Nyheter

Varför priset på Bitcoin rusat till sin högsta nivå på sex månader

Bitcoin lade till 40 miljarder dollar till sitt börsvärde över natten den 16 februari när det positiva sentimentet började vinna mark och en så kallas short squeeze sköt värdet på kryptotillgången till sitt högsta pris på sex månader. I denna artikel tittar ETC Group på varför priset på Bitcoin rusat till sin högsta nivå på sex månader

Bitcoin har nu stigit med 11,19 procent under de senaste 24 timmarna för att nå 24 500 USD och Ethereum har hoppat till 1 680 USD.

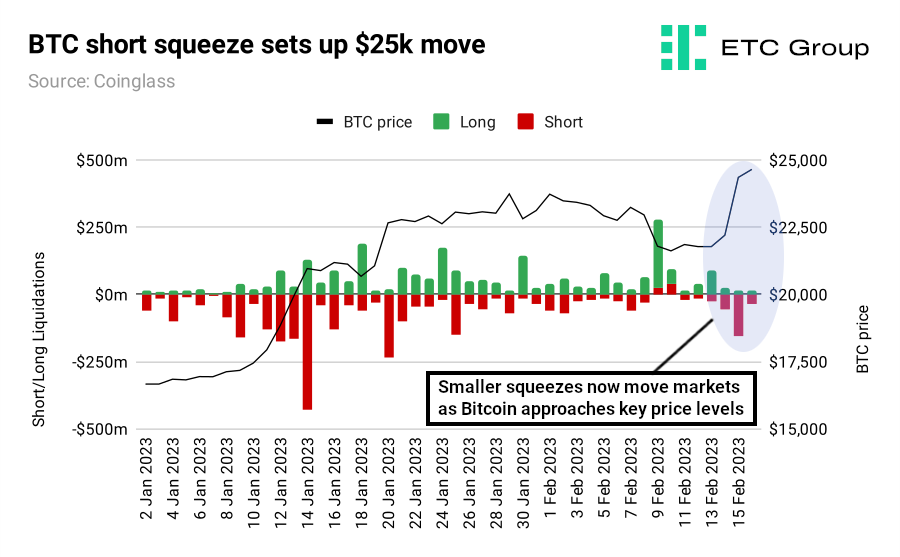

Det började med en short squeeze, men en rad spännande mindre händelser påverkar också samtidigt Bitcoin närmar sig en nyckelprisnivå. Utbudet av Bitcoins där innehavarna har vinst är nu den högsta nivån sedan i april 2022.

Short squeeze flyttar marknader: nyckelpriser strategi

Data från derivatsajten Coinglass visar att blankare– de som satsar på att priset på Bitcoin kommer att falla – slogs ut från sina positioner mellan 13 och 16 februari. Siffrorna visar att cirka 190 miljoner USD av korta Bitcoin-positioner likviderades under dessa 48 timmarna.

När blankningssäljare ser att deras stop loss överskrids, tvingas de köpa tillbaka Bitcoin till de nya, högre marknadspriserna, vilket i sin tur ser att det tillgängliga utbudet av Bitcoin på börser minskar, och det finns en allmän brådska från blankarna att köpa tillbaka till lägsta tillgängliga pris och därmed undvika stora potentiella förluster.

Med denna senaste prishöjning har Bitcoin sprungit ända upp till 24,5 000 dollar, det högsta priset kryptovalutan har handlats till på sex månader. Det som är mest spännande med vad som händer den här gången är att det krävs relativt små mängder positionering på handelsmarknaden för att få dessa rörelser att hända. För oss drar det slutsatsen att det råder en allmän säljarutmattning vid dessa prisnivåer.

