Nyheter

What’s in store for the ECB and the Euro

What’s in store for the ECB and the Euro ETF Securities FX Research: A global recession is just hype

Summary

Market dynamics in 2016 indicate that investors fret over the possibility of a global recession. There is little evidence or likelihood of this happening.

Central bank policy is bowing to market pressure to raise stimulus. The same stimulus measures that once had an impact are failing and new ideas are needed.

The Euro appears headed higher as the ECB again disappoints the market.

Not the end of the world

During 2016, share markets have mostly been in freefall, (in line with bond yields), and global asset volatility has surged. Investors appear concerned that the global economy is about to experience a recession. In turn, markets are expecting and most central banks seem willing to provide fresh stimulus to support economic activity. While such actions can produce a short-term impetus for risk appetite, it is unlikely to provide a sustained improvement in the underlying economy. New thinking is needed.

While investors are concerned about another global slowdown, and that market weakness could provide a negative feedback loop to the real economy, there appears little evidence of this occurring. The value of more and more of the same QE and lower and lower rates appears dubious, as does the reality surrounding recession fears. Economic data shows that activity isn’t stellar but it not in recession territory as investors fear.

(Click to enlarge) Source: Bloomberg, ETF Securities

The US and the UK economies remain robust, with good growth rates around 2%, and unemployment back near pre-crisis levels. Swedish Q4 2015 growth rose to the highest level in four years.

Eurozone unemployment remains elevated but has reached the lowest level in four years. Services sector buoyancy is offsetting weakness in manufacturing and overall growth is hovering at 1.5%. Even concern over the European banking sector seems misplaced. Although loan growth is stagnant, margins appear stable and non-performing loans have been falling for around 12 months, down 30% since the March 2014 peak.

Clearly oil exporters like Canada and Norway are struggling and require stimulus. However, other commodity currency countries (Australia and New Zealand) and faring well, with growth rates in the 2-3% range. Japanese growth has been stagnant for many years, despite some evidence of gaining traction. Nonetheless, negative rate environment has not assisted the real economy or kick-started inflationary forces. And the strong currency is hurting the Swiss economy, which is weakening sharply.

Who’s been doing what?

The main policy that G10 central banks have been implementing have been similar: a combination of asset purchases, so called quantitative easing (QE) and lowering interest rates (some into negative territory). While the impact of such policies appear to be losing their potency, policymakers appear to be pandering to market whims and simply responding to rising asset volatility.

Over the past year, six of the G10 central banks have cut rates and three are below zero, and appear ready to do more. At some point, moving rates further negative will either force banks to lend to increasing risky borrowers or enforce negative rates on its customers (potentially causing depositor flight). In an uncertain economic environment, neither choice is very palatable for banks. This leaves the option of central banks pushing rates further into negative territory as one that has limited gains and could keep FX volatility elevated. Inflation expectations are significantly correlated to oil prices, a weight on inflation that is generally accepted by central bankers to be a temporary influence. Accordingly, central banks shouldn’t be reacting to the volatility that the oil price movements are having on overall market sentiment. We feel that volatility is moderating and knee jerk policy reactions are likely to be a mistake and generate unintended consequences.

(Click to enlarge) Source: Bloomberg, ETF Securities

The impact on currency?

The beggar thy neighbour nature of central bank stimulus on currencies appears to be very myopic, short-lived and unlikely to have a sustained (if any) impact on trade. The idea that efficiency gains can drive rising export volumes seems flawed. The ‘J-curve effect’ is likely to take several months before improvement is seen in trade volumes. The UK and the US are the top two trading partners for the Eurozone countries, accounting for around 25% of total exports outside the Euro Area. In order for a meaningful improvement in trade, a sustainable depreciation in the Euro is required. This will not happen if the ECB continues its recent method of promising more than it delivers.

Additionally, rising FX market volatility has certainly been a factor in curbing the ambition of policymakers seeking competitive depreciations of local currencies, by limiting the timeframe of the currency response to policy changes.

(Click to enlarge) Source: Bloomberg, ETF Securities

Draghi to the rescue?

The next policy signpost is this week’s ECB meeting. Expectations remain high that the central bank will cut interest rates further and add to its QE program. Although most G10 central banks do not have a specific currency mandate (objective), it comes as no surprise that central bank policy indirectly impacts currencies. ECB President Draghi noted at its January meeting that, ‘ it’s pretty clear that our actions have an effect on the exchange rate’.

Interest rate differentials matter for currencies in any environment, but particularly when yield is such a scarce commodity as it is currently. In order to have a sustained impact on the local currency (the so-called easy win for efficiency gains), the central bank has to do more than its competitors, something that isn’t happening. Central banks need to send positive signals to market participants if they believe (as we do ) that the global recovery remains on a recovery path. Buying riskier debt instruments within the QE program can help restore some normalcy to government bond markets by switching more QE demand to private sector debt markets.

Composition of ECB balance sheet remains firmly skewed to government debt purchases. The ECB’s Public Sector Purchase program, of which the vast majority is sovereign bonds, accounts for over 75% of its QE asset purchases. The main difference between the Asset Backed Security Purchase Program (ABSPP) and the Covered Bond Purchase Program (CBPP3) schemes is that covered bond purchases remain on the balance sheet of the banks and purchases under ABSPP program can help relieve balance sheet stress of the banking sector because the debt pool is taken off balance sheet – something that investors have been acutely worried by in recent months. Nonetheless, both programs can help lift demand for the underlying bonds and motivate lending to (riskier sectors of) the real economy, as rates remain historically low, thereby repairing the credit transmission mechanism and supporting growth. The ECB could also loosen the criteria for eligibility for the ABSPP and CBPP3 programs.

