Nyheter

Time to increase allocation into emerging market equities

ETF Securities Asset Allocation Research – Time to increase allocation into emerging market equities

Summary

• Until recently developed market (DM) equities have been favoured over emerging market (EM) equities due to concerns over the slowdown of the Chinese economy.

• However, EM economies are recovering, investment flows are returning to emerging countries and EM equities are currently very cheap on absolute and relative values.

• Using the US dollar as a trading signal is a simple way to allocate between DM and EM equities and enhances the portfolio risk/return profile by increasing return.

Emerging market economy to rebound

The slowdown in EM equities has been driven by a combination of factors including the economic slowdown of its main constituent China, as the country is making its transition from an industry-driven economy into a service-driven economy and the slump in oil prices which affected many emerging countries such as Saudi Arabia.

Manufacturing PMIs for both DM and EM countries have been declining since early 2014. While DM PMIs remained above the 50 mark, EM PMIs fell below the 50 mark in August 2015 according to our calculations, before recovering last month.

(click to enlarge) Source: ETF Securities, Bloomberg

According to the Institute of International Finance (IIF), the year-over-year growth in foreign investment inflows into emerging countries has also been declining since May 2013 to become outflows in January and February 2016. According to market participants, EM companies have been through a period of deleveraging, repaying their foreign debt and refinancing them into local currencies. If this is the case, EM companies are getting healthier, setting the base for a potentially strong recovery. Total investment flows recovered for the first time last month, up US$3.4bn year-over-year, after 13 months of continuous decline.

(click to enlarge) Source: Institute of International Finance, ETF Securities, Bloomberg

Emerging market equities at a bargain

Our valuation analysis of DM and EM equities shows that EM equities are currently very cheap compared to DM equities as the relative, cyclically adjusted price to earnings (CAPE) currently stands at 35% below its 11 years median of 0.72.

(click to enlarge) *MSCI World index as proxy for DM equities and MSCI EM index as proxy for EM equities. Source: ETF Securities, Bloomberg

EM/DM relative CAPE has been declining since mid-2013 as EM CAPE has been falling 33% while DM CAPE has been quite flat over the same period. EM CAPE is 44% below its 11 years median, indicating that EM equities are also cheap in absolute value.

We use the MSCI world index as a proxy for DM equities and the MSCI EM index as a proxy for EM equities. While EM equities are more volatile than DM equities, EM equities have outperformed DM equities by an annualised 53% since 1988. The largest component for the EM index is China and the largest component for the DM index is the US, both accounting for 39% of their respective index.

Using USD to increase equity returns

As the benchmark currency for international trades, the US dollar (USD) is one of the key drivers of equity performance. Following the financial crisis, very accommodative monetary policy from the Fed weighed on the USD until the second half of 2014. Between the summer 2014 and the end of 2015, the USD surged 25% as the Fed reduced quantitative easing. EM equities, on the other hand, fell 23% over the same period.

In 2015, strong signs of US economic recovery led the Fed to initiate a rate tightening cycle, with the first rate hike in December last year. After a pause in the tightening cycle, we believe that the USD will appreciate as markets anticipate forthcoming rate increases but then it will depreciate again as rate hikes materialise. EM equities tend to perform well during periods of weak USD and vice-versa.

One simple and rational way to implement a relative trade strategy between EM and DM equities is to use the USD as a trading signal. In our strategy, we are using the dollar basket index (DXY) as a proxy for the USD. It measures the value of the USD against a basket of DM currencies. While the Fed’s trade-weighted USD index benchmarks the USD against a broader basket of currencies including EM currencies, we decided to use the DXY because of its stronger correlation with DM/EM relative performance.

(click to enlarge) *DXY Index as a proxy for the US dollar. Source: ETF Securities, Bloomberg

Our strategy is a momentum strategy which consists of buying DM equities when the USD has strengthened by more than 1.5% over the past 6 months and then shifting to EM equities when the USD has weakened by more than -1.5% over the past 6 months. As a result, the investment decision is not dependent on forecast data but only based on actual USD or DXY index historical returns over the past 6 months.

(click to enlarge) Source: ETF Securities, Bloomberg

Exposed to equity only, our portfolio does very little to reduce volatility, at 16.6% compared to 14.7% for the MSCI AC World, our benchmark. However, the strategy still enhances the portfolio Sharpe ratio to 0.40 from 0.08 by increasing returns by 122% compared to the MSCI AC World index.

The portfolio also outperformed both DM and EM equities on an annual basis over the same period by 119% and 43% respectively while being less volatile than EM equities. In addition, the transaction cost is expected to be very low as the number of transactions in the simulated portfolio stands at around two transactions per year on average.

