Nyheter

Crypto Rallies to Wall Street’s FOMO: What Happened in Crypto This Week?

• 13F Filings Disclose Wall Street’s FOMO

• Crypto Soars as Inflation Shows Signs of Cooling

• Chainlink Continues Powering Tokenization

Crypto Soars as Inflation Shows Signs of Cooling

While inflation shows tentative signs of easing, both Bitcoin and Ethereum surged on positive macro data and market forecasts suggesting potential rate cuts. However, Fed officials seem to be less optimistic. We’ll explore the conflicting signals, unpack the Fed’s next move, and highlight key events that could impact markets this week.

The Consumer Price Index (CPI) dipped to 3.4% in April, down from March’s level of 3.5%. Similarly, Core CPI, which excludes food and energy prices, also slightly declined to 3.6%. This decrease, coupled with weaker-than-expected retail sales data, suggests consumer spending may be easing, further dampening inflationary pressures. However, the Producer Price Index (PPI), which reflects wholesale costs, exceeded expectations in April, suggesting price pressures persist and may eventually reach end-consumers.

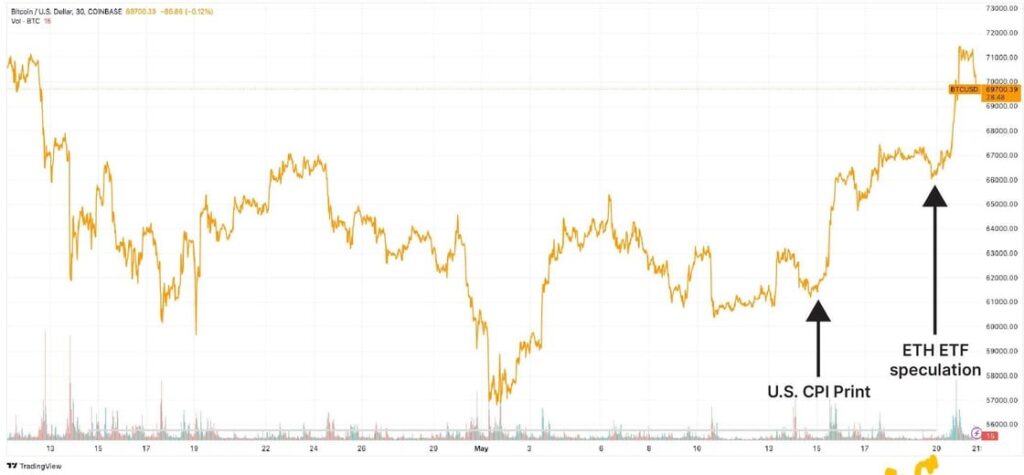

Nevertheless, the CPI news on May 15 was followed by a daily surge in Bitcoin’s price, jumping 7.5% to around $66K. Furthermore, on May 20, speculation around a potential ETH spot exchange-traded fund (ETF) in the U.S. sent the market on an even bigger rally, with Bitcoin and Ethereum surging by 13.6% and 24%, respectively over the past week.

Figure 1 – Bitcoin/USD Performance Against Last Week’s Events

Source: TradingView

Still, the high-for-longer sentiment seems to be the overarching theme in the Fed. Last week, high ranks of the Federal Reserve like Chair of Supervision Michael Barr and Vice Chair Philip Jefferson reiterated that although April’s reading may be considered encouraging, it’s still not enough to change the Fed’s stance on cutting interest rates.

Later today, members of the Federal Open Market Committee (FOMC) have a busy schedule of events where they’ll speak about economic outlook and monetary policy, which will be closely monitored given their effect on the general market sentiment.Coming out tomorrow, the minutes from the FOMC meeting earlier this month are expected to reveal further clarity on the Fed’s next move regarding interest rates and money supply. Should this reveal a dovish stance, investors may be pushed towards riskier assets. According to CME FedWatch, market participants are currently pricing a 60% chance of rate cuts in September and 88.5% in December.

