Nyheter

Gold Shines as a Safe Haven in January

Van Eck Global’s gold specialist Joe Foster shares his monthly perspective on the gold market, this one is named Gold Shines as a Safe Haven in January

» Open Gold Market Commentary

Gold Shines as a Safe Haven in January

Gold Market Commentary

By: Joe Foster, Gold Strategist

Market Review

Please note that the information herein represents the opinion of the author and these opinions may change at any time and from time to time.

It has been a very eventful start to the year. On January 4, the first trading day of 2016, the Chinese equity market fell drastically, with the Shanghai Composite Stock Index2 down 6.9% during the session. The equity slide continued, repeatedly triggering the recently instituted circuit breakers, which have subsequently been suspended. The Shanghai Composite Stock Index ended the month of January down 22.6%. The Chinese selloff spread to global equity markets with the S&P 500® Index3 having one of its worse starts to any year, falling almost 9% three weeks into January. By month end, however, the Index had recouped some losses to end January down 5%. The MSCI All-Country World Index4, which includes both emerging and developed world equity markets, fell 8% during the month. Commodities also took a hit, with oil and copper down 9% and 3%, respectively. Even the Japanese yen ended the month weaker, down 0.8% relative to the U.S. dollar, after the Bank of Japan (BOJ) surprisingly announced on January 29 its adoption of negative interest rates, which drove the yen down 2% that day.

Except for a stronger than expected employment report, most major U.S. economic data released during the month was disappointing, including the Empire State Manufacturing Index5, retail sales ex-autos, industrial output growth, capacity utilization, durable goods orders, pending December home sales, and Q4 2015 real GDP growth. It was no surprise that the Federal Reserve (Fed) left rates unchanged on January 27, but revised messaging in the Fed’s statement raised many questions in the market. The Fed softened its assessment of its growth and inflation outlooks, and indicated that it is “closely monitoring” global economic and financial developments, signaling that it is uncertain about their potential impact on the U.S. economy. Consequently market expectations for the Fed’s next rate hike have been delayed to November, with less than one full 25 bps hike priced in for 2016. We have been saying that, in our opinion, there is a good possibility that the Fed will not be as aggressive as previous guidance suggests, and that the U.S. economy is vulnerable, making rising rates a significant impediment in 2016. It appears that the market and even the Fed are increasingly adopting a similar view for 2016.

The U.S. dollar held up during January, with the U.S. Dollar Index6 (DXY) down slightly before the BOJ’s announcement on January 29, but rising later in the day to finish the month with a 1% gain. Gold bullion was, however, the true winner in January The gold price not only managed to gain in a month when the U.S. dollar also finished higher, but it outperformed significantly, benefiting from its safe haven7 status to close at $1,118.17 per ounce, a gain of $56.75 per ounce or 5.35%. Notably, holdings of global gold bullion exchange-traded products (ETPs) rose by 1.8 million ounces or 3.8% during January.

The World Gold Council published its latest World Official Gold Reserves for 2015. The figures rank China (1,762 tonnes, representing 1.7% of total foreign reserves) and Russia (1,393 tonnes, 13%), respectively, as the sixth and seventh largest holders of gold reserves in the world, behind the U.S., Germany, the International Monetary Fund (IMF), Italy, and France. The central banks of China and Russia were both significant buyers of gold in 2015. After announcing its updated gold holdings in June 2015, the People’s Bank of China (PBOC) purchased an additional 104 tonnes of gold in the six months from July to December. This equates to an annualized rate of purchase exceeding 200 tonnes of gold, which is double the average annual rate estimated from the PBOC’s June 2015 update. This suggests China may be stepping up its gold reserves purchases. Russia’s net purchases were estimated at about 185 tonnes of gold in 2015 (not including data for December), representing an increase of about 15% from 2014.

In its latest report Thomson Reuters GFMS Gold Survey estimates that in Q4 2015 total gold physical demand increased by 2.2% year over year, driven primarily by strong growth (23.2%) in official sector net purchases (dominated by Russia and China as explained above) and a 7.0% increase in retail investment in gold bars (driven by strong demand from China and India.) While jewelry demand in China dropped by 4%, demand out of India continued to recover, increasing 3% in Q4. The world’s total supply of gold dropped by 7.3% with mine production declining 3.8%.

