Nyheter

Crypto Market Compass | 22. July 2024

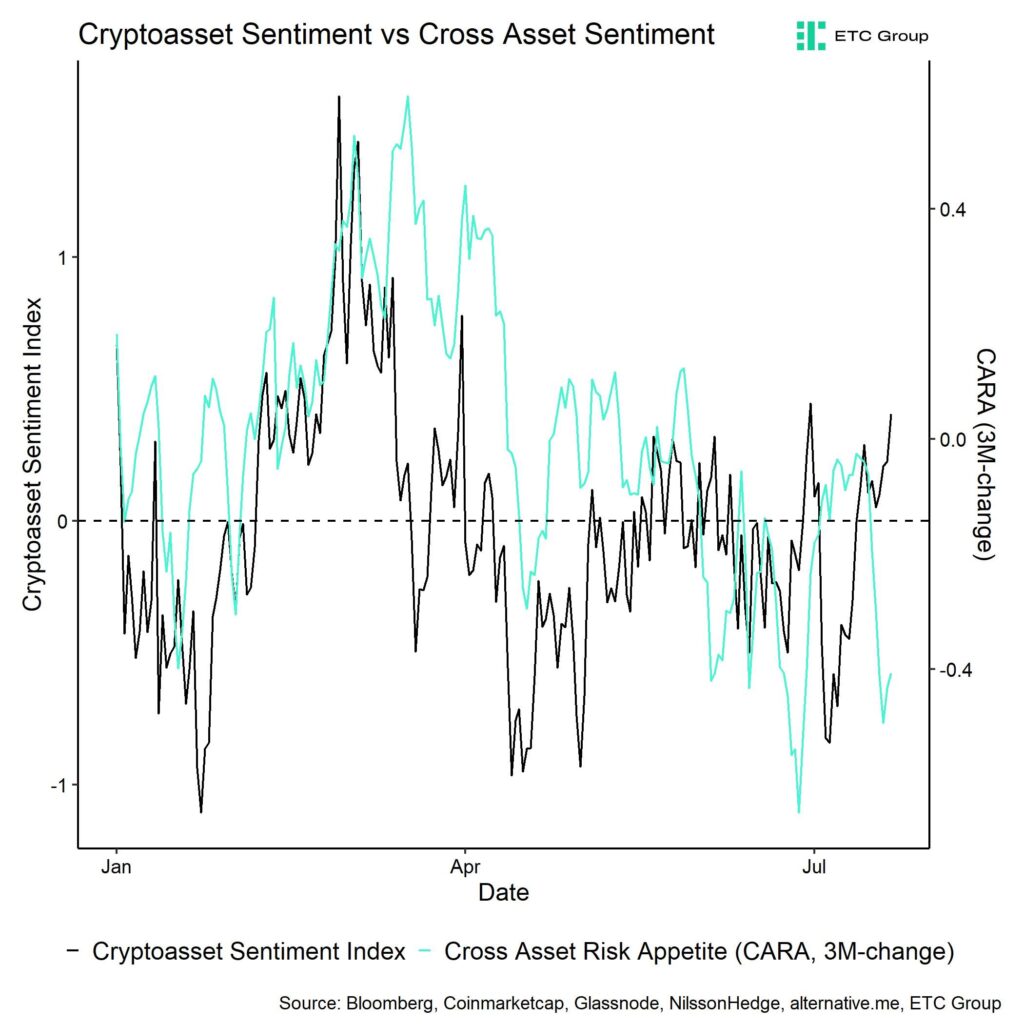

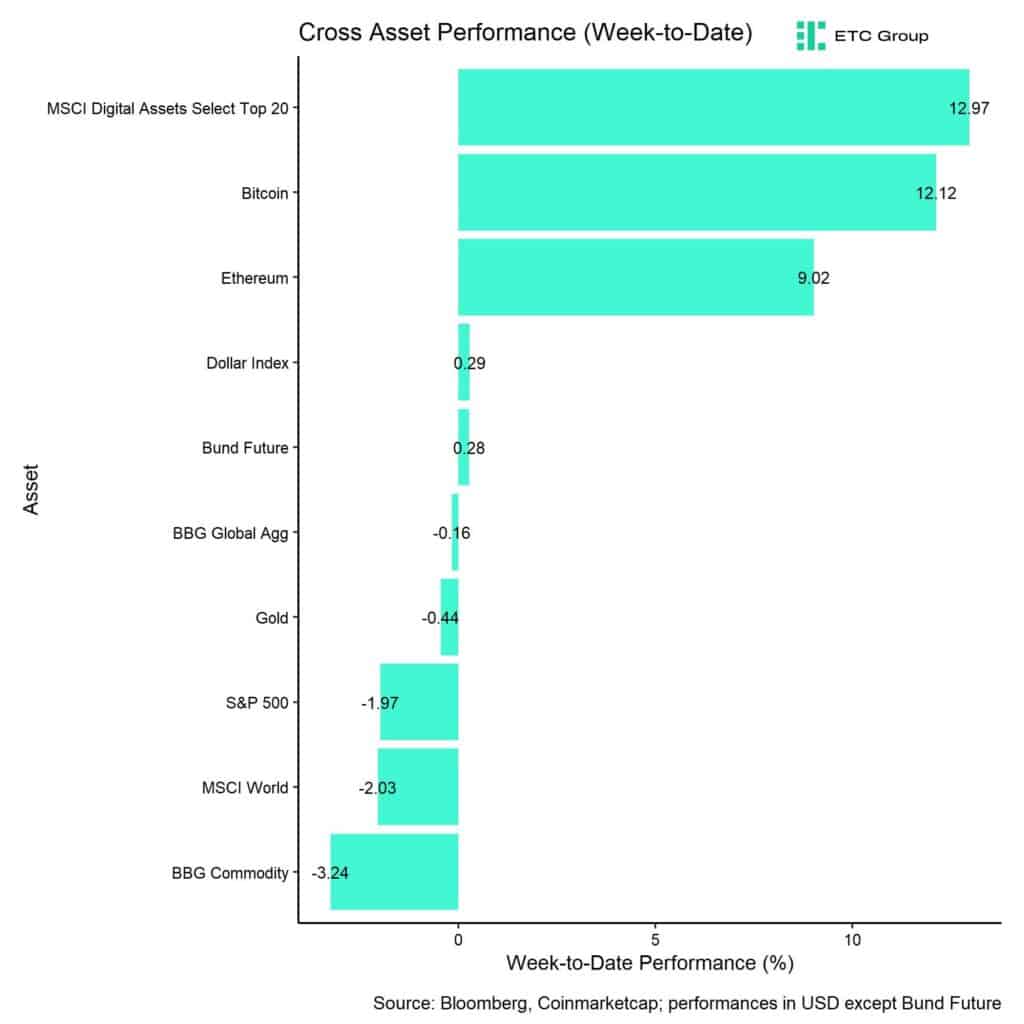

• Last week, cryptoassets decoupled from traditional financial assets such as equities on account of the global IT infrastructure outage caused by the faulty CrowdStrike software update.

• Our in-house “Cryptoasset Sentiment Index” has continued to climb and signals a slightly bullish sentiment.

• The global IT outage buoyed crypto market sentiment on account of the fact that major cryptoasset networks like Bitcoin continued to operate completely unaffected. This resulted in a decoupling of Cryptoasset Sentiment from Cross Asset Risk Appetite.

Chart of the Week

Performance

Last week, cryptoassets decoupled from traditional financial assets such as equities on account of the global IT infrastructure outage caused by the faulty CrowdStrike software update.

An estimated 8.5 million Microsoft Windows systems crashed and were unable to restart after an incorrect security software update was released by American cybersecurity company CrowdStrike on July 19. The biggest outage in the history of information technology was brought on by this, according to some reports.

This led to widespread global disruptions in transportation and financial sector operations that weighed on traditional financial markets. In contrast, the global IT outage buoyed crypto market sentiment on account of the fact that major cryptoasset networks like Bitcoin continued to operate completely unaffected. This resulted in a decoupling of Cryptoasset Sentiment from Cross Asset Risk Appetite (Chart-of-the-Week).

We think that this outage has made more investors aware of the meaning of a single-point-of-failure and the benefits of decentralized blockchain technology that underpin cryptoassets.

Moreover, although it has to be emphasized that this latest outage was not the result of a cyber attack, the IMF has just recently reiterated warnings that both the frequency and costs of cyber attacks has been rising globally which poses a threat to financial stability.