13F Filings Disclose Wall Street FOMO

Beyond the macro news, on Wednesday the deadline for the 13F filings concluded, revealing significant Bitcoin holdings among investment managers. There are 937 professional investors holding $11B in the U.S. Spot Bitcoin ETFs, representing 18.7% of the ETFs’ assets under management. In comparison, Gold ETFs had a modest 95 professional firms invested by the first quarter following the launch. Hedge fund Millennium Management is the largest institutional holder of the new funds, with roughly $2B invested, however the reach extended beyond traditional investment firms.

It has also been made public that the State of Wisconsin Investment Board purchased more than $160M in shares of Bitcoin ETFs in Q1, with the majority of that representing assets in the Wisconsin Retirement System, a growing trend that exemplifies the demand for Bitcoin as a store of value. Additionally, some of America’s biggest banks who had voiced adversary stances towards crypto have also reported Bitcoin ETF holdings. Morgan Stanley has recently disclosed it has $270M worth of shares while JP Morgan has invested $1.2M.

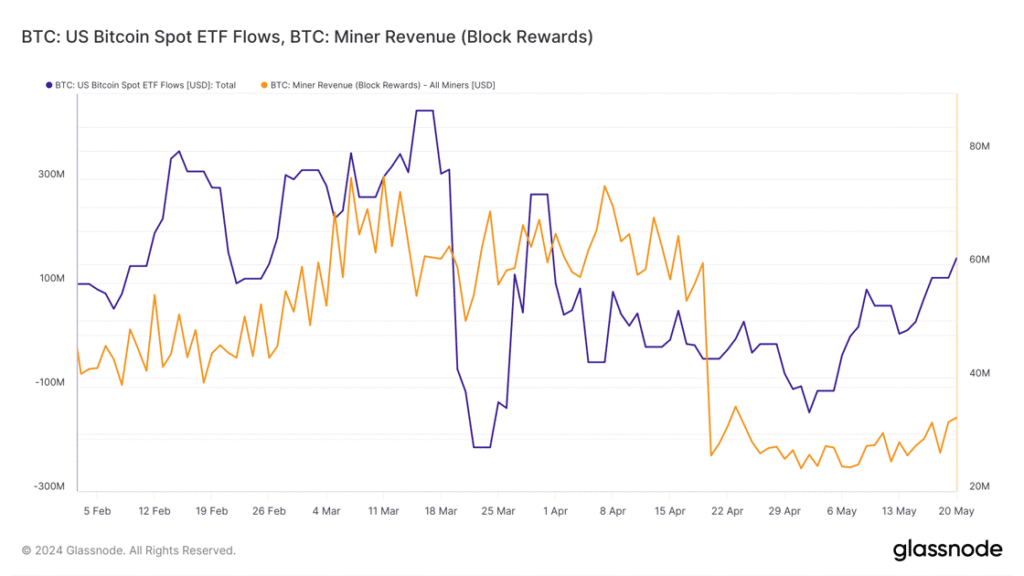

These disclosures are coming from the Wall Street giants who claimed Bitcoin was a bubble not so long ago. This level of adoption shows how Bitcoin’s fundamentals have pushed the world’s largest players to change their stance. Institutions are now mitigating their reputational risk by not delaying their Bitcoin adoption any further, which could otherwise be deemed unsound from an investment standpoint. On that front, last week Bitcoin ETFs crossed $1B in inflows, the best weekly performance since March, illustrating that Bitcoin adoption is not slowing down since the 13F filings. For instance, on a monthly basis, the ETFs have purchased over 21,700 BTC which is almost three times the new supply coming from miners, in the same time frame, as shown in Figure 2.

