Nyheter

3 Rules for Investing in Leveraged ETFs

Nyheter4 timmar sedan

ETF-special med Peter Lidblom

Nyheter5 timmar sedan

HANetf kommenterar om ryska drönare som tar sig in i polskt luftrum

Nyheter6 timmar sedan

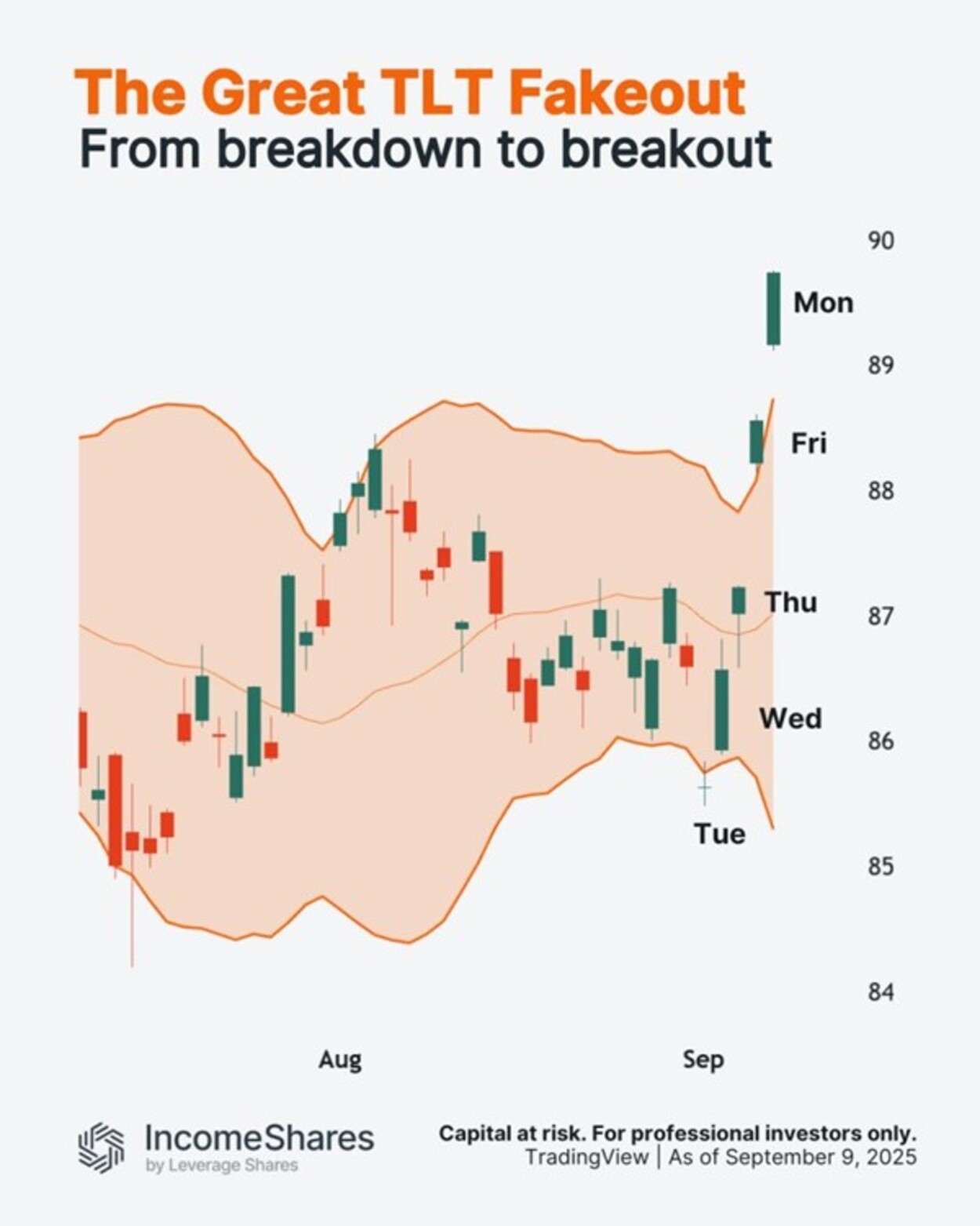

Den stora TLT-”fakeouten” – från sammanbrott till utbrott.

Nyheter7 timmar sedan

EMGM ETF är en satsning på emerging markets

Nyheter8 timmar sedan

Indo-Pac Defence ETF: Vart nästa utgiftscykel är på väg

Nyheter2 veckor sedan

Månadsutdelande ETFer uppdaterad med IncomeShares produkter

Nyheter1 vecka sedan

Utdelningar och försvarsfonder lockade i augusti

Nyheter4 veckor sedan

VALOUR ARB SEK spårar priset på kryptovalutan Arbitrum

Nyheter3 veckor sedan

HANetfs analyserar hur ett fredsavtal kan påverka det europeiska försvaret

Nyheter4 veckor sedan

HANetfs VD kommenterar Trump-Putin-toppmötet

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanMånadsutdelande ETFer uppdaterad med IncomeShares produkter

-

Nyheter1 vecka sedan

Nyheter1 vecka sedanUtdelningar och försvarsfonder lockade i augusti

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanVALOUR ARB SEK spårar priset på kryptovalutan Arbitrum

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanHANetfs analyserar hur ett fredsavtal kan påverka det europeiska försvaret

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanHANetfs VD kommenterar Trump-Putin-toppmötet

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanADLT ETF investerar bara i riktigt långa amerikanska statsobligationer

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanIncomeShares når 60 miljoner dollar i förvaltat kapital – Tillväxtöversikt 2025

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanFastställd utdelning i MONTDIV augusti 2025