We think that Bitcoin and other cryptoassets may offer a pristine hedge against these kind of risks which is also supported by the latest outperformance.

Meanwhile, we saw a major announcement by incumbent president Biden to not pursue re-election in November which has led to a spike in election odds of current vice-president Kamala Harris relative to Trump. At the time of writing, betting markets price an election probability of 60% for Trump and 40% for Harris, according to PredictIt.

The market is awaiting further impulses from the speeches by both Trump and Kennedy Jr. at the upcoming Bitcoin Conference on the 27th of July.

Besides, a major focus this week will be the official trading launch of Ethereum spot ETFs in the US. Bloomberg analysts expect a launch to happen tomorrow (23rd of July) barring any unforeseeable last-minute issues. We expect a significant impact of these ETF flows on Ethereum’s performance post trading launch as outlined here.

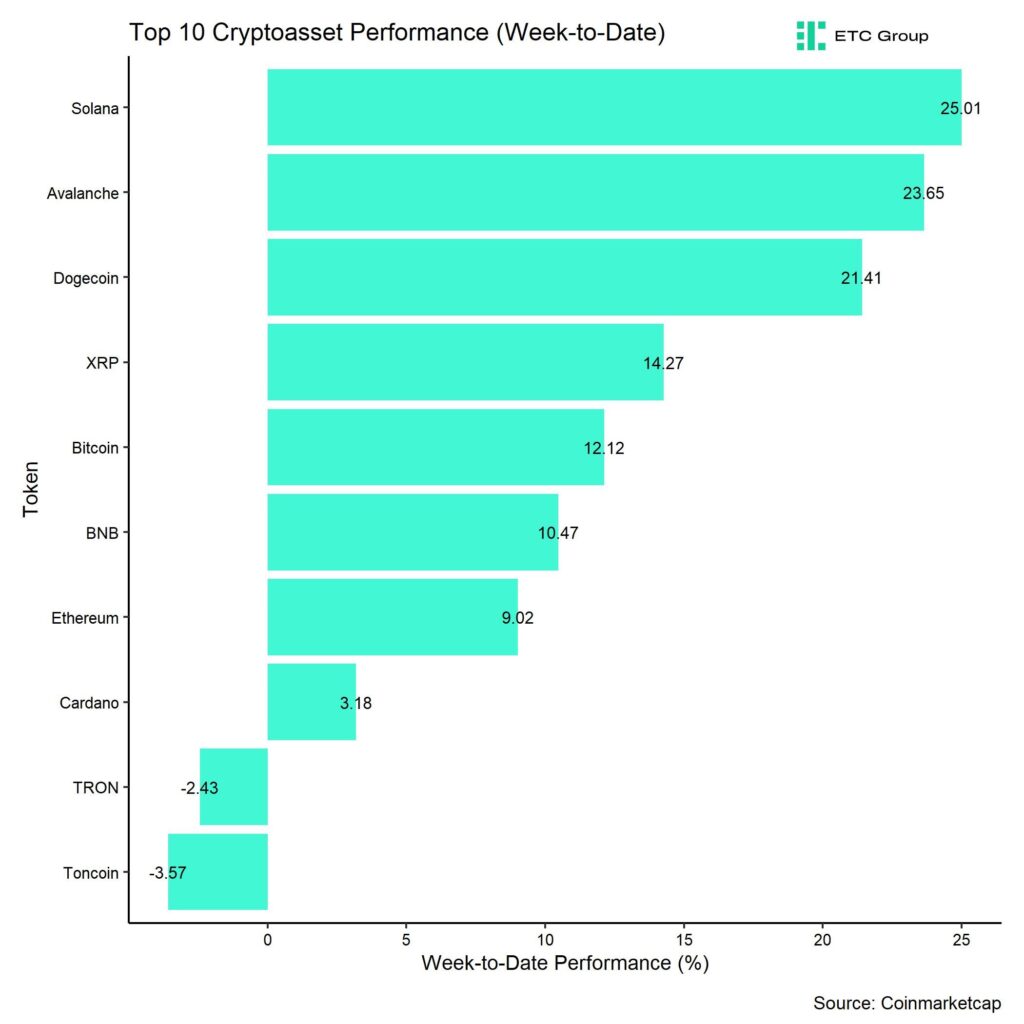

In general, among the top 10 crypto assets, Solana, Avalanche, and Dogecoin were the relative outperformers.