Källa: ETC Group

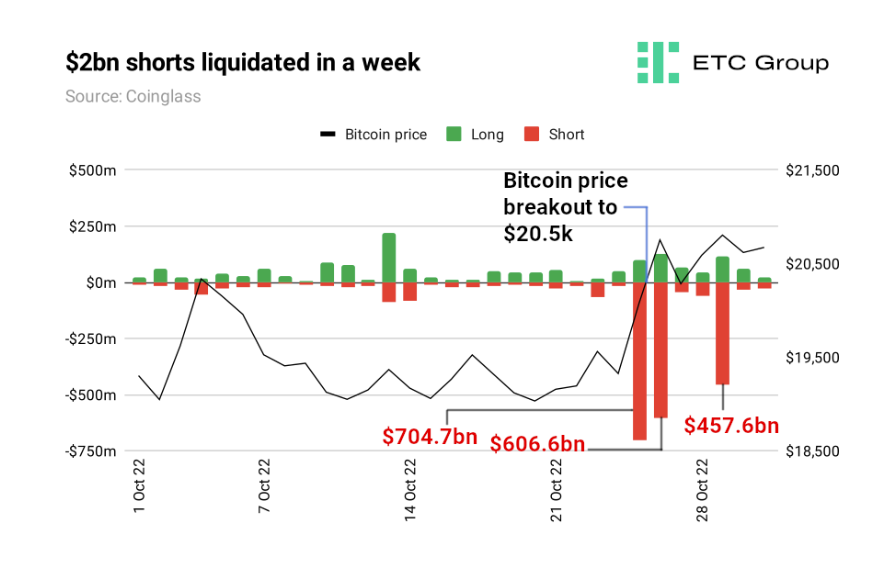

Blankade positioner om 190 miljoner korta positioner kan tyckas vara mycket, men det är en bråkdel av de nivåer vi såg i slutet av förra året. För jämförelse, titta på de sista dagarna av oktober 2022, när blankarnas återköp skickade Bitcoin till kanten av närmare 21 000 USD och Ethereum steg med 25 procent.

Mellan 26 oktober och 31 oktober likviderades två miljarder dollar i handlarpositioner som satsade på att priset på krypto skulle falla. De inträffade i tre stora korta likvidationshändelser med belåning på mer än 450 miljoner dollar på en dag.

Källa: ETC Group, oktober 2022.

Så nu flyttar mindre blankarnas återköp marknader när Bitcoin närmar sig nyckelnivån för realiserat pris som skulle markera en indikation på närmar sig slutet av Crypto Winter.

Tidigare kryptovintrar – så kallade för att de inte nödvändigtvis sammanfaller med nedgångar på aktiemarknaden – har kännetecknats av långa perioder med låg prisvolatilitet, oförändrade eller begränsade handelsvolymer, baisseartade prisåtgärder och stora nedgångar från rekordpriser.

Uppbackad av makro

Den amerikanska inflationen svalnade något i januari, vilket markerade den sjunde fallande månaden i rad, enligt data som träffade marknaderna onsdagen den 15 februari.

Precis som kryptomarknaderna såg ut som om de skulle falla under det psykologiskt viktiga marknadsvärdet på 1 biljon dollar, satte detta till bränsle till elden från investerare vars oro över inflationen minskar.

Det har också stötts av färska IMF-data som visar ”förvånansvärt stark” efterfrågan, BNP och tillväxt i Nordamerika och Europa, och prognoser som höjer globala tillväxtprognoser, detta innebär bättre utsikter för fallande räntor under hela året, och en bättre miljö för risker tillgångar som krypto och aktier.

IMFs ekonomer har höjt sin prognos för global tillväxt i år med 0,2 procentenheter, och förväntar sig att den globala ekonomin kommer att växa med 2,9 procent 2023 och sedan med 3,1 procent 2024.

