Nyheter

Commodity volatility expected

ETF Securities Commodities Research: Commodity volatility expected as China liberalises financial markets

Commodity volatility expected as China liberalises financial markets

Summary

China is both one of the largest producers and consumers of most commodities. Yet financial centres in the UK and US are responsible for setting global prices for many commodities.

China seeks to expand its role in the intermediation and price setting of global commodities. However a key hurdle is currency restrictions and capitals controls.

While timing of any currency and capital market reform is unclear, dismantling these restrictions could unwind large carry-trades that use commodities as collateral, introducing a new source of volatility to the asset class.

China and commodity demand

China’s role in the upward phase of the commodity supercycle remains largely undisputed: resource-intensive economic growth, led by urbanisation, industrialisation, and a growth in global trade between the mid-1990s and the financial crisis in 2008 drove demand for commodities higher. With supply unable to keep up with demand, prices rose substantially higher. Although more volatile, commodities prices have a fairly strong correlation to China’s GDP growth.

China’s commodity futures markets

Futures markets are an integral part of the global financial market infrastructure, as they allow both consumers and producers of commodities to hedge. Hedgers are typically on the short side of futures markets and thus need to offer positive risk premia to attract speculators on the long side.i By bringing a large number of financial investors to the long side, financialisation of commodities mitigates this hedging pressure and improves risk sharing.

Although China is the largest consumer of commodities, its development of a futures market in commodities only took place after the onset of the commodity supercycle (and many commodities have been added in the downward phase of the cycle). The Shanghai Futures Exchange (SHFE) started trading copper and aluminium in 1999 and added zinc (2007), gold (2008), nickel (2014).

The volume of gold and copper traded on the SHFE has been rising, highlighting the traction that the market for these metals has been gaining in China.

Global ambitions require currency policy change

China seeks to play a larger role in the intermediation of commodities internationally. It recognises it is the largest consumer and producer of many commodities, yet relies on financial centres outside of China for the setting of prices. Fang Xinghai, vice chairman of the China Securities Regulatory Commission, said at the SHFE’s annual conference in May 2016 “We’re facing a chance of a lifetime to become a global pricing center for commodities”. Due to currency restrictions, trading in raw materials is largely off-limits to overseas investors. However, that is an issue that China has long pledged to change. Any change in currency policy will likely be a strong catalyst for the growth of China’s commodity futures market.

Distortions in Chinese commodities…

Closed capital markets and currency restrictions have led to some unusual practices in China. China’s interest rate is higher than many other countries (especially developed market interest rates which in some cases are below zero). If Chinese investors were able to borrow in foreign currencies they could engage in a typical carry trade and arbitrage from the rate differential (subject to currency market moves). However, capital restrictions which stop domestic investors accessing foreign loans and exchange rate management violate the so called ‘covered interest rate parity’.

However a loophole exists. In order to make Chinese manufacturers more profitable, the authorities allow them to use work in process inventory such as copper, tin, aluminium (or even finished inventory) as collateral for loans. A manufacturer can go to a local bank and ask to borrow in US dollars or euros or yen etc. at low interest rates using commodity as collateral. The funds will be delivered to the manufacturer in Yuan and can be deposited at high interest rates. The local bank would verify to the People’s Bank of China (PBoC, the central bank) that the collateral is sitting in a warehouse (i.e. is bonded) and the PBoC will use an offshore entity to borrow the funds (which it will then pass to the local bank).The existence of the facility could be artificially inflating demand for commodity imports into China.

The risk with opening up currency markets therefore is that this carry trade could fall away and unlock a substantial amount of commodities tied up in bonded warehouses to industrial usage.

It is estimated that in 2014 about US$109 billion foreign exchange loans in China were backed by commodities as collateral, equivalent to 31% of China’s short-term FX loans and 14% of China’s total FX loans.ii In 2014, China imported US$1.7 trillion of commodities. The estimated amount of financing therefore represents about 6% of imports. In the worst case scenario if all those commodities were to unwind (a scenario we don’t believe will occur), there could be a 6% supply shock, which would be price negative. A collateral unwind of a smaller magnitude, we believe will still lead to commodity price volatility.

Copper is probably most at risk. Close to half of current copper demand in China could be from the copper carry trade.

…including gold

A similar trade exists in gold. Imported gold is being used via gold loans and letters of credit to raise low cost funds for business investment and speculation. Financial liberalisation could also see these trades unwind.

In 1950 China had prohibited private ownership of bullion and put the gold industry under state control. With the creation of the Shanghai Gold Exchange (SGE) in 2002, formal prohibition on gold bullion was lifted in 2004. China has embraced this relatively new opportunity to own gold, with the country overtaking India as the largest consumer gold coins and bars. Despite the cultural affinity to buy and store gold, those stocks can be monetised. Gold leasing i.e. the ability for banks to loan out gold has seen rapid growth. Gold can also be used as collateral for borrowing from banks as long as it meets the SGE criteria. Once again this collateral-based lending could fall away if access to unsecured loans is improved.

We expect any movement to a freer currency and open capital markets to be gradual. But that transition could introduce volatility to global commodity prices as collateral carry trades in China unwind.

i Keynes (1923), Hicks (1939), Hirshleiffer (1988)

ii “Commodities as Collateral” in forthcoming Review of Financial Studies by Ke Tang (Tsingua University) and Haoxiang Zhu (MIT Sloan School of Management), April 2016

Important Information

General

This communication has been issued and approved for the purpose of section 21 of the Financial Services and Markets Act 2000 by ETF Securities (UK) Limited (“ETFS UK”) which is authorised and regulated by the United Kingdom Financial Conduct Authority (the “FCA”).

