Nyheter

”Is Wall Street warming up to Crypto?”

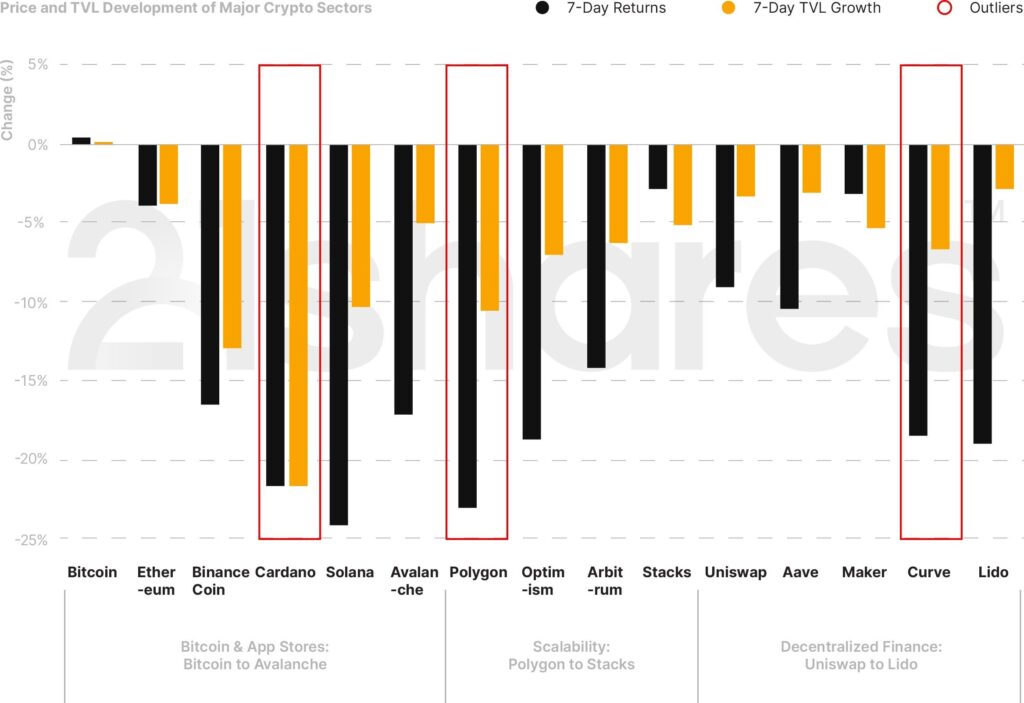

Markets continued to suffer on the back of the latest SEC complaints, with a new lawsuit launched against Coinbase and an unprecedented motion to freeze the assets of Binance’s US entity. Between June 5 and June 10, we saw more than $1 billion of mainly long liquidations. Long tail assets outside Bitcoin and Ethereum dropped by more than 20% week over week, especially alleged securities by the SEC. Spreads on Binance US became about 20 times wider than those on Coinbase and Kraken — and market depth dropped by 78% since the SEC crackdown. There is a flight to quality and safety with a rising Bitcoin dominance approaching the 50% mark, an all-time high in months while Tether’s market value broke a record of $83.3 billion.

Figure 1: Weekly TVL and Price Performance of Major Crypto Categories

Source: Coingecko and DeFi Llama. Close data as of June 12.

5 Things to Remember in Markets this Week

• Regulatory headwinds in the U.S. continue to pressure Coinbase and Binance: The Securities and Exchanges Commission (SEC) sued Coinbase over operating an unregistered exchange. The SEC also filed a temporary restraining order and motion to freeze assets held by Binance and its founder, Champeng Zhao, which is an unprecedented move against the world’s largest exchange, foreshadowing a prolonged regulatory crackdown on centralized exchanges. The recent complaints alongside the fall of FTX created a paradigm shift in investor behaviors with decentralized exchanges like Uniswap gathering more traction due to outflows from Binance and Coinbase. However, as discussed in this report, decentralized entities might no longer be immune to regulatory scrutiny.