(click to enlarge) *Based on daily data in USD from December 30, 1988 to March 31, 2016. Volatility and returns are annualised. Max drawdown defines as the maximum loss from a peak to a trough based on a portfolio past performance. Max recovery is the length of time in number of years to recover from the trough to previous peak. Risk free rate equals to 3.2% (Cash – a simulated combination of the IMF UK Deposit Rate and the Libor 1Yr cash yield). Source: ETF Securities, Bloomberg

After three years of negative performance, emerging markets are starting 2016 on a positive note, posting a solid 5.4% return during the first quarter of 2016 while DM equities were down – 1%. EM manufacturing PMIs for March have returned above the 50 mark indicating that emerging economies are recovering. Capital flows into EM are increasing again and our valuation analysis shows that EM equities are currently at a bargain, indicating that it is an opportune time to gain exposure or increase exposure to EM equities. With EM growth highly correlated to the USD, using the currency as a trading signal enables investors to increase their portfolio return and improve its Sharpe ratio by shifting exposure between DM and EM equities at a low implementation cost.

Important Information

General

This communication has been issued and approved for the purpose of section 21 of the Financial Services and Markets Act 2000 by ETF Securities (UK) Limited (“ETFS UK”) which is authorised and regulated by the United Kingdom Financial Conduct Authority (the “FCA”).

Amid soaring US debt and Gold’s steady gains, Bitcoin has continued to deliver strong returns over the past 15 years. Its scarcity and decentralization make it a hedge that investors can’t ignore, providing new ways to pursue growth, security, and opportunity in an evolving financial landscape.

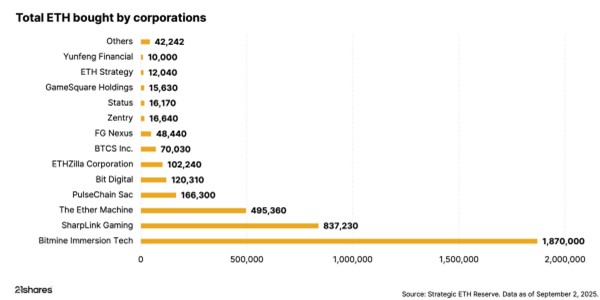

Investors can’t ignore the corporate world’s big bet on Ethereum

Ethereum is stealing the spotlight, as public companies have accumulated over 4.4 million ETH, worth nearly $19 billion, in the past few months. This treasury boom is outpacing Bitcoin’s early adoption and redefining how Wall Street approaches digital assets.

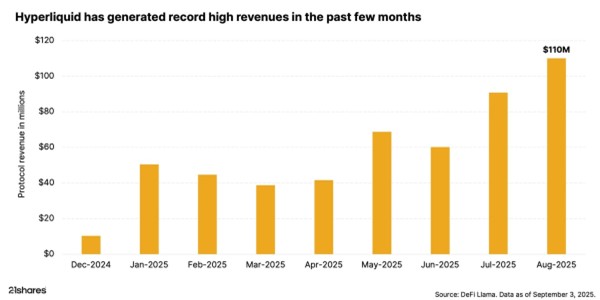

The rise of Hyperliquid: DeFi’s record-breaking powerhouse

Hyperliquid is making waves in DeFi perpetuals by setting new records, leading trading volumes, and propelling its token to all-time highs. Backed by market volatility, high-performance infrastructure, and concentrated liquidity, the platform continues to draw investors and assert its market dominance.

Research Newsletter

Each week the 21Shares Research team will publish our data-driven insights into the crypto asset world through this newsletter. Please direct any comments, questions, and words of feedback to research@21shares.com

Disclaimer

The information provided does not constitute a prospectus or other offering material and does not contain or constitute an offer to sell or a solicitation of any offer to buy securities in any jurisdiction. Some of the information published herein may contain forward-looking statements. Readers are cautioned that any such forward-looking statements are not guarantees of future performance and involve risks and uncertainties and that actual results may differ materially from those in the forward-looking statements as a result of various factors. The information contained herein may not be considered as economic, legal, tax or other advice and users are cautioned to base investment decisions or other decisions solely on the content hereof.

