Nyheter

Chinese Renminbi, The Basics

ETF Securities Currencies – Chinese Renminbi, The Basics

Summary

The liberalisation of currency controls and the growth of the “Dim-sum” bond market have seen the global trade of the hinese Renminbi (RMB) soar in recent years.

The RMB has come into sharp focus since last August, where its sudden depreciation generated a severe market selloff.

The RMB is traded on both onshore and offshore markets and rates between the two can differ.

Capital controls currently in place require the use of Non- Deliverable Forwards (NDFs) to gain exposure to the onshore RMB exchange rate for investors.

Download the complete report

A Brief History

Since the development of the Yuan in 1948, Chinese authorities have maintained strict control over its value, pegging it to the US Dollar at various levels to meet economic objectives1. From 1994, the fixed exchange rate regime saw China accumulate a large trade surplus and considerable foreign exchange reserves (see Figure 1) as the undervaluation of the currency kept international exports artificially competitive.

(click to enlarge) 1 A Yuan is a unit of Chinese currency and is to the Renminbi (RMB) what the Pound is to Sterling, so both terms can be used interchangeably.

Unsurprisingly, this policy was unpopular and generated pressure from its primary trading partners, pressure which in 2005 led to a movement towards a “managed floating” exchange rate regime and a removal of the peg. This gave the currency more flexibility but still allowed for government influence on its overall level.

In more recent years, Chinese authorities have altered course and have progressively removed barriers to the free trade of the RMB. These moves have prompted the growing use of the Yuan in international business, with the RMB recently surpassing the Japanese Yen to become the fourth most popular payment currency globally (SWIFT, 2015). In addition, the proliferation of the “Dim-sum” bond market in 2009, which are bonds issued outside of China denominated in RMB have also helped the internationalisation of the currency. Global bodies like the International Monetary Fund (IMF) have also acknowledged the increasingly “free” use of the RMB and have included the Yuan in the valuation of its coveted Special Drawing Rights (SDR) basket in October of last year.

(click to enlarge)

Many faces of the RMB

The global market for the RMB is somewhat segmented and so is quoted in a number of forms.

The RMB is traded both on the onshore Chinese market and on numerous offshore markets in Hong Kong, London, Singapore and New York. On a daily basis the People’s Bank of China (PBoC), the Chinese Central bank, provides a daily fixing (at 09.15 local time) for the onshore rate (CNY) against the a basket of reference currencies, around which the pair can trade within a ±2% band. This onshore market, despite being somewhat liberalised, is still subject to considerable regulation.

The offshore market rate (CNH) is not subject to as strict controls and is ultimately determined by market forces. While the CNY and CNH rates tend to move in tandem, differences in liquidity and capital restrictions on arbitrage prevent this gap from closing permanently (see Figure 2).

Yuan plunges

On August 11th 2015, the PBoC announced that it would modify the mechanism through which the daily Yuan fixing would take place. In attempt to foster a more “market-driven” process, quotes from onshore primary dealers would be used as inputs into the calculation of the fix on a daily basis. That morning, the USD/CNY fix plunged 1.9% and the next day a further 1.0% in response, the largest absolute one day moves since the peg was removed in 2005.

The sharp declines sparked speculation that Chinese authorities were more concerned about domestic growth than previously anticipated and permitted the depreciation to boost the competitiveness of Chinese exports. The Chinese stock market reaction was sharp; with the Hang Seng Index plunging 3% intraday (see Figure 3). The impact was felt globally, with other major equity indices also falling considerably, only to recoup losses in the subsequent trade.

(click to enlarge)

How to trade the CNY

Due to trading restrictions imposed on the CNY, a liquid market for CNY Non-Deliverable Forwards (NDFs) has blossomed. An NDF is a forward contract that fixes the exchange rate for a currency transaction at some point in the future. At expiry the profit/loss of the underlying contract is calculated and converted into US Dollars and settled.

NDF’s evolved out of the necessity for market participants to hedge exposure to currencies such as the CNY, Taiwan Dollar (TWD) and the Brazilian Real (BRL) all of which are subject to capital controls and cannot be physically delivered. Like FX forwards, the rates at which NDFs price is based on expected future interest rate differentials between the two relevant currencies.

When using NDFs, an investor has to “roll” his/her position prior to expiry in order for the currency exposure to be maintained. “Rolling” involves closing out a near term position before it expires and re-investing in a longer dated forward. Like in other asset classes this process can incur a cost/gain depending on the shape of the forward curve. As mentioned previously, interest rate differentials determine forward FX levels and thus dictate the shape of the curve and the corresponding impact of the roll (see Figure 4).