Overall, altcoin outperformance vis-à-vis Bitcoin has decreased again compared to the prior week, with only 10% of our tracked altcoins managing to outperform Bitcoin on a weekly basis. Ethereum also underperformed Bitcoin on a weekly basis.

Sentiment

Our in-house “Cryptoasset Sentiment Index” has continued to climb and signals a slightly bullish sentiment.

At the moment, 9 out of 15 indicators are above their short-term trend.

Last week, there were significant declines in the BTC 25-delta option skew and BTC relative put-call volume ratios which tend to be bullish signals.

The Crypto Fear & Greed Index has also reversed sharply and currently signals a “Greed” level of sentiment again as of this morning.

Performance dispersion among cryptoassets has increased slightly again but remains at low levels. This means that altcoins are still very much correlated with the performance of Bitcoin.

Altcoin outperformance vis-à-vis Bitcoin has declined again compared to the week prior, with only 10% of our tracked altcoins outperforming Bitcoin on a weekly basis, which is consistent with the fact that Ethereum also underperformed Bitcoin last week.

In general, increasing (decreasing) altcoin outperformance tends to be a sign of increasing (decreasing) risk appetite within cryptoasset markets and the latest altcoin underperformance is a signal of decreasing appetite for risk at the moment.

Meanwhile, sentiment in traditional financial markets as measured by our in-house measure of Cross Asset Risk Appetite (CARA) worsened and decoupled from the improving Cryptoasset Sentiment as shown in our latest Chart-of-the-Week.

Fund Flows

Fund flows into global crypto ETPs continued to be very positive but decelerated slightly compared to the prior week.

Global crypto ETPs saw around +1,393.1 mn USD in net inflows across all types of cryptoassets which is still very positive but somewhat lower than the +1,852.5 mn mn USD in net inflows recorded the prior week.

Global Bitcoin ETPs saw net inflows of +1,304.9 mn USD last week, of which +1,197.8 mn USD in net inflows were related to US spot Bitcoin ETFs alone. US spot Bitcoin ETF net inflows accelerated a bit compared to the prior week.

Last week saw a significant deceleration in net inflows into Hong Kong Bitcoin ETFs to only +18.4 mn USD after +451.9 mn USD in net inflows in the prior week.

Outflows from the ETC Group Physical Bitcoin ETP (BTCE) continued to decelerate last week with net outflows equivalent to -14.3 mn USD while the ETC Group Core Bitcoin ETP (BTC1) once again saw positive net inflows of +1.0 mn USD.

The Grayscale Bitcoin Trust (GBTC) continued to see some net outflows, with around -56.1 mn USD last week.

Meanwhile, global Ethereum ETPs also saw a slight deceleration in net inflows last week compared to the week prior with positive net inflows totalling +65.6 mn USD. Hong Kong Ethereum ETFs also attracted some capital last week (+14.5 mn USD).

The ETC Group Physical Ethereum ETP (ZETH) saw minor outflows last week (-0.5 mn USD) while the ETC Group Ethereum Staking ETP (ET32) showed a very significant increase in net inflows last week (+5.1 mn USD).

Altcoin ETPs ex Ethereum also an increase in net inflows of around +21.4 mn USD which was higher than last week.

Thematic & basket crypto ETPs continued to see only minor flows with only +1.2 mn USD, based on our calculations. The ETC Group MSCI Digital Assets Select 20 ETP (DA20) saw neither in- nor outflows last week (+/- 0 mn USD).

Meanwhile, global crypto hedge funds continued to increase their market exposure even further. The 20-days rolling beta of global crypto hedge funds’ performance increased to around 0.80 (up from 0.72) per yesterday’s close.

On-Chain Data

Bitcoin on-chain data have continued to improve at the margin over the past week.

Whale net exchange transfers have declined significantly to only ~4k BTC over the past week, down from a peak of 30.8k BTC reached on the 10th of July. This has significantly decreased selling pressure on Bitcoin exchanges. Whales are defined as network entities that control at least 1,000 BTC.

In fact, net buying volumes on bitcoin spot exchanges continued to be positive although they have decelerated again more recently. However, overall net transfers to bitcoin exchanges still remained relatively high over the past week implying significant transfers to exchanges by smaller investors.