Figure 2 – US Bitcoin Spot ETF Flows vs. Bitcoin Block Rewards

Source: 21Shares, Glassnode

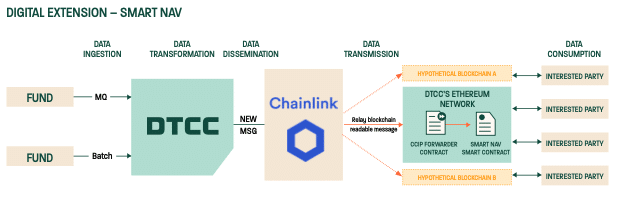

Chainlink Continues Powering Tokenization

Chainlink is the leading decentralized oracle network, bridging the gap between blockchains and the external world. While blockchains are powerful, they live in siloed environments, meaning they cannot access information or data that exists off-chain. Chainlink offers an expansive set of Oracle-based services and leverages its Cross-Chain Interoperability Protocol (CCIP) to integrate data from existing external systems across any blockchain securely. For instance, by providing Proof-of-Reserves for traditional assets or executing Verifiable Random Functions to fairly mint NFTs. Chainlink’s innovative solution has enabled over $10T in transactions across 22 separate blockchain networks, showcasing the reach this innovative protocol has on the wider industry.

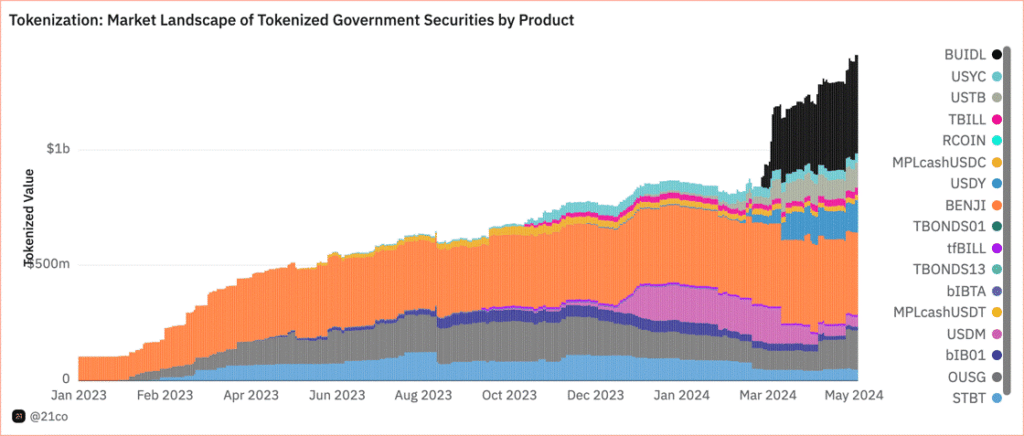

Last Thursday, the Depository Trust and Clearing Corporation (DTCC), the world’s largest securities settlement system which processed $3 quadrillion in securities in 2023, announced it successfully completed a pilot project in collaboration with Chainlink and major financial institutions such as BNY Mellon and JP Morgan. The project builds upon the existing DTCC Mutual Funds Profile Service I (MFPS I), which serves as the industry standard for transmitting NAV data, such as fund price and rate. The pilot does not affect initial workflows such as calculating fund data, as the focus was to create a standardized way to disseminate fund information across different blockchains. The project is likely to expedite real-world asset tokenization, which has become an increasingly important industry segment, showcased by tokenized government securities growing 10x in assets under management since the start of 2023, from nearly $100M to almost $1.4B.

Figure 3 – Market Landscape of Tokenized Government Securities by Product

Source: 21co on Dune Analytics

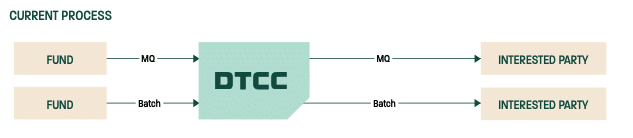

Every day, the DTCC’s service oversees the transmission of price and rate data for tens of thousands of mutual fund securities. In the current architecture, the DTCC links funds and service providers to distributors, collecting relevant fund data via a message queue and file-based methods, and finally disseminates them at regular intervals, as shown below.