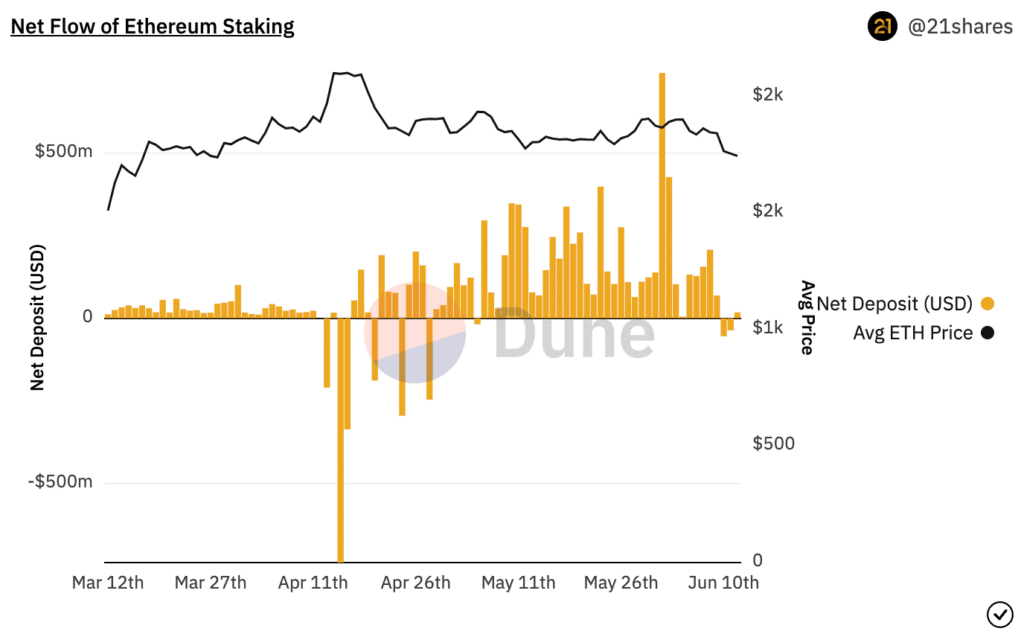

Figure 2: Net Flow Ethereum Staking

Source: 21shares on Dune Analytics

Ethereum staking experienced two consecutive days of outflows for the first time since April, as shown in Figure 2, most exits in the past week originated from Coinbase.

• Adoption in Hong Kong and Singapore grows: A member of the Legislative Council of Hong Kong extended an open invitation to welcome all global digital asset marketplaces including Coinbase to register in HK. Hong Kong aims to become a global crypto hub by attracting foreign investments, for example, the first Chinese financial institution to issue a tokenized security. In collaboration with UBS, and under both Swiss and English law, Bank of China investment bank issued structured notes worth the equivalent of $28M (200 million of offshore renminbi) on the Ethereum blockchain. Moreover, Circle obtained a license from Singapore to offer digital payment token services and cross-border and domestic money transfer services which outlines the scale of adoption of real-world assets in the city-state.

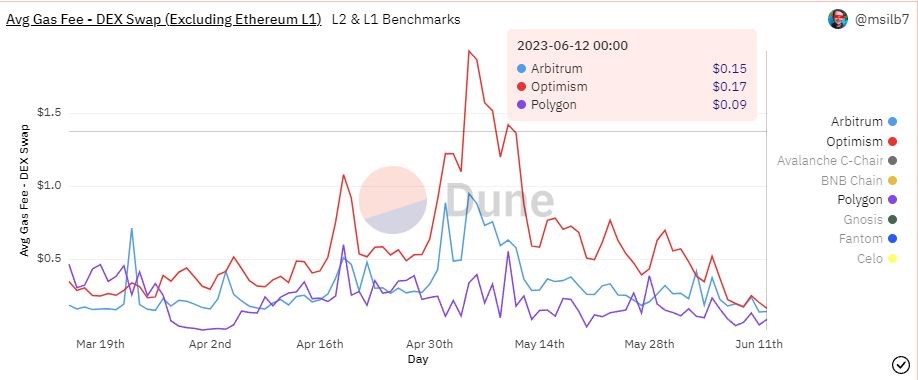

• Ethereum formalizes the scope of improvements for the next major upgrade: Dubbed Dencun, the next network upgrade will introduce five improvement proposals designed to expand the data storage capacity and reduce transaction costs: EIP-1153, 4788, 5656, and EIP 6780. However, the focus will be on EIP 4844, otherwise named Proto-DankSharding, which will allocate more space for ‘data blobs’. Blobs refer to transactions that are only stored by Ethereum’s consensus layer, which effectively makes the data processing from layer 2 networks to Ethereum much cheaper than historically (). Optimism, a layer 2 network, is anticipated to be among the primary beneficiaries of this upgrade, particularly as the Bedrock upgrade has markedly enhanced the network’s performance by reducing the average transaction fees by more than 50%. The upgrade will facilitate the realization of scaling networks’ full potential by providing a cost-effective solution for conducting financial activities on-chain for tokenization and other use cases.

Figure 3: Comparing L2 Fees

Source: @msilb7 on Dune Analytics

• Polygon: The pioneering scalability solution of Ethereum has unveiled its strategic initiative to transform and enhance the network’s infrastructure. Referred to as Polygon 2.0, this innovative design embraces a network of Layer2 solutions, leveraging Zero Knowledge technology. As a reminder, Zero-knowledge refers to a method that allows verifying information without revealing any underlying data, ensuring privacy and security in transactions. That said, the new architecture aims to consolidate Polygon’s diverse scaling offerings into a unified framework, enabling users to transition between various scaling services effortlessly. Ultimately, the upgraded Polygon network will focus on establishing a seamless and interconnected web of L2 chains, empowered and interconnected through Zero-Knowledge Proofs technology.