This is one of the reasons why BTC exchange balances have continued to stay elevated near year-to-date highs according to data provided by Glassnode. In contrast, ETH exchange balances have moved mostly sideways over the past week.

That being said, both realized profits and losses have significantly declined since the beginning of July.

Besides, the transfers by the Mt Gox trustee wallets to Kraken did not affect selling pressure on exchanges meaningfully, yet. We also don’t expect the distribution of these bitcoins to be a significant drag on performance over the coming weeks since we only expect a small percentage of those coins to be liquidated.

The Mt Gox trustee balance has fallen to 89.8k BTC more recently, down from approximately 139k BTC in a sign of imminent redistribution of those coins to former holders.

Other large holders such as the US government have not distributed more bitcoins recently. However, a potential distribution still remains a risk over the short- to medium term since they had already distributed some bitcoins on the 25th of June. At the time of writing, the US government still controls around 207k BTC.

The overall hash rate in the Bitcoin network continued to recover in a sign of decreasing economic pressure on Bitcoin miners.

However, we have seen a notable decline in aggregate BTC miner balances more recently as miners sold the most bitcoins since January 2023 into the most recent rallye.

Continuing BTC miner distribution could also exert some downside pressure on the market in the short term.

Futures, Options & Perpetuals

Last week, both BTC futures and perpetual open interest continued to increase in a sign of a return in risk appetite. Futures liquidations were dominated by short liquidations as prices generally moved up.

Perpetual funding rates increased to a 1-month high which also signals increasing risk appetite. When the funding rate is positive (negative), long (short) positions periodically pay short (long) positions. A positive funding rate tends to be a sign of bullish sentiment in perpetual futures markets.

The 3-months annualized BTC futures basis rate also continued to increase to around 12.8% p.a.

Besides, there was a very significant increase in BTC options’ open interest which was mostly driven by an increase in BTC call option demand as evidenced by the continued drop in put-call open interest ratio.

This is consistent with the fact that both relative BTC put-call volume ratios as well as the 1-month 25-delta option skew also declined significantly signalling a drop in relative demand for put options.

Meanwhile, BTC option implied volatilities have increased significantly following the continued rallye. At the time of writing, implied volatilities of 1-month ATM Bitcoin options are currently at around 65.1% p.a.

Bottom Line

• Last week, cryptoassets decoupled from traditional financial assets such as equities on account of the global IT infrastructure outage caused by the faulty CrowdStrike software update.

• Our in-house “Cryptoasset Sentiment Index” has continued to climb and signals a slightly bullish sentiment.

• The global IT outage buoyed crypto market sentiment on account of the fact that major cryptoasset networks like Bitcoin continued to operate completely unaffected. This resulted in a decoupling of Cryptoasset Sentiment from Cross Asset Risk Appetite.

To read our Crypto Market Compass in full, please click the button below:

This is not investment advice. Capital at risk. Read the full disclaimer

© ETC Group 2019-2024 | All rights reserved

JGPD ETF är en aktivt förvaltad ETF som delar ut månadsvis

JP Morgan noterar tre nya ETFer på Xetra en av dem i SEK

OSYU ETF ger exponering mot Secured Overnight Financing Rate

iShares Space Technologies UCITS ETF investera bortom jorden

JIPD ETF delar ut månadsvis

USA satsar 2 miljarder dollar på kvantdatorer – så kan investerare dra nytta av utvecklingen

De bästa ETFerna för att investera i emerging markets

Extrema skillnader: Varför presterar Europas kvantdator-ETFer så olika?

Fastställd utdelning i MONTDIV maj 2026

Varför Plus500 är en dröm för finans-affiliate

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanUSA satsar 2 miljarder dollar på kvantdatorer – så kan investerare dra nytta av utvecklingen

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanDe bästa ETFerna för att investera i emerging markets

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanExtrema skillnader: Varför presterar Europas kvantdator-ETFer så olika?

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanFastställd utdelning i MONTDIV maj 2026

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanVarför Plus500 är en dröm för finans-affiliate

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanASWF ETF är en aktivt förvaltad fond som investerar i Kanada

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanETFer för fotbolls-VM 2026

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanQQCC ETF följer företag världen över som är aktiva inom kvantberäkning