(click to enlarge)

An alternative to investing through NDF’s directly is to utilise currency exchange traded products (ETPs). Currency ETPs provide a transparent, liquid and freely tradable medium through which to gain access to emerging market currency pairs. Currency ETPs trade like shares and mitigate some of the operational complexities involved in investing in NDFs, although indices are priced from NDF’s.

Prospects for the CNY

Chinese authorities continue to manage the nation’s transition from an export and investment led fast growing economy to a more moderate mature consumer driven model. Recent declines in the PBoC’s FX reserves and intervention in the onshore stock market reflect the government’s desire for stability during this period of change. Therefore the possibility of further monetary intervention remains, which, in the near term which could weigh the RMB.

Important Information

This communication has been issued and approved for the purpose of section 21 of the Financial Services and Markets Act 2000 by ETF Securities (UK) Limited (“ETFS UK”) which is authorised and regulated by the United Kingdom Financial Conduct Authority (the “FCA”).

The information contained in this communication is for your general information only and is neither an offer for sale nor a solicitation of an offer to buy securities. This communication should not be used as the basis for any investment decision. Historical performance is not an indication of future performance and any investments may go down in value.

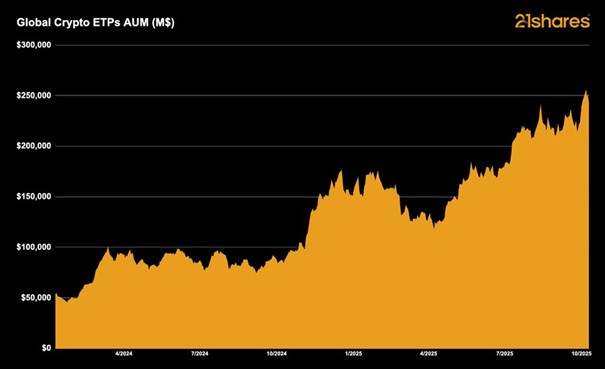

I början av året förutspådde 21shares att krypto-ETPer skulle driva ytterligare institutionell adoption och nå 250 miljarder dollar i förvaltat kapital globalt. Den milstolpen har just nåtts.

Research Newsletter

Each week the 21Shares Research team will publish our data-driven insights into the crypto asset world through this newsletter. Please direct any comments, questions, and words of feedback to research@21shares.com

Disclaimer

The information provided does not constitute a prospectus or other offering material and does not contain or constitute an offer to sell or a solicitation of any offer to buy securities in any jurisdiction. Some of the information published herein may contain forward-looking statements. Readers are cautioned that any such forward-looking statements are not guarantees of future performance and involve risks and uncertainties and that actual results may differ materially from those in the forward-looking statements as a result of various factors. The information contained herein may not be considered as economic, legal, tax or other advice and users are cautioned to base investment decisions or other decisions solely on the content hereof.

Globala krypto-ETPer förvaltade tillgångar når 250 miljarder dollar

YGLD ETP spårar priset på guld och ger en löpande avkastning

Investera i Stacks med en börshandlad produkt

VALOUR FLR SEK följer priset på kryptovalutan FLR

BlackRock utökar sitt utbud av iShares iBonds UCITS ETFer med sex nya lanseringar

HANetf och Infrastructure Capital Advisors samarbetar för att lansera aktivt förvaltad preferensavkastnings-ETF i Europa

IN0A ETF spårar S&P 500 med fokus på företag med höga ESG-betyg

De bästa lågvolatilitets ETFer på marknaden

PLTY ETP utfärdar optioner mot aktier i Palantir

Time in Bitcoin beats timing Bitcoin

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanHANetf och Infrastructure Capital Advisors samarbetar för att lansera aktivt förvaltad preferensavkastnings-ETF i Europa

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanIN0A ETF spårar S&P 500 med fokus på företag med höga ESG-betyg

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanDe bästa lågvolatilitets ETFer på marknaden

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanPLTY ETP utfärdar optioner mot aktier i Palantir

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanTime in Bitcoin beats timing Bitcoin

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanHANetf kommenterar kopparuppgången

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanFokus mot en helt ny börshandlad produkt i september 2025

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanM5TYs senaste utdelningstakt (55 %) belyser covered call-strategins inkomstpotential