• Adoption of NFTs grows within the crypto community, while regulatory headwinds drive Web3 outside of the US: Kraken launched their NFT marketplace on June 8, expanding its offering now to include Polygon NFTs, such as Reddit collectible avatars. Its beta version already supported Ethereum and Solana. Kraken is making an effort to make NFTs simple and accessible to a broader audience without the need to own self-custody wallets.

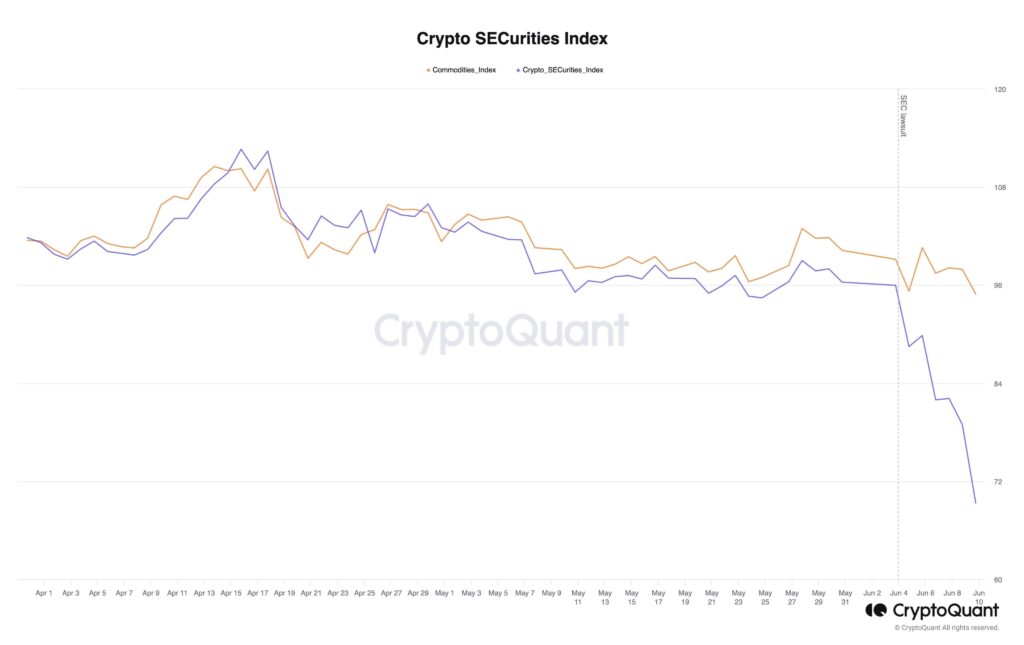

What You Should Pay Attention To Assets classified as securities by the SEC are likely to face stricter market conditions

Thus, we could see US-based exchanges exercising caution with respect to these disputed assets until there is further clarity, potentially leading to a wave of delistings. For instance, Robinhood removed SOL, ADA, and MATIC from its platform due to their involvement in the civil lawsuit against Coinbase last week. For context, users have until the 27th to withdraw their assets to external wallets. Otherwise, the platform will automatically sell them and credit the accounts with the corresponding USD value. Etoro took a similar stance as they disabled the purchase of MANA, MATIC, and ALGO. In that view, we anticipate a gradual flight to safety with capital migrating towards Bitcoin and Ethereum, as the ongoing trend of delistings could increase the selling pressure on the disputed assets. The ongoing movement towards high-quality assets is evident as Bitcoin’s dominance broke through its 2.5-year resistance level of 47%, signaling a notable shift in the market dynamic.

Figure 4: Token index composed of assets initially deemed as securities by SEC v. the broader market

Source: CryptoQuant

Binance is lawyering up, while Coinbase will keep fighting for regulatory clarity in court: Coinbase is determined to contest the allegations in court, evident by their CEO, Brian Armstrong, interview with the Wall Street Journal. The outcome of this case is of great significance to the industry, as Coinbase is focused on addressing the absence of clear regulatory recognition for assets that initially represent security traits during capital raising but later transition into utility tokens as the ecosystem grows and more sophisticated use cases emerge. At the same time, the network continues to decentralize over time. Monitoring this case as a precedent is vital, as it will shed light on a crucial aspect of the structure and utility of tokens, as well as establish their legal status in the United States. Alternatively, it is possible that the Department of Justice (DOJ) and the Commodity Futures Trading Commission (CFTC) may take further regulatory action against Binance. The latter also prepares for this battle by staffing a global sanctions and CTF Investigations team. So far, Binance has endured almost $300M in net flows in the past 24 hours, according to our dashboard on Dune Analytics.