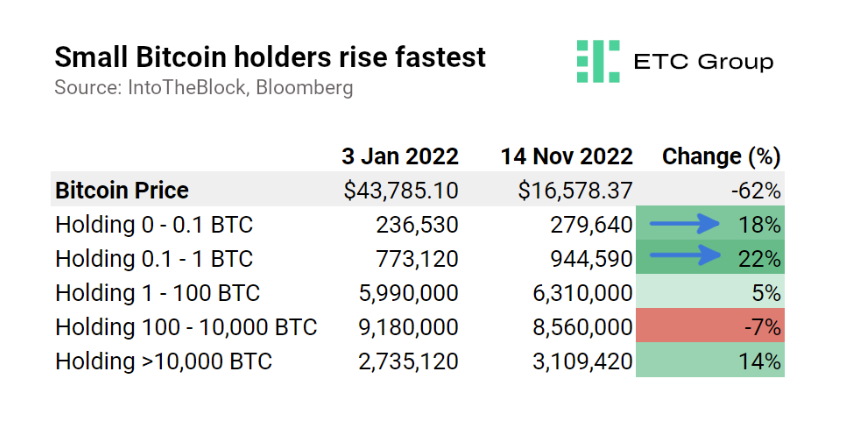

2022 var en hotfull innehavsperiod för Bitcoin-investerare. Nätverksdata visar ändå att antalet småinnehavare exploderade snabbast till alla tiders högsta nivåer under den FTX-inducerade nedgången i november 2022 till ett Bitcoin-pris på 16 578,37 USD.

Antalet mindre investerare, de som har plånböcker som rymmer upp till 0,1 BTC, klättrade rejält mellan januari 2022 och slutet av förra året, trots att priset på Bitcoin föll med 70 procent.

Källa: ETC Group

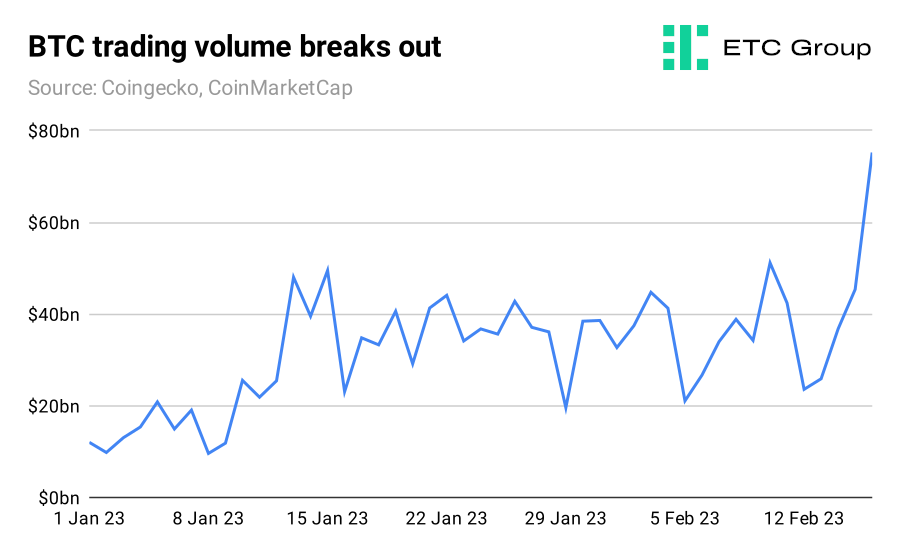

Innehavare – eller HODLers, om du föredrar det – har aldrig hållit så hårt fast vid sin föredragna tillgång. Ett av de andra sätten det går att kategorisera marknadssentiment är att följa hur många affärer (mätt under en 24-timmarsperiod, ofta kallad ”volym”) användare gör med Bitcoin.

I djupet av kryptos marknadskrasch rasade den dagliga handelsvolymen. Även mitt i årsskiftets optimism sjönk 24-timmarshandelsvolymen den 8 januari under 10 miljarder dollar för första gången på över två år.

