, recordings may be available afterward.

Bookmarks

• Senior Research Associate Adrian Fritz was featured on Boerse Muenchen.

• Our Tokenization Report was featured on multiple media outlets, such as Laura Chin’s Unchained and Coindesk.

• Check out our webinar, where the Research Team introduced the State of Crypto, featuring a special guest.

• State of Crypto issue 10 is out! Discover how crypto is changing the world.

Next Week’s Calendar

This is what we’re monitoring for next week.

• October 25: Fed Chair Jerome Powell to deliver opening remarks at the Moynihan Lecture in Social Science and Public Policy, in Washington DC

• October 30: Optimism is set to unlock 2.74% of its current circulating supply

Research Newsletter

Each week the 21Shares Research team will publish our data-driven insights into the crypto asset world through this newsletter. Please direct any comments, questions, and words of feedback to research@21shares.com

Disclaimer

The information provided does not constitute a prospectus or other offering material and does not contain or constitute an offer to sell or a solicitation of any offer to buy securities in any jurisdiction. Some of the information published herein may contain forward-looking statements. Readers are cautioned that any such forward-looking statements are not guarantees of future performance and involve risks and uncertainties and that actual results may differ materially from those in the forward-looking statements as a result of various factors. The information contained herein may not be considered as economic, legal, tax or other advice and users are cautioned to base investment decisions or other decisions solely on the content hereof.

Schroders noterar aktiv USA-ETF på Xetra

Virtune noterar Virtune Sui ETP på Nasdaq Stockholm

Invesco: Gold signals a shifting world order without a new leader

ASLT ETF företagsobligatoner med kort duration

Anslut dig till kvantrevolutionen med Lunates nya ETF på Xetra

Vilka fonder lockade störst intresse under mars 2026?

Börshandlade fonder för kvantberäkning

Invesco on Iran war: Prudent response is to stay invested

ISRA ETF investerar i stora europeiska företag

Globala krypto-ETPer såg 1,8 miljarder dollar i nettoinflöden i mars

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanVilka fonder lockade störst intresse under mars 2026?

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanBörshandlade fonder för kvantberäkning

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanInvesco on Iran war: Prudent response is to stay invested

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanISRA ETF investerar i stora europeiska företag

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanGlobala krypto-ETPer såg 1,8 miljarder dollar i nettoinflöden i mars

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanAre you quantum ready?

-

Nyheter2 veckor sedan

Nyheter2 veckor sedan21shares korsnoterar nio ETPer på Xetra

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanXUML ETF återspeglar resultatet för amerikanska företag med stort börsvärde