Smart NAV extends the dissemination capabilities of MPFS I, where in addition to data being sent through existing channels, it is transformed into a modern JSON-based data structure. The newly formatted data is wrapped into a blockchain transaction, signed by DTCC’s private keys, and finally routed to Chainlink’s CCIP, allowing relevant fund data to be sent across almost any blockchain, private or public. Once the fund data is transmitted to these networks, a CCIP based smart contract forwards the data to the Smart-NAV-specific smart contracts responsible for validating permissions and storing data for the interested parties to consume.

The dissemination process highlighted above has an effect on traditional funds, as well as those represented on-chain. For instance, the real-time API sits off-chain and pushes fund data to all those integrated with the service. As soon as the relevant data is available, the API can be queried for both real-time and past information, which is impossible with the current MPFS I service. This distinction is crucial, as while the solution is inherently blockchain-based, it can clearly benefit participants who are not yet exploring tokenizing their funds, by allowing for faster and historical data dissemination. Additionally, Single Fund Consumer Smart Contracts and Bulk Consumer Smart Contracts, allowed participants to simulate tokenized funds, or a grouping of funds, which are instantly enriched with the respective data, as soon as available for the off-chain counterparty. This prevents users needing to store NAV data in a separate database that references the fund itself, thus allowing for a more streamlined tokenization process.

The collaboration between the DTCC and Chainlink represents a significant leap forward in the realm of tokenization. Chainlink’s CCIP abstracts away the need for the DTCC to directly connect to every blockchain network where tokenized funds may live on. This would be difficult for the DTCC to execute alone, given the potential costs and technical nuances that exist across chains. Hence, the use of Chainlink is vital as we envision a cross-chain tokenized landscape. The project presents a glimpse into the future where the process of distributing data is hosted on-chain, allowing for quicker, dynamic and historical distribution, empowering investors to make more informed investments. The project could be taken further to automate workflows, for instance the Bulk Consumer Smart Contract could represent a model portfolio, enabling the respective smart contract to rebalance these automatically. While the project is still young, any developments will be closely monitored, given the effect it would have on the growing industry segment of tokenization.

This Week’s Calendar

Source: Forex Factory, 21Shares

Research Newsletter

Each week the 21Shares Research team will publish our data-driven insights into the crypto asset world through this newsletter. Please direct any comments, questions, and words of feedback to research@21shares.com

Disclaimer

The information provided does not constitute a prospectus or other offering material and does not contain or constitute an offer to sell or a solicitation of any offer to buy securities in any jurisdiction. Some of the information published herein may contain forward-looking statements. Readers are cautioned that any such forward-looking statements are not guarantees of future performance and involve risks and uncertainties and that actual results may differ materially from those in the forward-looking statements as a result of various factors. The information contained herein may not be considered as economic, legal, tax or other advice and users are cautioned to base investment decisions or other decisions solely on the content hereof.