Källa: ETC Group

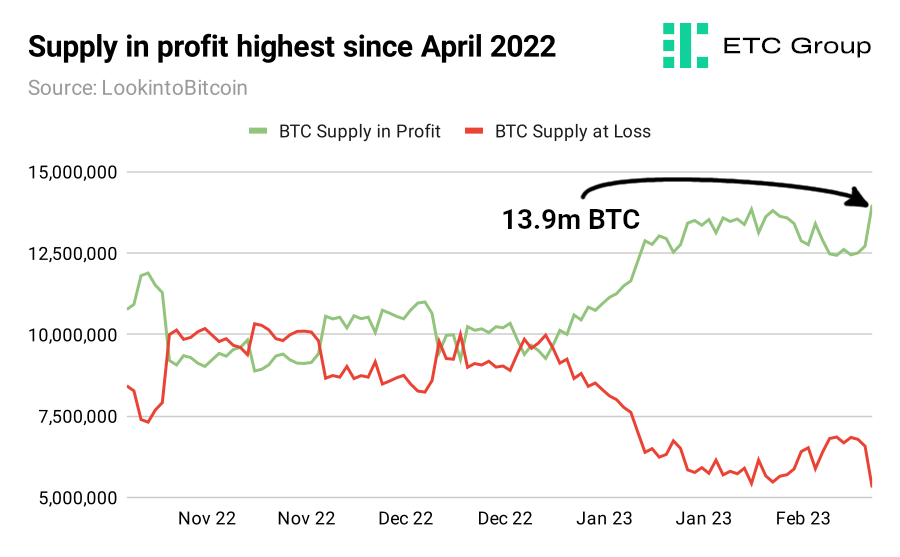

Ett annat nyckelmått att titta på för att se det övergripande tillståndet på marknaden är att titta på antalet Bitcoin-innehavare som säljer mynt med vinst, jämfört med de som säljer med förlust. Den första positionen är positiv, eftersom handlare tjänar pengar och är mer benägna att återvända till marknaden. Det motsatta är också sant.

Källa: ETC Group

Med 13,9 miljoner BTC nu i vinst, jämfört med 5,8 miljoner BTC med förlust, är detta ett högvattenmärke som inte setts sedan april 2022.

Kryptomarknadsanalysanalytiker som de på ETC Group tittar på data i kedjan för att hitta mönster. ETC Group gör det genom att titta på hela historien för de öppet tillgängliga datapunkter som blockkedjor producerar, och sedan utföra beräkningar för att hitta medelvärden och trender.

När Bitcoin är undervärderat vet marknaden.

Börja med Bitcoins

Här har du en guide vad Bitcoins är. På CryptorRunner.com finns det mycket information hur du gör för att börja med bitcoin och kryptovalutor.”

Hur investerar jag i multi-asset ETFer med flera tillgångar?

HDBA ETF investerar i hållbara obligationer

Berkshire Hathaways senaste 13F är ute – Här är vad Buffett har köpt och sålt

US4D ETF spårar amerikanska mid cap företag

HANetfs VD kommenterar Trump-Putin-toppmötet

Vilken ETF för Europas försvarsindustri är bäst?

8 nya IncomeShares ETPer kommer till Tyskland

De bästa ETFerna för att investera i artificiell intelligens (AI)

ETFer som ger exponering mot börsintroduktioner

De börshandlade fonderna som lockade mest i sommarvärmen

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanVilken ETF för Europas försvarsindustri är bäst?

-

Nyheter4 veckor sedan

Nyheter4 veckor sedan8 nya IncomeShares ETPer kommer till Tyskland

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanDe bästa ETFerna för att investera i artificiell intelligens (AI)

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanETFer som ger exponering mot börsintroduktioner

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanDe börshandlade fonderna som lockade mest i sommarvärmen

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanFastställd utdelning i MONTDIV juli 2025

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanMånadsutdelande ETFer uppdaterad med två börshandlade fonder från AXA

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanAXA noterar två kortfristiga ränte-ETFer på Xetra