(Click to enlarge) Source: European Central Bank, ETF Securities

Without further risk taking from the ECB and its ability to differentiate itself from other central banks in terms of generic QE and declining rates, the Euro is likely to reverse course and become a burden for the economic union’s trade volumes. The ECB has consistently over promised and under delivered and we expect next week’s meeting to again disappoint.

Important Information

General

This communication has been issued and approved for the purpose of section 21 of the Financial Services and Markets Act 2000 by ETF Securities (UK) Limited (“ETFS UK”) which is authorised and regulated by the United Kingdom Financial Conduct Authority (the “FCA”).

HANetf meddelae att U.S. Global Investors har förvärvat, HANetf Travel, The Travel UCITS ETF (ticker: 7RIP).

U.S. Global Investors är en innovativ investeringsförvaltare med stor erfarenhet av globala marknader och specialiserade sektorer. Företaget grundades som en investeringsklubb och blev en registrerad investeringsrådgivare 1968 och har en lång historia av globala investeringar och lansering av förstklassiga investeringsprodukter.

Bolaget förvärvade HANetf Travel (7RIP) – som också är listat som TRIP eller TRYP på vissa europeiska marknader – från HANetf. 7RIP ska inte förväxlas med det amerikanska onlinebokningsföretaget TripAdvisor, som också handlar under tickern TRIP på Nasdaq.

”Vi är mycket glada över den här sammanslagningen och vi tror att 7RIP kommer att komplettera vår serie av dynamiska, smarta beta 2.0 ETF:er,” säger Frank Holmes, VD och Chief Investment Officer på U.S. Global Investors.

Bolaget förvaltar U.S. Global Jets ETF (NYSE: JETS), en USA-baserad ETF som investerar i kommersiella flygbolag, flygplatstjänster, flygplanstillverkare och onlinebokningsföretag. År 2021, i samarbete med HANetf, lanserade företaget U.S. Global Jets UCITS ETF som Europas första och enda globala flygbolagsindustri ETF. JETS-portföljen använder smart beta 2.0-fundamental, vilket innebär att den kombinerar passiv investering och en mer faktorbaserad, kvantamentell metod.

7RIP försöker dölja Solactive Travel Index, som spårar börsnoterade företag som är involverade i resebranschen, inklusive flygbolag, hotell, resebyråer och kryssningsrederier.

Holmes anser att kryssningsrederier är ett intressant tillägg till temat för globala reseinvesteringar, vilket är anledningen till att han förespråkade sammanslagningen av de två UCITS-produkterna:

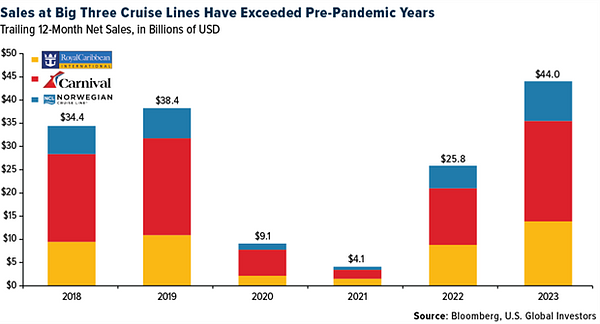

”Precis som det kommersiella flyget var kryssningsindustrin en av de hårdast drabbade under pandemin, men under månaderna sedan har den sett en stark återuppgång i efterfrågan”, säger Holmes. ”Kryssningspassagerarvolymerna ökade med nästan 7 % globalt från 2019 till 2023, enligt Cruise Lines International Association (CLIA), med Nordamerika som levererade den starkaste tillväxten på 17,5 %.”

Ökad efterfrågan på fritidsresor har resulterat i högre intäkter för kryssningsrederierna. År 2023 hade de tre stora namnen – Carnival, Royal Caribbean och Norwegian – en sammanlagd 12-månaders nettoomsättning på cirka 44 miljarder dollar, upp från 38,2 miljarder dollar under pre-pandemin 2019.

Handla 7RIP ETF

HANetf Airlines Hotels Cruise Lines UCITS ETF (7RIP ETF) är en europeisk börshandlad fond som handlas på bland annat London Stock Exchange och tyska Xetra.

Det betyder att det går att handla andelar i denna ETF genom de flesta svenska banker och Internetmäklare, till exempel DEGIRO, Nordnet, Aktieinvest och Avanza.

U.S. Global Investors tar över HANetf Travel

David LaValle diskuterar Bitcoins utveckling

AAKG ETF ger exponering mot tekniska innovationer inom den genomiska hälsovårdssektorn

Successfully navigate through Bitcoin & Cryptoassets Markets

The Bitcoin Halving and Beyond

ETFmarknaden i Europa firar sitt 24-årsjubileum med tillgångar på två biljoner USD

De mest populära börshandlade fonderna mars 2024

3 ETF:er du nog inte visste finns

FUIG ETF investerar i hållbara företagsobligationer som följer Parisavtalet

Tillgång till obligationsmarknaden för företagsobligationer från utvecklade marknader

-

Nyheter1 vecka sedan

Nyheter1 vecka sedanETFmarknaden i Europa firar sitt 24-årsjubileum med tillgångar på två biljoner USD

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanDe mest populära börshandlade fonderna mars 2024

-

Nyheter4 veckor sedan

Nyheter4 veckor sedan3 ETF:er du nog inte visste finns

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanFUIG ETF investerar i hållbara företagsobligationer som följer Parisavtalet

-

Nyheter1 vecka sedan

Nyheter1 vecka sedanTillgång till obligationsmarknaden för företagsobligationer från utvecklade marknader

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanFörsvarsfond når förvaltad volym på 500 MUSD

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanVad händer härnäst för Bitcoin?

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanDen största källan till elektricitet i Europa