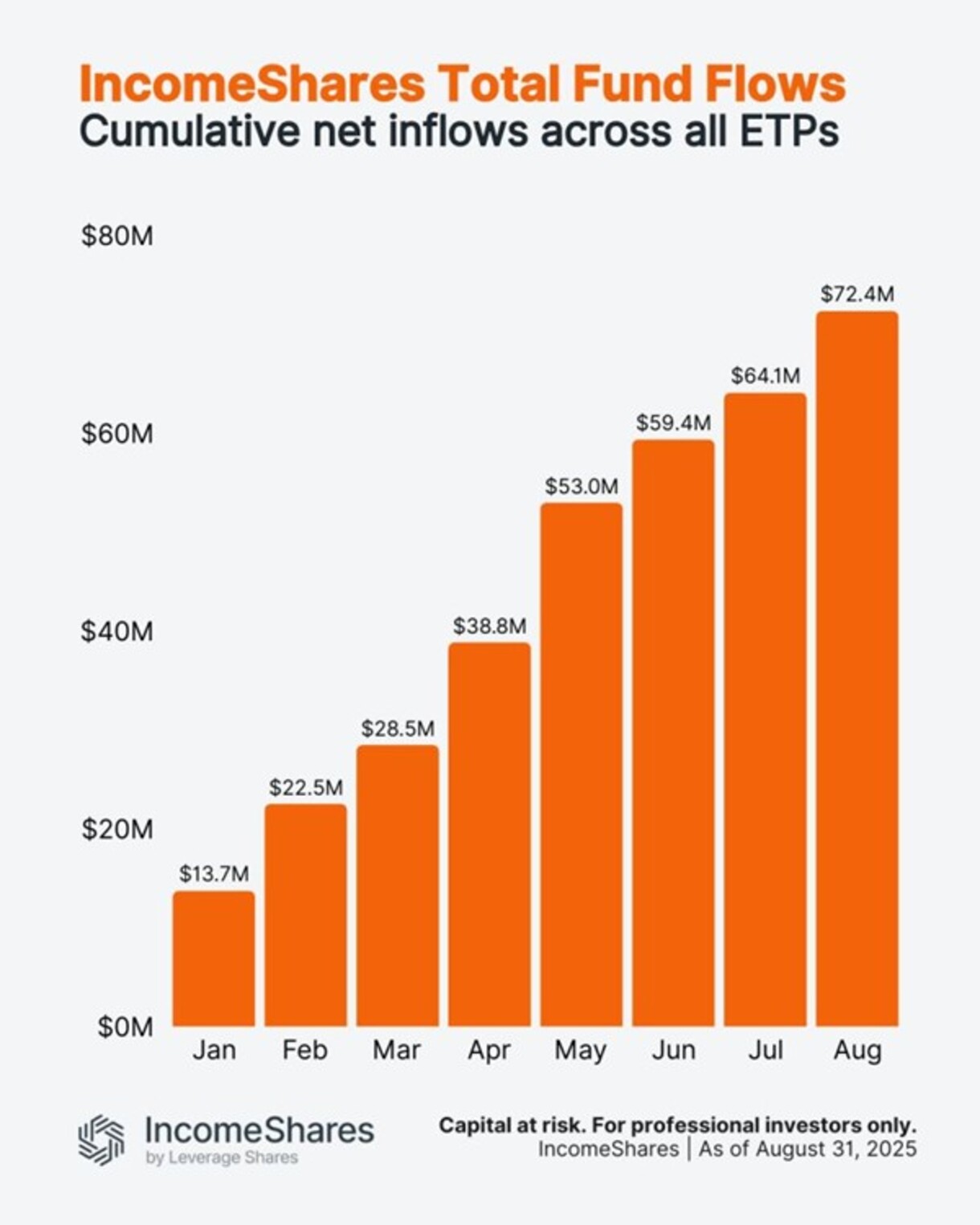

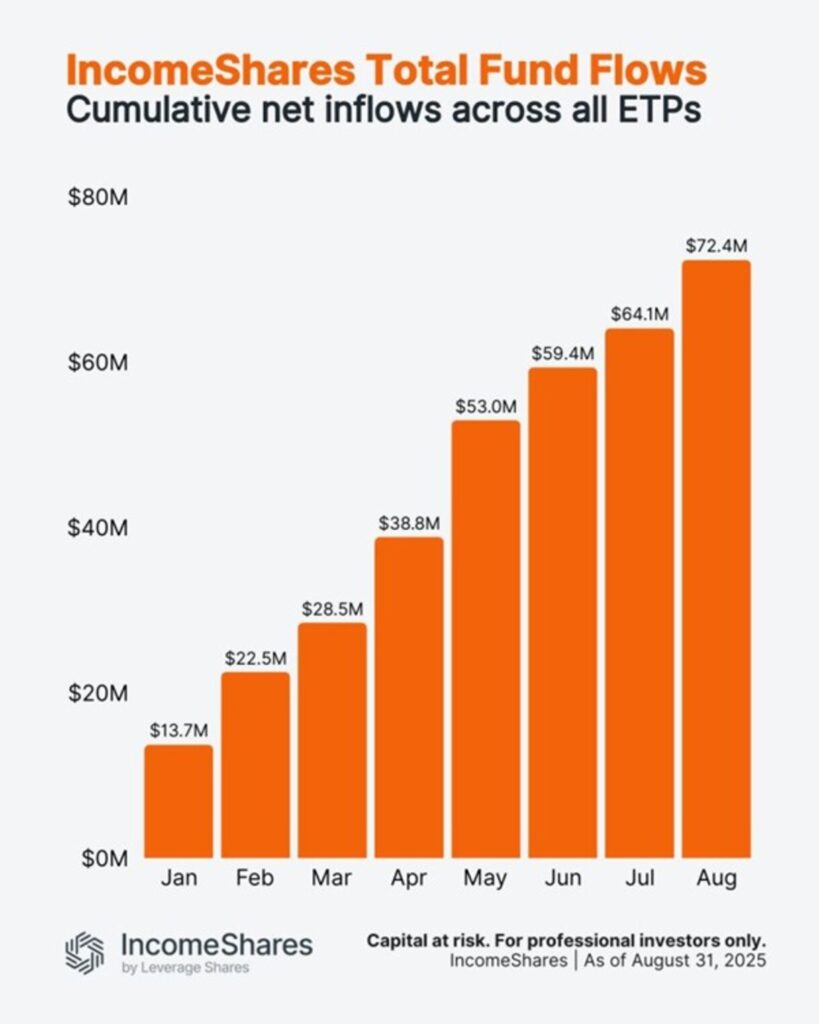

Fondflöden spårar hur mycket pengar investerare sätter in i eller tar ut från IncomeShares börshandlade produkter. Positiva fondflöden innebär att mer pengar kommer in än går ut – ett tecken på efterfrågan på börshandlade produkter.

Kumulativa fondflöden har ökat varje månad under 2025. I slutet av augusti nådde de 72,4 miljoner dollar. Det är över 8 miljoner dollar i nya pengar som tillkommit enbart i augusti – den största månatliga ökningen sedan maj.

Diagrammet nedan visar trenden.

Följ IncomeShares EU för fler uppdateringar.

XB28 ETF köper företagsobligationer med förfall 2028 och stänger sedan

IncomeShares fondflöden nådde en ny rekordnivå i augusti

JIGG ETF investerar i företagsobligationer från hela världen

JEQA ETF investerar i Nasdaq-100 i kombination med en derivatteknik

Bitwises Bradley Duke om marknadstrender och Bitcoin-utsikter

VALOUR ARB SEK spårar priset på kryptovalutan Arbitrum

Månadsutdelande ETFer uppdaterad med IncomeShares produkter

HANetfs analyserar hur ett fredsavtal kan påverka det europeiska försvaret

HANetfs VD kommenterar Trump-Putin-toppmötet

De bästa innovations-ETFerna

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanVALOUR ARB SEK spårar priset på kryptovalutan Arbitrum

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanMånadsutdelande ETFer uppdaterad med IncomeShares produkter

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanHANetfs analyserar hur ett fredsavtal kan påverka det europeiska försvaret

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanHANetfs VD kommenterar Trump-Putin-toppmötet

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanDe bästa innovations-ETFerna

-

Nyheter6 dagar sedan

Nyheter6 dagar sedanUtdelningar och försvarsfonder lockade i augusti

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanADLT ETF investerar bara i riktigt långa amerikanska statsobligationer

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanIncomeShares når 60 miljoner dollar i förvaltat kapital – Tillväxtöversikt 2025