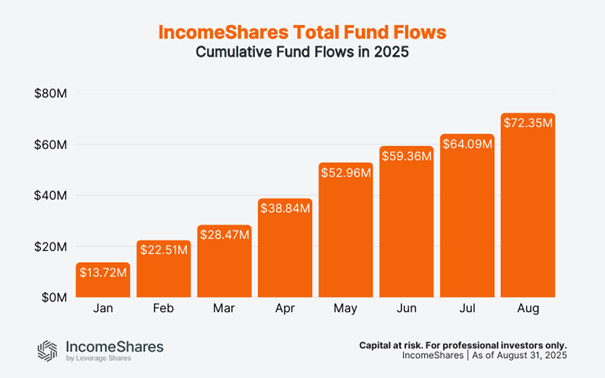

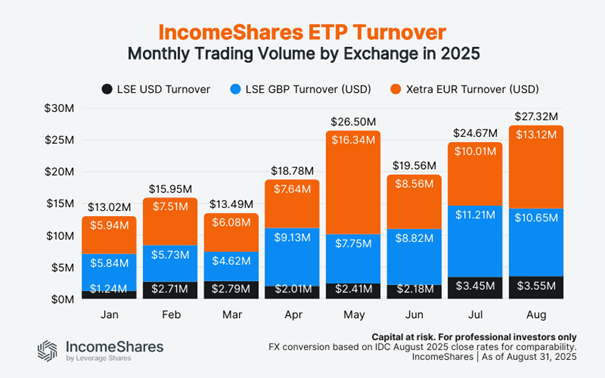

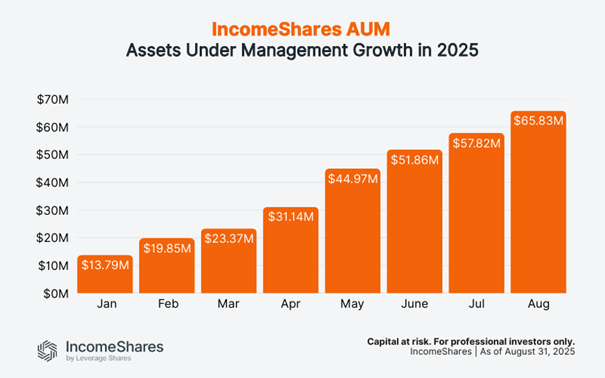

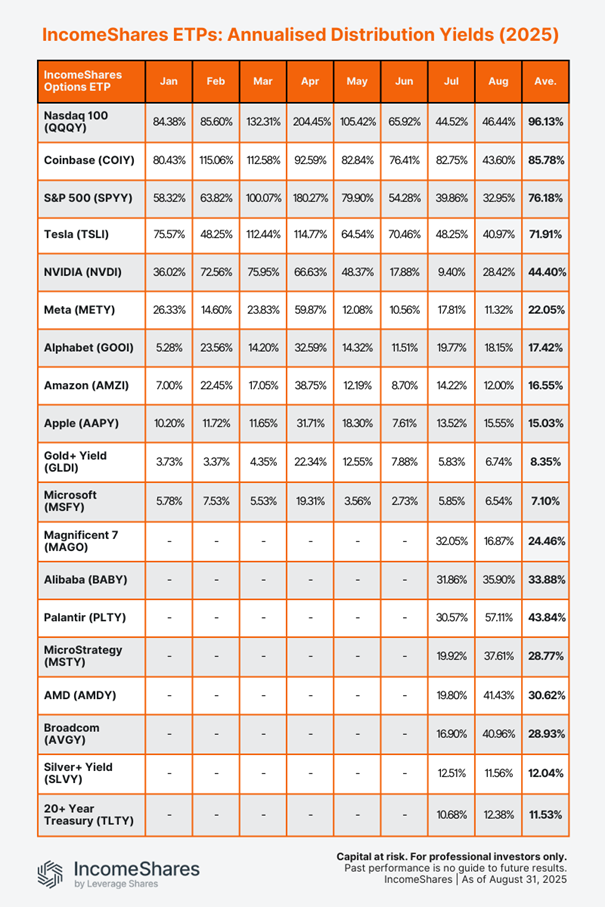

IncomeShares passed three milestones in August. Assets under management climbed to almost $66 million, cumulative fund flows topped $72 million, and turnover across London and Xetra listings reached over $27 million. Palantir paid the highest annualised distribution yield at 57.11%. The sections below break the numbers down in more detail.

Cumulative fund flows

Fund flows track how much money investors put into or take out of IncomeShares ETPs (exchange-traded products). Positive flows mean more money coming in than going out – a sign of demand for the products.

Flows have risen every month this year. In January, they stood at $13.7 million. By the end of August, they reached $72.4 million. That’s over $8 million of new money added in August alone – the biggest increase since May.