Polygon is poised to serve as the foundational value layer of the internet. As further information unfolds in the coming weeks regarding the new network, the redesigned structure of the Matic token, and the seamless integration of the comprehensive blockchain framework, Polygon’s forthcoming architecture emerges as a captivating development. By harnessing zero-knowledge proof technology to enable intercommunication between sovereign networks, Polygon is well-positioned to address critical barriers to entry in the realm of cross-chain communication, especially as it pertains to unified liquidity. This strategic direction positions Polygon to become a formidable infrastructure leader, consolidating its array of scaling solutions and competing effectively against leading rollup networks such as Optimism and Arbitrum, which are also offering interconnected L3 layers through their Superchain and Orbit initiatives.

Decentralized autonomous organizations (DAOs) and decent*ralized exchanges (DEXs) could be held legally liable for their actions in the U.S. The Commodity Futures Trading Commission (CFTC) won its lawsuit against Ooki DAO, a decentralized autonomous organization operating tokenized margin trading and lending protocol for tokenized margin trading and lending. This is the first time a DAO is held liable in the eyes of the law in the U.S., which could set the precedent DAOs of any kind including DEXs in the future. The silver lining here is that bad actors or offshore entities may no longer be able to circumvent the law under the invisibility cloak of decentralization.

Next Week’s Calendar

These are the top 3 events we’re monitoring for next week.

• The Future of Digital Assets: Providing Clarity for the Digital Asset Ecosystem US House Financial Services Committee to hold a session that will be important to monitor as it builds on the newly introduced bill called “Digital Asset Market Structure” proposed by House Financial Services Committee Chair Patrick Mchenry and Agriculture Committee Chair Glenn which should help provide a statutory framework for digital assets, combined with a bipartisan bill draft for stablecoin issuance.

• The unsealing of the Hinman documents in the Ripple v. SEC case should help drive further regulatory clarity around Bitcoin as it pertains to how the agency views statements made about the asset in terms of its designation as a security or a commodity.

• FOMC minutes on Wednesday should paint a more complete picture of where the FED stands regarding rate hikes based on their analysis of the CPI, which rose at a 4% annual rate in May, the lowest in two years, although core inflation was still up 5.3% from a year ago.

Source: Forex Factory, CoinMarketCal

Research Newsletter

Each week the 21Shares Research team will publish our data-driven insights into the crypto asset world through this newsletter. Please direct any comments, questions, and words of feedback to research@21shares.com

Disclaimer

The information provided does not constitute a prospectus or other offering material and does not contain or constitute an offer to sell or a solicitation of any offer to buy securities in any jurisdiction. Some of the information published herein may contain forward-looking statements. Readers are cautioned that any such forward-looking statements are not guarantees of future performance and involve risks and uncertainties and that actual results may differ materially from those in the forward-looking statements as a result of various factors. The information contained herein may not be considered as economic, legal, tax or other advice and users are cautioned to base investment decisions or other decisions solely on the content hereof.

HEQD ETF investerar i aktier som handlas på Nasdaq

MNTE ETF är en buffert-ETF som spårar amerikanska storbolag

Vilken typ av sektor ETFer finns det?

LVLD ETF investerar i ett urval av företag världen över med låg volatilitet

Den europeiska ETF-revolutionen: Skiftet som ritar om kartan för kapitalförvaltning

USA satsar 2 miljarder dollar på kvantdatorer – så kan investerare dra nytta av utvecklingen

Extrema skillnader: Varför presterar Europas kvantdator-ETFer så olika?

QQCC ETF följer företag världen över som är aktiva inom kvantberäkning

Varför Plus500 är en dröm för finans-affiliate

Den osynliga flaskhalsen i AI-boomen: Varför elinfrastruktur är nästa stora megatrend

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanUSA satsar 2 miljarder dollar på kvantdatorer – så kan investerare dra nytta av utvecklingen

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanExtrema skillnader: Varför presterar Europas kvantdator-ETFer så olika?

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanQQCC ETF följer företag världen över som är aktiva inom kvantberäkning

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanVarför Plus500 är en dröm för finans-affiliate

-

Nyheter1 vecka sedan

Nyheter1 vecka sedanDen osynliga flaskhalsen i AI-boomen: Varför elinfrastruktur är nästa stora megatrend

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanETFer för fotbolls-VM 2026

-

Nyheter4 veckor sedan

Nyheter4 veckor sedan21shares produkter nu finns tillgängliga hos Revolut

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanOlja och Hormuzsundet fick flest sökningar i maj 2026