The information contained in this communication is for your general information only and is neither an offer for sale nor a solicitation of an offer to buy securities. This communication should not be used as the basis for any investment decision. Historical performance is not an indication of future performance and any investments may go down in value.

Nyheter

HANetf och Infrastructure Capital Advisors samarbetar för att lansera aktivt förvaltad preferensavkastnings-ETF i Europa

{kind=link}

{kind=link}

{kind=link}

HANetf och Infrastructure Capital Advisors samarbetar för att lansera aktivt förvaltad preferensavkastnings-ETF i Europa

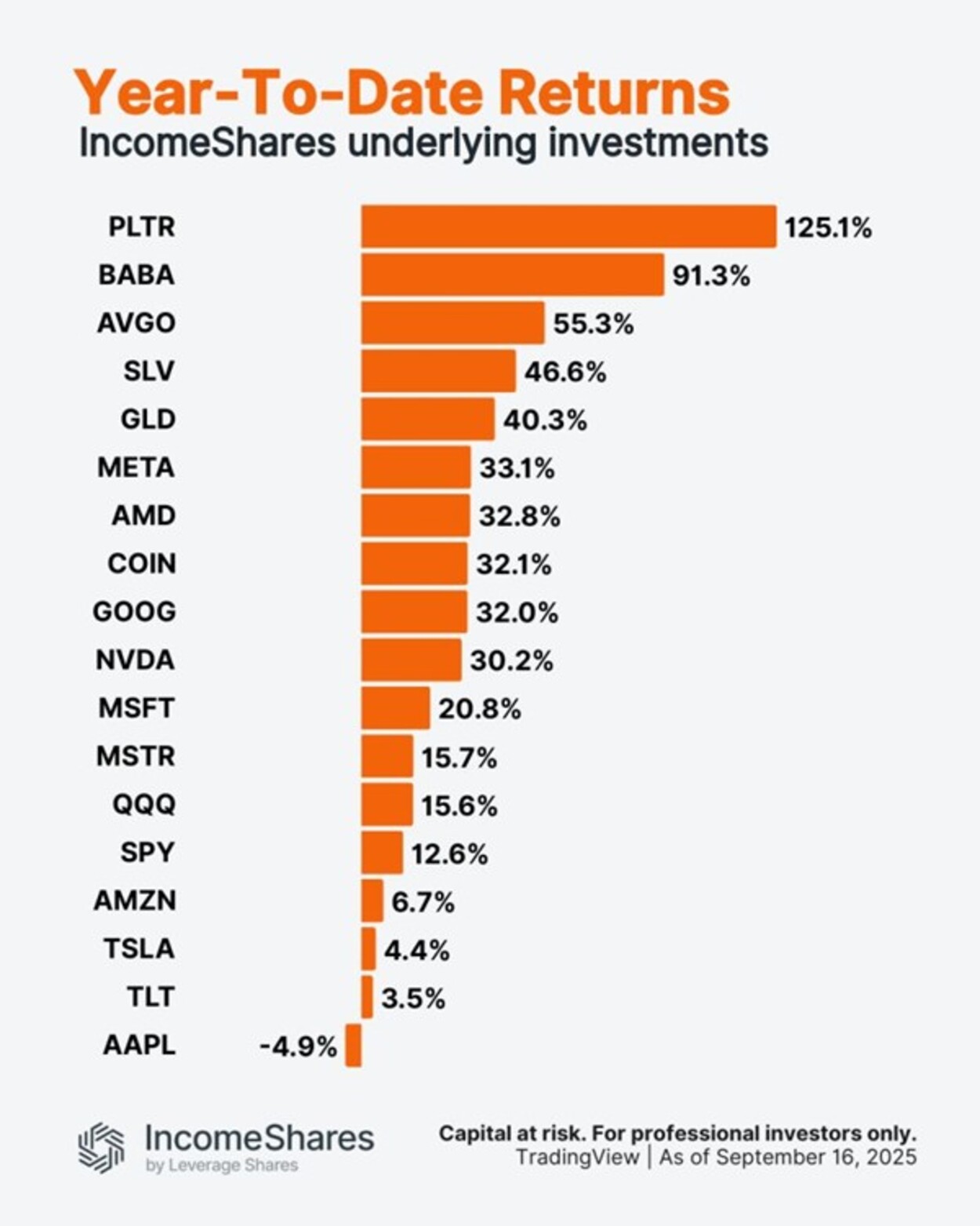

Palantir är upp 125 % i år. Apple är ner 5 %.

Utforska framtiden för AI och DeFi

ONCC ETP spårar den schweiziska dagslåneräntan

HANetf kommenterar kopparuppgången

Utdelningar och försvarsfonder lockade i augusti

Månadsutdelande ETFer uppdaterad med IncomeShares produkter

HANetfs analyserar hur ett fredsavtal kan påverka det europeiska försvaret

ADLT ETF investerar bara i riktigt långa amerikanska statsobligationer

Septembers utdelning i XACT Norden Högutdelande

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanUtdelningar och försvarsfonder lockade i augusti

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanMånadsutdelande ETFer uppdaterad med IncomeShares produkter

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanHANetfs analyserar hur ett fredsavtal kan påverka det europeiska försvaret

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanADLT ETF investerar bara i riktigt långa amerikanska statsobligationer

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanSeptembers utdelning i XACT Norden Högutdelande

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanFastställd utdelning i MONTDIV augusti 2025

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanHANetf kommenterar mötet mellan Kina, Ryssland och Nordkorea vid militärparad

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanAICT ETF investerar i obligationer utgivna av företag från tillväxtmarknader