Trading turnover

Turnover is the total dollar value of IncomeShares ETPs bought and sold on the exchanges. Higher turnover means more activity and liquidity for investors.

Turnover reached $27.3 million in August – the highest on record and more than double January’s $13.0 million. London listings (USD and GBP combined) made up $14.2 million, with Xetra listings close behind at $13.1 million. Both exchanges have seen steady increases through 2025, showing rising interest in income options strategies across the board.

Note: Figures use IDC FX rates as of the August month-end to convert GBP and EUR into USD. We apply the same August rates to all prior months to compare turnover on a like-for-like basis.

Assets under management (AUM)

AUM is the total value of assets held across all IncomeShares ETPs. It grows when new investors buy in, or when the underlying assets rise in value.

AUM grew from $13.8 million in January to $65.8 million at the end of August. It was also $8 million more than in July. Steady inflows and consistent income distributions are helping the product range build scale.

Distribution yields

Distribution yields represent the annualised income paid to investors as a percentage of the current NAV (net asset value), based on the latest month’s yield. IncomeShares ETPs aim to generate this income from selling options. Yields change each month depending on strategy performance and market volatility.

Annualised August yields (ranked highest to lowest):

• Palantir Options ETP (PLTY): 57.11%

• Nasdaq 100 Options ETP (QQQY): 46.44%

• Coinbase Options ETP (COIY): 43.60%

• AMD Options ETP (AMDY): 41.43%

• Tesla Options ETP (TSLI): 40.97%

• Broadcom Options ETP (AVGY): 40.96%

• MicroStrategy Options ETP (MSTY): 37.61%

• Alibaba Options ETP (BABY): 35.90%

• S&P 500 Options ETP (SPYY): 32.95%

• NVIDIA Options ETP (NVDI): 28.42%

• Alphabet Options ETP (GOOI): 18.15%

• Magnificent 7 Options ETP (MAGO): 16.87%

• Apple Options ETP (AAPPY): 15.55%

• 20+ Year Treasury Options ETP (TLTY): 12.38%

• Amazon Options ETP (AMZI): 12.00%

• Silver+ Yield Options ETP (SLVY): 11.56%

• Meta Options ETP (METY): 11.32%

• Gold+ Yield Options ETP (GLDI): 6.74%

• Microsoft Options ETP (MSFY): 6.54%

Our Palantir ETP topped the list with an annualised yield of 57.11% for August, up from 30.57% in July. The stock was volatile in August, trading between $142 and $190. That wider range increased option premiums, which boosted the ETP’s yield. The ETP sells put options on Palantir stock and holds shares – the strategy used for all our single stock ETPs and the Magnificent 7 product.

The Nasdaq 100 ETP paid an annualised yield of 46.44% in August, up slightly from 44.52% in July. At the other end, Gold+ and Microsoft stayed below 7%, reflecting relatively calmer conditions in their underlying assets.

The table below shows the annalised distribution yields for all IncomeShares ETPs so far this year. Note that the bottom eight ETPs launched in late June, so they only have yields for July and August.

Key takeaways

• Fund flows climbed to $72.4 million, with August adding more than $8 million.

• Turnover hit a record $27.3 million, split almost evenly between London and Xetra.

• Palantir topped the yield table at 57%, with Nasdaq 100 and Coinbase also paying above 40%.

Concerned about rising government debt? Bitcoin’s got you covered

N100 ETF följer det amerikanska Nasdaq 100 indexet

IncomeShares Monthly Investor Update – August 2025

CHSJ ETF investerar i CLO-obligationer

HYPE ETP ger exponering mot Hyperliquid

VALOUR ARB SEK spårar priset på kryptovalutan Arbitrum

Månadsutdelande ETFer uppdaterad med IncomeShares produkter

Utdelningar och försvarsfonder lockade i augusti

HANetfs analyserar hur ett fredsavtal kan påverka det europeiska försvaret

De bästa innovations-ETFerna

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanVALOUR ARB SEK spårar priset på kryptovalutan Arbitrum

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanMånadsutdelande ETFer uppdaterad med IncomeShares produkter

-

Nyheter1 vecka sedan

Nyheter1 vecka sedanUtdelningar och försvarsfonder lockade i augusti

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanHANetfs analyserar hur ett fredsavtal kan påverka det europeiska försvaret

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanDe bästa innovations-ETFerna

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanHANetfs VD kommenterar Trump-Putin-toppmötet

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanADLT ETF investerar bara i riktigt långa amerikanska statsobligationer

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanIncomeShares når 60 miljoner dollar i förvaltat kapital – Tillväxtöversikt 2025