The performance of gold stocks was mixed in January. The NYSE Arca Gold Miners Index (GDMNTR) gained 3.35%, while Market Vectors Junior Gold Miners Index8 (MVGDXJTR) dropped 0.79%. While the underperformance of gold stocks relative to gold is atypical when the price of gold is on the rise, the end-of-year performance of gold stocks was also somewhat out of character. In December, while gold fell to a new cycle low, gold stocks did not follow to new long-term lows, and in fact, the GDMNTR Index and the MVGDXJTR Index advanced 0.9% and 2.8%, respectively. Perhaps the reversal of that uncharacteristic December outperformance helps explains some of the underperformance in January, along with general weakness in the broader equity market that can also drag down gold equities.

Additional factors affected gold stocks and likely contributed to negative sentiment towards equities during the month. Some companies reported preliminary operating results for 2015 and provided guidance for 2016. While 2015 results were broadly in-line and costs continued to trend down, 2016 production guidance seems slightly below current expectations. Furthermore, base metals and silver underperformed gold in January, affecting valuations of companies with exposure to those metals. Finally, there was company-specific news that had significant negative impact on share prices, which we didn’t always deem as justified. This news included: Eldorado’s planned suspension of its projects in Greece; a material mineral resource revision of Rubicon’s Phoenix project and its impact on Royal Gold’s stream on that project; and the potential fundraising B2Gold may require, given current gold prices, to finance its Fekola project.

The performance gap between gold bullion and gold equities was widest on January 19. Since then the stocks have materially outperformed, closing the gap. As of February 1, the GDMNTR Index and gold were both up 6.3% year-to-date.

Market Outlook

Financial markets in January helped to remind investors around the globe why perhaps every portfolio should have an allocation to gold. It is our opinion that gold should be used mainly as a portfolio diversifier and as a hedge against tail risk9; a form of portfolio insurance that attempts to preserve value when tail risk becomes a reality. Gold has little correlation to other financial assets (Figure 1 below).

(Click to enlarge)

Figure 1: Correlation of Gold to other asset classes during expan¬sions and contractions since 1987*

*As of December 2015. Expansion and contraction as per the National Bureau of Economic Research (NBER). Source: Bloomberg, NBER, World Gold Council. Historical information is not indicative of future results; current data may differ from data quoted.

When most other investments are performing poorly, gold is expected to do well, and vice versa. Worsening financial conditions, escalating geopolitical turmoil in the Middle East, recurring issues with European sovereign debt, currency issues and slow growth in China, Russian aggression, and failure of Japan and the U.S. to reach their economic potential are all risks that threaten growth and economic development globally. Gold can act as a financial hedge against these risks.

Many investors use gold stocks to gain leveraged exposure to gold, however, we just finished a one-month period during which the expected outperformance of gold stocks relative to gold did not materialize. We do not expect this trend to continue.

As we mentioned, a day after month-end, on February 1, the year-to-date gap between the GDMNTR Index and gold had already closed, and we expect stocks to continue to outperform if the gold price continues to rise. In fact, gold shares should offer their highest leverage to gold when the gold price is close to the cost of production, as is now the case. The leverage comes from earnings leverage; as the gold price increases, the change in a company’s profitability significantly outpaces the change in the gold price. For example, say a gold producer realizes a $200 per ounce margin at current gold prices. At $1,100 gold, a $100 increase in the gold price would increase the producer’s margin by 50%, while representing only about a 9% increase in the gold price. The higher the cost of production, the smaller the margin, and the more leverage companies have to increasing gold prices.

It therefore makes sense that equities should outperform gold during rising gold prices, and underperform if gold falls, unless of course costs are increasing at the same time the gold price is increasing and margins are flat or shrinking. This was the main reason why gold equities underperformed gold in 2011 and 2012, two years during which the gold price increased. Since then positive changes have taken place in the gold mining industry, returning profitability to the sector.

We now see the industry in the best shape it has been in for a long time. Unfortunately, this positive transformation of the sector coincided with, and to some extent was intensified by, a period of falling gold prices. As Figure 2 below indicates, however, equities have consistently demonstrated their effectiveness as leverage plays on rising gold during these past years.

(Click to enlarge)

Source: Bloomberg. Past performance is no guarantee of future results; current performance may be lower or higher than the performance data quoted. Gold equities are represented by NYSE Arca Gold Miners Index (GDMNTR).

by Joe Foster, Portfolio Manager/Strategist

With more than 30 years of gold industry experience, Foster began his gold career as a boots on the ground geologist, evaluating mining exploration and development projects. Foster offers a unique perspective on gold and the precious metals asset class.

Important Information For Foreign Investors

This document does not constitute an offering or invitation to invest or acquire financial instruments. The use of this material is for general information purposes.

Please note that Van Eck Securities Corporation offers actively managed and passively managed investment products that invest in the asset class(es) included in this material. Gold investments can be significantly affected by international economic, monetary and political developments. Gold equities may decline in value due to developments specific to the gold industry, and are subject to interest rate risk and market risk. Investments in foreign securities involve risks related to adverse political and economic developments unique to a country or a region, currency fluctuations or controls, and the possibility of arbitrary action by foreign governments, including the takeover of property without adequate compensation or imposition of prohibitive taxation.

Please note that Joe Foster is the Portfolio Manager of an actively managed gold strategy.

Any indices listed are unmanaged indices and include the reinvestment of all dividends, but do not reflect the payment of transaction costs, advisory fees or expenses that are associated with an investment in the Fund. An index’s performance is not illustrative of the Fund’s performance. Indices are not securities in which investments can be made.

1NYSE Arca Gold Miners Index (GDMNTR) is a modified market capitalization-weighted index comprised of publicly traded companies involved primarily in the mining for gold. 2Market Vectors Junior Gold Miners Index (MVGDXJTR) is a rules-based, modified market capitalization-weighted, float-adjusted index comprised of a global universe of publicly traded small- and medium-capitalization companies that generate at least 50% of their revenues from gold and/or silver mining, hold real property that has the potential to produce at least 50% of the company’s revenue from gold or silver mining when developed, or primarily invest in gold or silver. 3Tail risk is the risk of an asset or portfolio of assets moving more than three standard deviations from its current price. 4S&P 500® Index (S&P 500) consists of 500 widely held common stocks covering industrial, utility, financial, and transportation sectors. 5Dot-com bubble grew out of a combination of the presence of speculative or fad-based investing, the abundance of venture capital funding for startups and the failure of dotcoms to turn a profit. Investors poured money into internet startups during the 1990s in the hope that those companies would one day become profitable, and many investors and venture capitalists abandoned a cautious approach for fear of not being able to cash in on the growing use of the internet. 6Source: Bloomberg.

Please note that the information herein represents the opinion of the author and these opinions may change at any time and from time to time. Not intended to be a forecast of future events, a guarantee of future results or investment advice. Historical performance is not indicative of future results; current data may differ from data quoted. Current market conditions may not continue. Non-Van Eck Global proprietary information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission of Van Eck Global. ©2015 Van Eck Global.

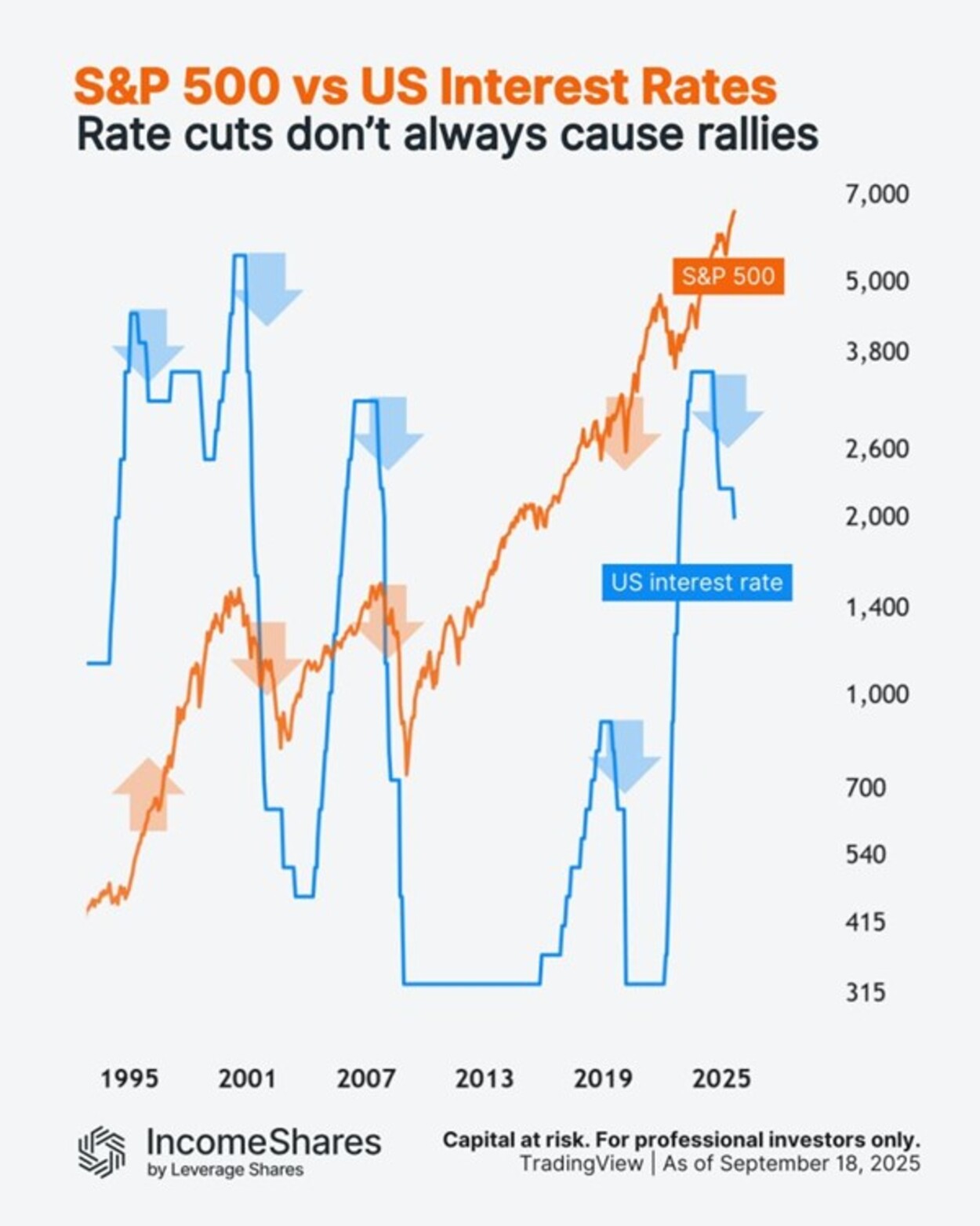

Den amerikanska centralbanken Federal Reserve sänkte räntorna med 0,25 % i veckan– men vad kan det betyda för den amerikanska aktiemarknaden?

Detta diagram följer S&P 500-indexet (orange linje) mot amerikanska räntor (blå linje) sedan 1990-talet.

Här är vad som hände med aktierna de senaste gångerna Fed började sänka räntorna från tidigare ränte”toppar”:

• 1995: aktierna steg (före dotcom-bubblan).

• 2000: aktierna föll (dotcom-bubblan sprack).

• 2007: ytterligare en björnmarknad (före finanskrisen 2008).

• 2019: aktierna steg först (sedan föll de in i Covid-kraschen 2020).

Fyra av fem gånger sammanföll räntesänkningarna med stora nedgångar. Men orsakerna var alltid olika. Korrelation innebär inte kausalitet.

Och nu, 2024/25, befinner vi oss i en ny sänkningscykel. Aktierna sjönk med cirka 20 % i början av 2025, men har sedan dess stigit till nya toppar. Frågan är, vad händer härnäst?

IncomeShares S&P500 Options (0DTE) ETP har exponering mot S&P 500 och säljer dagliga säljoptioner för potentiell inkomst.

Följ IncomeShares EU för marknadsinsikter.

HANetfs VD kommenterar kärnkraftsavtalet mellan Storbritannien och USA

WMSE ETF en global momentumfond som handlas i euro och pund

Federal Reserve sänkte räntorna med 0,25 %

ARAY ETP följer priset på kryptovalutan Raydium

Bellevue lanserar aktiv hälso-ETF på Xetra

Utdelningar och försvarsfonder lockade i augusti

Månadsutdelande ETFer uppdaterad med IncomeShares produkter

HANetfs analyserar hur ett fredsavtal kan påverka det europeiska försvaret

ADLT ETF investerar bara i riktigt långa amerikanska statsobligationer

Septembers utdelning i XACT Norden Högutdelande

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanUtdelningar och försvarsfonder lockade i augusti

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanMånadsutdelande ETFer uppdaterad med IncomeShares produkter

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanHANetfs analyserar hur ett fredsavtal kan påverka det europeiska försvaret

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanADLT ETF investerar bara i riktigt långa amerikanska statsobligationer

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanSeptembers utdelning i XACT Norden Högutdelande

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanFastställd utdelning i MONTDIV augusti 2025

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanHANetf kommenterar mötet mellan Kina, Ryssland och Nordkorea vid militärparad

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanAICT ETF investerar i obligationer utgivna av företag från tillväxtmarknader